Oil tops $90 as risk premium rises; US jobs show weakness

Crude oil prices have surged to multi-year highs driven by escalating geopolitical volatility in the Middle East. The near-closure of the Strait of Hormuz is severely disrupting energy supply chains, mainly impacting crude exports to Asian markets. Concurrently, US labour market data has exhibited significant weakness, casting doubt on the Federal Reserve’s forthcoming monetary policy trajectory.

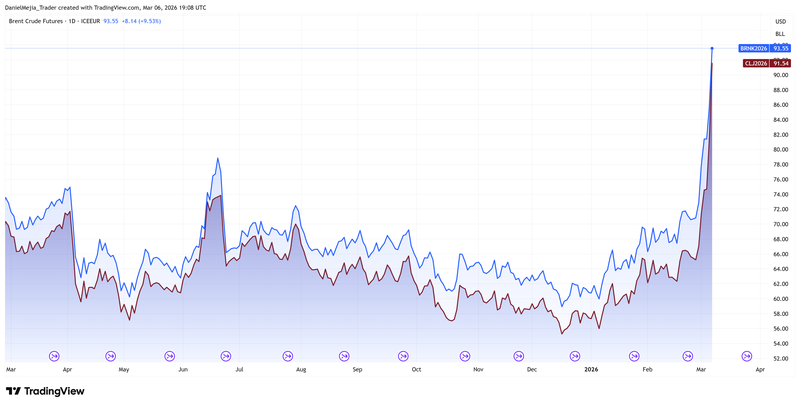

Global benchmarks Brent and WTI have surpassed the critical $90 threshold, accumulating an appreciation of approximately 50% over the last two months.

The closure of the Strait of Hormuz and the systematic targeting of energy infrastructure across the Middle East have triggered a surge in the geopolitical risk premium, driving energy prices to multi-year highs.

The latest US employment report revealed a contraction in payrolls and an uptick in the unemployment rate, while resilient average hourly earnings continue to exert upward pressure on inflationary expectations.

Global benchmarks Brent and WTI surpass $90 threshold amid escalating Middle East tensions

The primary oil benchmarks, Brent and West Texas Intermediate (WTI), have reached their highest valuations since November 2023, surpassing the $90 level. Over the past eight weeks, prices have rallied by approximately 50% as geopolitical friction between the US, Israel, and Iran intensified. This volatility has evolved into a broader regional conflict within the Middle East—a territory critical to global energy security as a premier exporter of crude oil and liquefied natural gas (LNG).

Since Saturday, 28 February, military engagements in the region have escalated significantly. Of particular concern is the Strait of Hormuz—a strategic maritime chokepoint through which approximately 20% of the world’s global oil and natural gas consumption transits. Following a coordinated US-Israeli strike, Iranian forces moved to obstruct the passage. According to reports from Reuters, approximately 15 million barrels of crude oil per day, along with 4.5 million barrels of refined products, remain stagnant due to the near-complete closure of the waterway. While this blockade severely undermines the export-dependent Iranian economy, it also poses a significant threat to Western nations currently struggling to contain "sticky" inflation rates.

In turn, Asian economies are facing acute pressure, as roughly 60% of their crude imports are sourced from the Middle East. This disruption is particularly damaging to energy-intensive sectors such as automotive manufacturing and petrochemicals.

Analysts suggest that even in the event of a swift reopening of the Strait, damaged energy infrastructure may require weeks to return to nameplate capacity. Consequently, several nations have pivoted toward alternative supply routes. Demand for Russian crude has surged as a result; for example, Indian refineries have increased their intake of Russian oil, operating under a time-limited waiver provided by the US intended to mitigate the shock to global refining capacity.

By the close of the session, Brent futures (BRNK26) rose by 8.50% to $92.68 per barrel, while WTI (CLJ26) appreciated by 11.75% to settle at $90.53. In related energy markets, natural gas futures (NGJ26) increased by 6.79% to $3.21, and gasoline futures (RBJ26) rose by 2.67% to $2.74 per unit.

Figure 1. Brent and WTI Futures Contracts (2025–2026). Source: Data from the NYMEX and ICE-EUR Exchanges; Figure obtained from TradingView.

US employment data signals weakness in NFP and unemployment; Hourly earnings accelerate

Data released by the US Bureau of Labour Statistics (BLS) revealed that Non-Farm Payrolls (NFP) contracted by 92,000 in February. This figure fell significantly short of the 59,000 increase anticipated by analysts and marked a sharp reversal from the previous month’s creation of 126,000 jobs. Simultaneously, the unemployment rate climbed from 4.3% to 4.4%, exceeding the consensus forecast. Despite the softening labour demand, Average Hourly Earnings (YoY) accelerated from 3.7% to 3.8%.

These indicators present a complex "stagflationary" signal: a contracting job market and rising unemployment coupled with wage growth that pressures inflationary expectations. While a weakening labour market typically encourages the Federal Reserve to adopt a more accommodative (dovish) monetary stance to support growth, the recent spike in energy costs complicates this outlook. A prolonged Middle East conflict would heighten the risk of an inflation rebound, complicating the U.S. central bank’s ability to balance its dual mandate.

Consequently, amid weak employment data and rising inflation concerns, U.S. equity indices declined in tandem. The S&P 500 fell 1.33% to 6,740, the Dow Jones Industrial Average dropped 0.95% to 47,501, while the Nasdaq Composite declined 1.59% to 22,387.