Gold heads into Fed week, but the real question is the tone

Gold is entering the Fed week with a familiar trigger, but an unfamiliar reaction the renewed closure of the Strait of Hormuz, following the U.S. seizure of an Iranian-flagged vessel, has pushed energy risk back into the system.

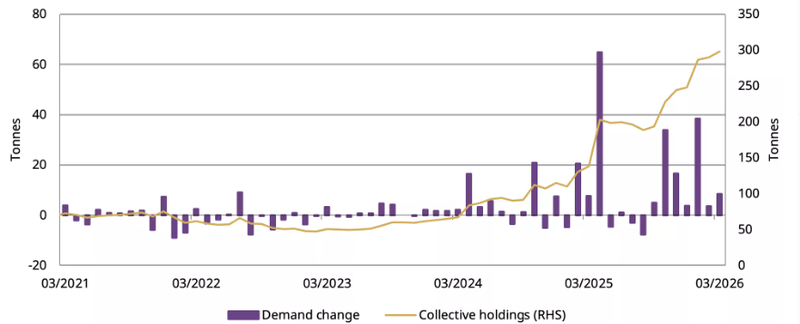

Gold record $8.5 billion inflow in Q1 2026.

Crude is not just reflecting geopolitical stress it is feeding directly into inflation expectations.

Gold is under pressure even in a volatile geopolitical backdrop.

Gold between geopolitical and ETF flows

Gold is entering the Fed week with a familiar trigger but an unfamiliar reaction the renewed closure of the Strait of Hormuz, following the U.S. seizure of an Iranian-flagged vessel, has pushed energy risk back into the system, with Brent holding near the mid-$90s and WTI in the high $80 but the more important point is not the price, it is the disruption behind it.

An estimated 10–11 million barrels per day have been affected at the peak of the disruption, and even if some flows resume, the system is no longer functioning normally. Shipping remains cautious, insurance costs are elevated, and refiners are adjusting procurement strategies this is not a clean shock that fades with headlines, it is a disruption that lingers in the system.

In past cycles, that kind of backdrop would have triggered a stronger and more consistent bid in gold. This time, it has not. Gold has struggled to extend higher, not because demand is absent, but because it is being offset. The dollar is firm, yields are elevated, and that combination is absorbing what would otherwise be a clear safe haven move.

At the same time, underlying demand is not weak, gold saw a record $8.5 billion inflow in Q1 2026, and part of that flow is structural. Chinese investors, in particular, are buying the dip with a different mindset, not as a short-term rate trade, but as a long-term monetary hedge. That creates a base of support under the market, even as macro pressures limit upside.

Source: Gold.org

Oil is no longer a shock, it is a constraint

The real shift is how oil is being interpreted. At these levels, crude is not just reflecting geopolitical stress it is feeding directly into inflation expectations. Energy sits at the front of the pricing chain. What happens in oil today shows up in transport, food, and services with a lag, but markets do not wait for the data they price the path.

That is where gold’s role becomes more complicated. Inflation, in isolation, can support gold. But inflation that forces policy to stay restrictive does the opposite. It raises real yields, strengthens the dollar, and increases the opportunity cost of holding a non-yielding asset.

Yields are not collapsing despite growth concerns. The dollar is not weakening despite geopolitical risk. That combination is not accidental, it reflects a market that is starting to price persistence, not progress, on inflation, oil moving higher is not translating into gold strength, it is tightening financial conditions instead.

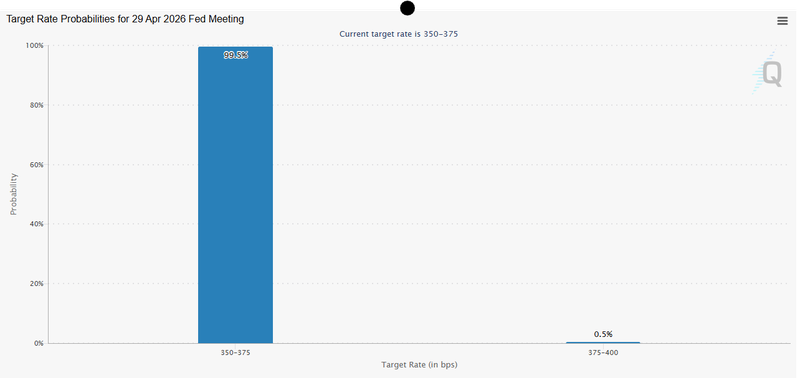

The Fed will hold, but the market is listening for direction

Rate decision itself is largely settled; no change is expected but that is not where the risk is.

The focus is on the reaction function, how the Fed interprets what is happening Powell’s tone will determine whether markets continue to price a delayed easing cycle or start to consider a more defensive stance from the Fed.

If the message leans toward caution, emphasizing inflation risks tied to energy and the need for patience, it reinforces the “higher for longer” framework that keeps yields supported, the dollar firm, and gold under pressure even in a volatile geopolitical backdrop.

If the tone leaves room for easing later in the year, acknowledging that inflation may not accelerate meaningfully despite energy shocks, gold could stabilize not because the macro picture improves immediately, but because the policy constraint eases.

Source: CME Group