Geopolitical tensions weigh on US stocks; Oil and yields advance

Geopolitical instability in the Middle East remains a primary driver of market volatility as the conflict involving the United States, Israel, and Iran persists. Oil prices settled higher following contradictory reports regarding purported diplomatic channels between Washington and Tehran. Concurrently, US equity markets retreated as investors grew increasingly concerned over a macroeconomic environment defined by persistent inflation and sustained high interest rates.

Both Brent and West Texas Intermediate (WTI) rose by more than 4% amid profound uncertainty surrounding the US-Israel-Iran conflict, with no immediate resolution in sight.

US stock indices declined in tandem due to mounting fears of a stagflationary environment—a scenario where elevated interest rates stifle economic growth while inflationary pressures remain high.

Sovereign bond yields across Western economies neared multi-month highs, driven by expectations of further monetary tightening, particularly within the United Kingdom, the European Union, and the United States.

Geopolitical volatility persists: Crude oil advances as US equities retreat

Geopolitical tensions have intensified following conflicting statements from the US and Iran. On one hand, US president Donald Trump suggested potential negotiations with Tehran regarding the reopening of the Strait of Hormuz; however, Iranian officials have categorically denied that such conversations are taking place. Simultaneously, Reuters’ reports indicate the deployment of thousands of American troops to the Middle East—specifically from the elite 82nd Airborne Division—suggesting a potential escalation of the regional conflict.

In response, crude oil prices continued their upward trajectory at the market close. The Brent futures contract (BRNM6) rose by 4.5% to reach $104 per barrel, while the West Texas Intermediate (WTI) futures contract (CLK6) increased by 4.70% to settle at $92.22 per barrel. Market participants are currently pricing in the risk of a re-escalation should US forces move to secure key Iranian-held territories. High volatility remains the defining characteristic of the energy markets in this context.

Conversely, US equity indices dropped in unison. The S&P 500 decreased by 0.37% to 6,556, the Dow Jones Industrial Average fell by 0.18% to 46,124, and the Nasdaq 100 depreciated by 0.77% to 24,002 points. Private-sector profitability is increasingly pressured by a potential hawkish Federal Reserve stance, which economic expansion could be impacted, while rising energy costs continue to fuel inflationary expectations—creating a possible stagflationary scenario.

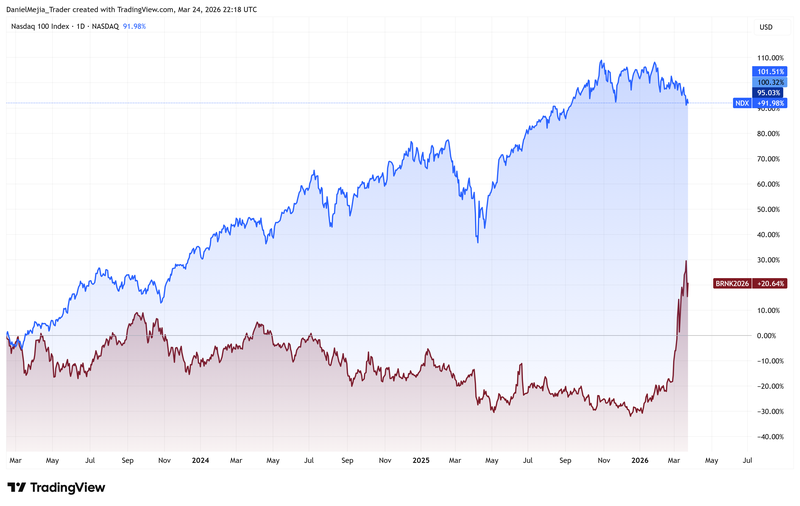

Figure 1. Nasdaq Index versus Brent Future Contract (2023–2026). Source: Data from the Nasdaq and the ICE-EUR Exchanges; Own analysis conducted via TradingView.

The figure 1 exhibits an inverse correlation where the S&P 500 is decreasing amid higher prices in the Brent futures contract.

Western bond yields climb amid rising inflationary risks

Government bond yields (10Y) across Western nations near to multi-month highs as market participants react to the inflationary risks posed by surging energy prices. Long-term yields typically advance when the market anticipates that central banks will implement further interest rate hikes to combat price pressures.

Notably, UK Gilt yields increased by 8.5 basis points to 4.98%, as the United Kingdom continues to grapple with the highest inflation levels among major Western economies (3%). US Treasury yields rose by 2 basis points to 4.36%, reflecting market expectations that the Federal Reserve could maintain a "higher-for-longer" restrictive monetary policy. Meanwhile, European sovereign bond yields edged up by 1.1 basis points to 2.99%, following signals from the European Central Bank (ECB) that it remains prepared to employ hawkish policy instruments if necessary to anchor inflation expectations.