BoE set for rate cut, but hawkish caution prevails amid sticky inflation

The Bank of England is widely expected to deliver a 25bp cut to 4.00%, but will likely avoid signaling an aggressive easing cycle as inflation expectations rise.

BoE likely to cut rates to 4.00% but stress "gradual and careful" easing amid sticky inflation.

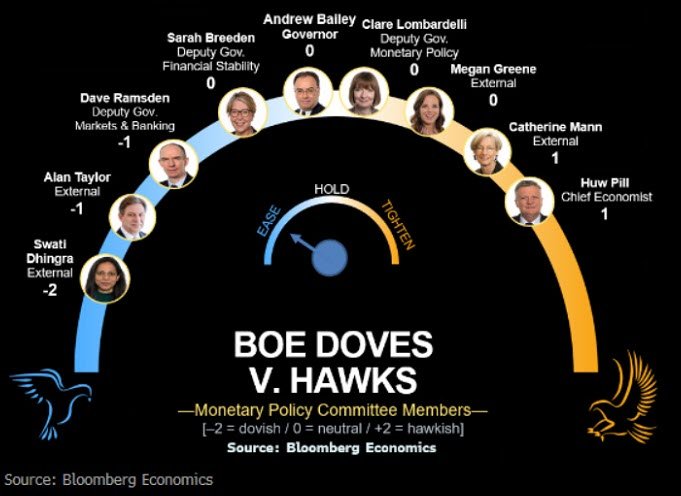

Vote split expected at 6–3, with potential for minority calls for a larger 50bp move.

Inflation expectations and food prices have surprised to the upside, limiting dovish room.

Labour market is loosening, but slower than initially estimated, reducing urgency for further cuts.

BoE poised to cut rates, but signals may stay hawkish

Markets are pricing a 90% probability that the Bank of England will lower interest rates to 4.00% at its August meeting on Thursday. However, expectations for aggressive follow-up cuts are fading, as the central bank continues to face stubborn inflation and only modest labor market softening.

A 6–3 vote split is expected, with Catherine Mann, Huw Pill, and Megan Greene likely voting to hold. Swati Dhingra could push for a larger 50bp cut, but recent labor market revisions may limit support for such a move. Alan Taylor, who has previously signaled support for five cuts this year, may still favor a cautious pace.

Sticky inflation complicates policy outlook

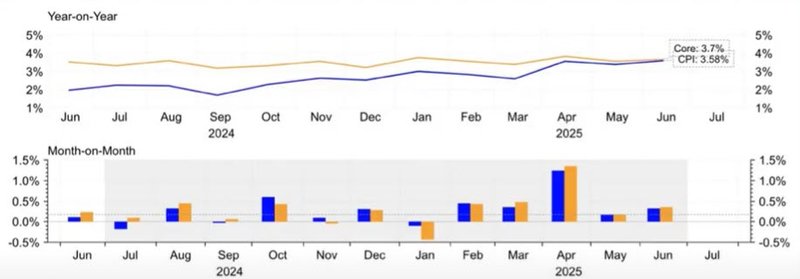

UK headline inflation rose 3.6% in June, overshooting the BoE’s forecast by 0.2 percentage points. The upside surprise was largely driven by food inflation, which remains over a full point above projections. This has pushed up medium-term inflation expectations, making policymakers wary of endorsing a faster pace of rate reductions.

Source: Refenitiv

Despite elevated CPI, the central bank is expected to reaffirm its medium-term view that inflation will return to target by 2026, assuming a policy rate of 3.5% by mid-next year. However, the near-term path for inflation will likely be revised upward in Thursday’s Monetary Policy Report.

Labour market softens, but not sharply

While the labour market is cooling, the pace of loosening is slower than previously thought. The unemployment rate rose to 4.7% in May, slightly above the BoE’s 2Q25 forecast, but revised payroll data suggests employment has not declined as steeply.

Private sector wage growth slowed to 4.9%, trailing the 5.2% forecast for Q2, and forward indicators point to sub-4% wage growth by year-end. These dynamics support a dovish tilt, but the BoE is unlikely to commit to further cuts until the trend becomes more definitive.

Growth forecast trimmed as trade frictions weigh

The UK economy contracted by -0.3% in April and -0.1% in May, largely due to fallout from U.S. tariffs, which have dented UK exports. Growth in Q2 is now seen at just 0.1%, below the central bank’s 0.25% estimate in June.

While the US-UK economic prosperity deal reduced Britain’s average tariff rate from 11% to around 8%, the BoE had already priced in some relief. Global tariffs remain lower than in the bank’s April baseline but could rise again if reciprocal measures expand.

Cautious easing, not pre-committed

Markets are watching closely for changes in BoE guidance. The Monetary Policy Committee (MPC) is expected to stick with its line that easing will be “gradual and careful”, and not on a pre-set course. Any shift in tone—such as suggesting that future cuts may be spaced more widely—would signal a potential pause in November.

Forecast updates are expected to lift near-term inflation expectations slightly, while medium-term projections remain anchored. Most financial conditions, including gas prices and interest rates, are unchanged from May’s baseline, though oil is up by $5, adding about 0.1 ppt to CPI in the near term.