Higher for now fed signals extended pause

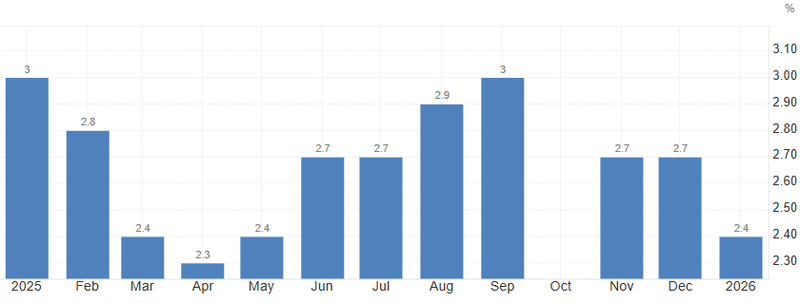

Thomas Barkin of the Federal Reserve Bank of Richmond said policy is “well positioned” to handle economic risks, and inflation has now eased to 2.4%, its lowest level since May 2025, a meaningful step closer to target. At the same time, the unemployment rate printed 4.3% lowest number since July 2025.

Holding rates in the current range remains appropriate for some time.

Inflation has now eased to 2.4%, its lowest level since May 2025.

Global investors now hold a record $64.1 trillion in U.S. financial assets.

One or two rate cuts later this year strengthens.

Fed signals patience

The Federal Reserve is signaling steady hands for now, even as inflation shows further signs of cooling.

Speaking at a conference hosted by the Federal Reserve Bank of Boston, Boston Fed President Susan Collins said it is “quite likely” that holding rates in the current range remains appropriate for some time. However, she emphasized that policymakers must stay flexible, noting that multiple economic scenarios remain possible and that decisions will continue to be patient and data driven.

On the same panel, Thomas Barkin of the Federal Reserve Bank of Richmond said policy is “well positioned” to handle economic risks. Both officials acknowledged that the labor market appears stable, describing it as a low-hire, low-fire environment, but stressed they need clearer evidence that inflation will continue moderating toward the Fed’s 2% target.

Inflation and Labour moving in the right direction

Inflation has now eased to 2.4%, its lowest level since May 2025, a meaningful step closer to target. At the same time, the unemployment rate ticked up to 4.3%, its highest reading since July 2025. While that represents some softening, the job market remains historically stable and far from recessionary territory.

Collins described the current policy stance as mildly restrictive or near neutral. To justify additional cuts, she said she is looking for “more confidence” that disinflation will continue. Her base case suggests inflation pressures could cool further later this year potentially reopening the door for rate cuts in the second half of 2026.

Source: U.S. Bureau of Labor Statistics

Tariffs and policy risk

Both officials downplayed the economic impact of the recent Supreme Court decision striking down much of President Donald Trump’s trade tariffs and the subsequent tariff adjustments. For now, policymakers do not see trade developments materially shifting the macro-outlook.

Global investors now hold a record $64.1 trillion in U.S. financial assets, highlighting continued confidence in the U.S. economy and its capital markets. That demand helps support the dollar and Treasury market stability, giving the Fed additional room to maneuver without immediate funding pressures.

Possibly two rate cuts

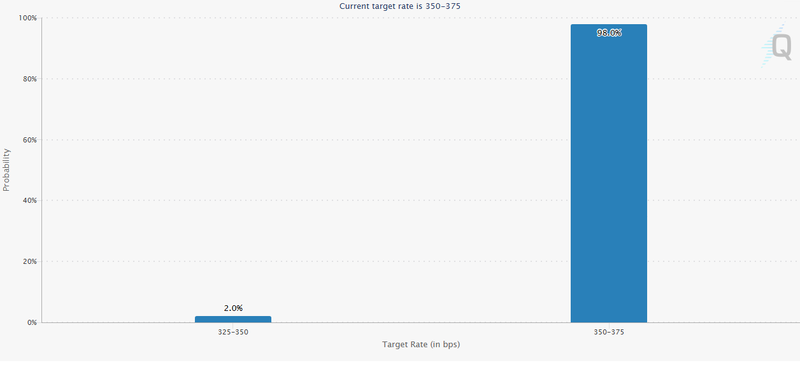

The benchmark federal funds rate remains at 3.50% to 3.75%, following cumulative cuts of 75 basis points last year. Markets are pricing in a 98% probability of a hold at the upcoming meeting, reinforcing the view that the Federal Reserve is firmly in wait-and-see mode.

The near-term path looks relatively clear: rates are likely to stay unchanged at the next meeting. The real question is not whether the Fed moves now but when it moves next.

If inflation continues its gradual descent toward the 2% target and unemployment edges slightly higher from 4.3% without signaling sharp economic weakness, the case for one or possibly two rate cuts later this year would strengthen. Such a scenario would reflect a soft-landing narrative, where price pressures cool without triggering a recession.

However, if inflation stalls above 2.5% or wage growth reaccelerates, policymakers may feel compelled to extend the pause well into early 2027. In that case, the “higher for longer” theme would regain traction, especially given the Fed’s desire to avoid a premature easing cycle.

Source: CME Group