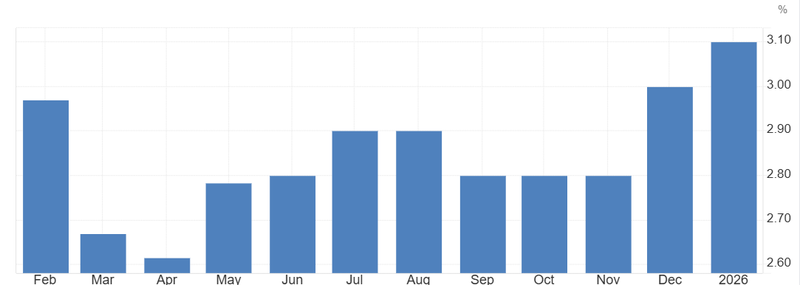

Today's PCE: fed's first real test on the path ahead

The latest PCE cycle shows inflation is no longer falling in a clean line, it’s flattening out, and energy is accelerating that stall. Core PCE at 3.1%, with expectations near 3.0%, keeps the Federal Reserve well above its 2% target

Core PCE at 3.1%, with expectations near 3.0%, keeps the Federal Reserve well above its 2% target.

A higher PCE print could shift that debate toward whether cuts happen at all in the near term.

Persistence is enough to keep policy restrictive for longer.

Disinflation stalls as energy reshapes the path

The latest PCE cycle shows inflation is no longer falling in a clean line, it’s flattening out, and energy is accelerating that stall. Core PCE at 3.1%, with expectations near 3.0%, keeps the Federal Reserve well above its 2% target, but the real concern is the loss of momentum. Monthly core readings around 0.4% remain too firm, while producer prices and services costs stay sticky. At the same time, real consumer spending is soft once adjusted for inflation, suggesting demand is not strong but inflation is not easing either. That combination is uncomfortable. It signals not a resurgence, but persistence.

Oil near $98 shifts this from cyclical stickiness to something more structural. PCE captures past pricing, but markets are already looking ahead. Energy acts as a transmission channel feeding into fuel, freight, shipping and utilities even if core measures initially filter it out. The lag matters. Inflation may not spike immediately, but behaviour adjusts quickly. Firms pass through costs faster, and households adjust expectations sooner. That is how inflation becomes embedded not through a surge, but through persistence.

Source: U.S. Bureau of Labor Statistics

If PCE is higher

A PCE print above 3.0%, especially with firm monthly momentum, would likely force a sharp repricing across rates and risk assets. Treasury yields would rise as rate-cut expectations are pushed back, the dollar would strengthen, and equities, particularly growth and other duration-sensitive sectors, would likely come under pressure. The first reaction would be tactical, but the bigger move would be narrative driven.

The market is still debating when cuts begin. A hot PCE print could shift that debate toward whether cuts happen at all in the near term. That is where the real damage sits, because once the market starts questioning the easing path itself, financial conditions tighten even if the Fed does nothing. Higher yields, a firmer dollar, and weaker risk appetite do part of the central bank’s work for it.

If PCE is softer

A softer print at or below 3.0% would likely trigger an immediate relief rally. Yields could slip, the dollar could ease, and equities could bounce, especially in rate-sensitive pockets of the market. But that move may prove fragile because the Fed is unlikely to change direction on the basis of one slightly better number, especially with energy risks still rising.

That is what makes the reaction asymmetric. A strong print can change the story quickly; a softer one usually only delays the worry. Investors may initially price relief, but they will quickly refocus on whether energy costs and sticky services inflation are about to reintroduce pressure in the next few prints. In that sense, a mild downside surprise buys time, not conviction.

Credibility is the real issue

The deeper risk is no longer only inflation itself, but the Fed’s credibility in controlling it. Short-term inflation expectations can drift higher even while longer-term expectations remain anchored, and that early movement matters. Central banks can tolerate inflation above target for a time, but they cannot afford to look reactive or behind the curve.

That is why the Fed’s reaction function has become more defensive. Policymakers are not just responding to realized inflation anymore; they are reacting to the risk that inflation stops improving. Energy shocks, geopolitics, and sticky services inflation all push in the same direction: not necessarily toward a fresh inflation surge, but toward persistence. Persistence is enough to keep policy restrictive for longer.

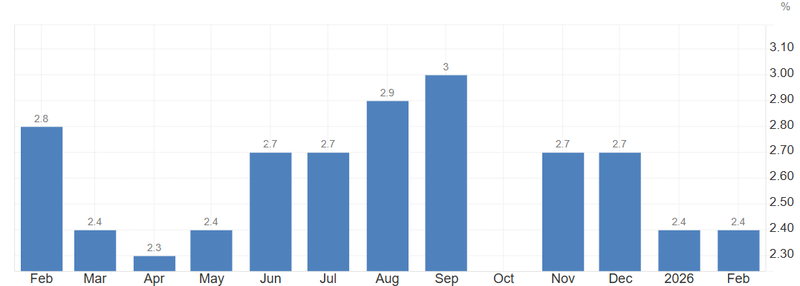

Tomorrow’s CPI adds another layer of tension. Expectations for a rise to 3.4% from 2.4% would be a sharp jump and would reinforce the idea that price pressures are rebuilding rather than fading. Even if part of that move reflects energy, the signal would still matter because markets trade the direction of inflation expectations, not just the mechanical breakdown.

If CPI confirms that inflation is re-accelerating or even just refusing to cool, the Fed will have little room to ease. That would be uncomfortable for growth, earnings, and valuation multiples because the market is still trying to reconcile slowing activity with elevated rates. The result is a market that gets weaker macro support just when it most wants policy relief.

Source: U.S. Bureau of Labor Statistics