BoE between cooling growth and rising inflation risks

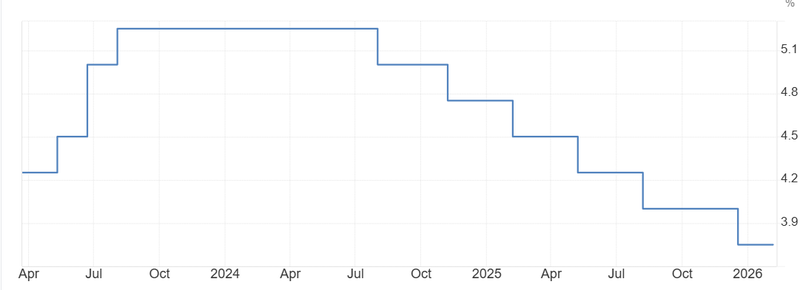

All eyes are on today’s decision from the Bank of England, where policymakers are widely expected to hold interest rates at 3.75%. Just a few weeks ago, markets were leaning toward a near-term rate cut to 3.50%, but that view has shifted quickly.

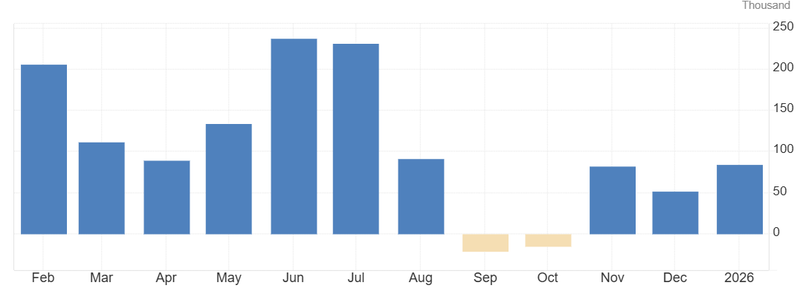

The number of people in employment rose by 84,000 to 34.31 million in the three months to January 2026.

The central bank is no longer in tightening mode, but it is not ready to ease either.

Today’s decision may not deliver a surprise but the guidance that comes with it could set the tone for UK monetary policy.

Labour market shows mixed resilience

Recent labour market data adds another layer to the policy debate. The number of people in employment rose by 84,000 to 34.31 million in the three months to January 2026, significantly beating expectations of a decline and marking the strongest job growth since late summer. Gains were seen across both full-time and part-time roles, suggesting that, at least on the surface, the labour market is holding up better than expected.

However, the broader picture is less straightforward. The unemployment rate held at 5.2%, still its highest level since early 2021, and total unemployment increased by 37,000 to 1.869 million. More notably, the rise was concentrated among those unemployed for six months or longer, pointing to a gradual build-up of slack in the labour market.

For policymakers, this combination is important. Strong headline job creation suggests resilience, but rising longer-term unemployment indicates that underlying conditions may be weakening. This dynamic reduces the risk of wage-driven inflation but also signals that economic momentum is slowing beneath the surface.

Source: Office for National Statistics

Market expectations and policy path

The sharp repricing in interest rate expectations has been one of the more notable shifts in recent weeks. Earlier in the year, markets were confident that rate cuts would begin in the near term, with a move to 3.50% seen as highly likely. That confidence has faded as energy prices climbed and inflation risks have resurfaced.

While most economists still expect easing later in 2026, the timing and pace are now far less certain. If inflation proves more persistent, particularly due to elevated oil and gas prices, the Bank of England may delay cuts or proceed more gradually than previously anticipated. On the other hand, if growth weakens further and labour market conditions continue to soften, pressure to ease policy could return more quickly.

Based on current market pricing, expectations are shifting toward a more gradual easing cycle, with around one to two rate cuts priced in for the second half of 2026 if conditions remain broadly unchanged. Looking further ahead into 2027, markets are leaning toward a cumulative easing of 75 to 100 basis points, though this remains highly dependent on how inflation evolves.

This leaves policy in a holding pattern for now. The central bank is no longer in tightening mode, but it is not ready to ease either. Instead, it is watching closely, waiting for clearer signals from both inflation and growth data. For markets, the key risk is that expectations continue to shift as new data comes in, meaning the path of rates is likely to remain fluid rather than fixed.

A delicate balance ahead

The UK economy is entering a phase where conflicting forces are pulling in different directions. On one side, easing inflation and signs of labour market cooling support the case for eventual rate cuts. On the other, rising energy prices and geopolitical uncertainty are reintroducing upside risks to inflation.

For the Bank of England, this means staying flexible. Holding rates at 3.75% buys time, allowing policymakers to assess whether the recent inflation pressures are temporary or something more persistent.

For markets, the takeaway is clear: the path toward lower rates is no longer straightforward. Expectations will likely continue to shift with incoming data, and central bank communication will play a crucial role in shaping sentiment.

In this environment, today’s decision may not deliver a surprise but the guidance that comes with it could set the tone for UK monetary policy, and market expectations, for months to come.

Source: Bank of England