Japan inflation risks rise as war and policy collide

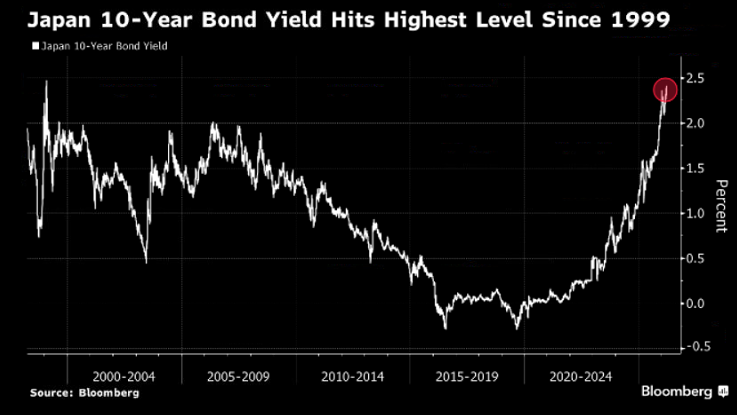

Japan is once again being pulled into a familiar problem rising inflation driven by forces largely outside its control. The shift is already visible in markets. Japanese government bond yields have climbed to their highest levels since 1999, signaling not just rising inflation expectations but also a lack of natural buyers at current levels.

Estimates suggest that even a 10% increase in oil prices can lift inflation by around 0.3 percentage points.

Japanese government bond yields have climbed to their highest levels since 1999.

70% probability now assigned to a rate hike as soon as April.

Inflation shock Japan can’t absorb easily

Japan is once again being pulled into a familiar problem rising inflation driven by forces largely outside its control. The escalation of conflict involving Iran is rapidly feeding into global energy prices, and for Japan, that is not just another macro variable. It is a direct and immediate vulnerability, one that transmits quickly through the entire economy.

Oil has already surged roughly 50% since the outbreak of the war, and the implications are only beginning to surface. As a heavily import-dependent economy, Japan does not absorb energy shocks gradually they pass through quickly into producer costs, utility bills, and ultimately consumer prices. Estimates suggest that even a 10% increase in oil prices can lift inflation by around 0.3 percentage points. At current levels, the cumulative impact points to a material reacceleration in inflation over the coming months, not yet fully reflected in official data.

What matters now is the lag this creates a window where markets are already pricing higher inflation, but policymakers are still reacting to older data. As those higher energy costs filter through supply chains, Japan is likely to face a renewed phase of inflation pressure one that could push readings further above target and test the Bank of Japan’s tolerance.

If oil prices remain elevated or move higher from here, the next stage is unlikely to be just higher inflation it will be a shift in expectations. Businesses may begin adjusting pricing behavior more aggressively, and households, already strained by years of rising costs, could start to anticipate further increases. That is where the risk becomes structural rather than temporary.

The case for a rate hike is building

Against this backdrop, the case for policy tightening is becoming increasingly difficult to ignore. Markets are already pricing roughly a 70% chance that the Bank of Japan could move as soon as this month, pulling forward what was once seen as a distant normalization path.

Inflation remains above target, with risks skewed to the upside as energy fed into the next phase of price pressures. In isolation, that would support gradual tightening, but the situation is no longer that simple.

The shift is already visible in markets. Japanese government bond yields have climbed to their highest levels since 1999, signaling not just rising inflation expectations but also a lack of natural buyers at current levels. Financial conditions are tightening ahead of policy, increasing pressure on the BOJ to act.

If incoming data begins to reflect the full impact of higher energy prices, a rate hike this month would mark more than a step it would signal a shift toward a more reactive policy stance, with less room to delay.

Source: Bloomberg

Fiscal pressure adds fuel to the fire

At the same time, fiscal policy is starting to move in the opposite direction. Prime Minister Sanae Takaichi has already signaled increased spending to cushion households from rising living costs, with more measures likely if pressures persist.

While this may ease short-term strain, it risks adding to inflation at a time when price pressures are already elevated. Fiscal support in this environment doesn’t just offset pain, it can reinforce it.

This sets up a growing tension. The BOJ is being pushed toward tightening, while the government is leaning toward stimulus. If both paths continue, policy will begin working against itself, complicating the inflation outlook and increasing the risk of a more volatile adjustment ahead.

The risk of policy hesitation

The more critical risk, however, lies in hesitation. If political considerations begin to influence monetary policy decisions, the consequences could extend beyond inflation.

Markets are highly sensitive to any sign that the Bank of Japan is falling behind the curve. That risk is already being reflected in pricing, with roughly a 70% probability now assigned to a rate hike as soon as April. At the same time, Japanese yields have climbed to their highest levels in over two decades, signaling that markets are moving ahead of the central bank.

If investors begin to doubt the BOJ’s commitment to stabilizing inflation, the response could be swift particularly in the currency market. A delayed policy response in the face of rising inflation risks could trigger renewed yen weakness, with foreign investors accelerating selling. A weaker yen would, in turn, amplify imported inflation, especially through higher energy costs.

If oil prices remain elevated and inflation begins to accelerate further, the BOJ may have little room to wait. What is currently seen as a probable move could quickly become a necessary one.

Governor Kazuo Ueda has emphasized that decisions will depend on how inflation risks evolve, reflecting a central bank navigating uncertainty rather than leading it. But the challenge is timing. Move too early, and policy risks tightening into an external shock that weakens growth. Move too late, and inflation expectations may begin to drift, eroding credibility.

What makes this cycle particularly difficult is the nature of inflation itself. It is not demand driven, but energy-led, more volatile, less predictable, and harder to control. That leaves the BOJ increasingly reactive, raising the risk that it falls behind if pressures continue to build.