Could geopolitical tensions in the Middle East delay the path of rate cuts?

The Federal Reserve heads into this week’s meeting facing a more complicated policy backdrop, as the conflict in the Middle East revives inflation risks and forces markets to rethink the path for US interest rates. What had been a debate over when cuts might begin is increasingly turning into a tougher question: whether the Fed will be able to cut at all this year.

The Fed is confronting new inflation risks tied to the Middle East conflict.

Core PCE rose to 3.1% in January from 2.6% last April.

Markets have sharply reduced expectations for rate cuts this year.

Policymakers now face the risk of higher inflation and slower growth at the same time.

A new shock hits the inflation fight

Federal Reserve officials are once again being forced to navigate an inflation story that refuses to stay quiet for long. Just as policymakers were trying to regain confidence that price pressures were moving steadily back toward target, the latest conflict involving the United States and Iran has injected a fresh layer of uncertainty into the outlook.

For the fifth year in a row, the Fed’s path back to 2% inflation is being disrupted by an external shock. First came the aftershocks of the pandemic. Then Russia’s invasion of Ukraine triggered an energy surge. After that came tariffs and renewed trade frictions. Now the Middle East is threatening to reopen the inflation chapter through oil and broader commodity markets.

Inflation had already stopped improving

Even before the latest geopolitical escalation, the inflation picture was becoming less comfortable. The Fed’s preferred underlying measure, core personal consumption expenditures, accelerated to 3.1% in January after falling to 2.6% last April. That reversal suggested the disinflation process had already begun to stall.

Source: Tradingeconomics

That matters because the Fed had been hoping for clearer evidence that inflation was moving lower in a durable way. Instead, the data now point to an economy where price pressures remain sticky even before any full pass-through from higher energy prices appears.

Oil is the new complication

The biggest near-term problem is simple: higher oil prices make the Fed’s job uglier. Energy shocks tend to lift inflation while also squeezing demand, since households face higher fuel and transport costs and businesses face rising input prices.

That creates the kind of policy headache central banks hate most. Inflation moves up, growth risks move down, and the space for clean policy signaling narrows fast. If tensions ease, oil could retreat and the shock may fade. If the conflict deepens, the Fed could be staring at a more persistent inflation impulse paired with softer activity.

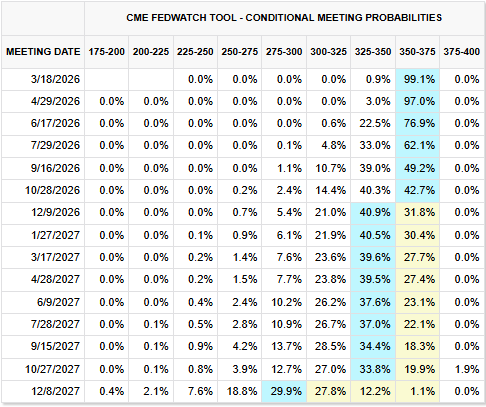

Markets are rapidly rethinking rate cuts

Financial markets have already started adjusting. Expectations for easing have been cut back sharply, with the implied probability of a rate cut by December falling to 47% from 74% before the Iran war began.

That is a meaningful repricing. It tells you investors are no longer asking only when the first cut arrives. They are beginning to wonder whether the Fed will be able to deliver any easing at all in 2026 without risking a fresh inflation mistake.

Source: CME Group

This week’s meeting matters more than usual

The upcoming Fed meeting now carries extra weight. Investors will be focused on three things in particular: the wording of the policy statement, the updated economic projections, and Chair Jerome Powell’s press conference.

If policymakers revise inflation forecasts higher, the argument for cuts becomes much harder to defend. That is especially true if officials also judge that current policy is not meaningfully restrictive anymore. In that case, the hurdle for easing rises further.

At the same time, some Fed officials are still watching the labor market closely. An energy shock that pushes up prices while squeezing household budgets could eventually weaken spending and growth. That keeps alive the possibility that the economy slows even as inflation remains uncomfortable.

The debate has changed

That is why the center of the policy discussion is shifting. The question is no longer just when rate cuts begin. It is whether the Fed can still present easing as the likely next step without losing credibility on inflation.

For now, caution is the obvious response. The range of possible outcomes has widened, and the Fed is unlikely to lock itself into a firm path while oil, inflation and geopolitical risks are all moving targets at once.

The result is a central bank stuck in a familiar but unpleasant place: waiting for clearer evidence, knowing that the next move could still be down, delayed — or, if the shock worsens enough, not down at all.