US personal income falls, GDP revised down—yet stocks continue to rise

US equity markets advanced in tandem following renewed optimism regarding a potential resolution to Middle Eastern geopolitical tensions. This rally persisted despite lacklustre economic data, including a contraction in personal income and a downward revision of fourth-quarter Gross Domestic Product (GDP) figures.

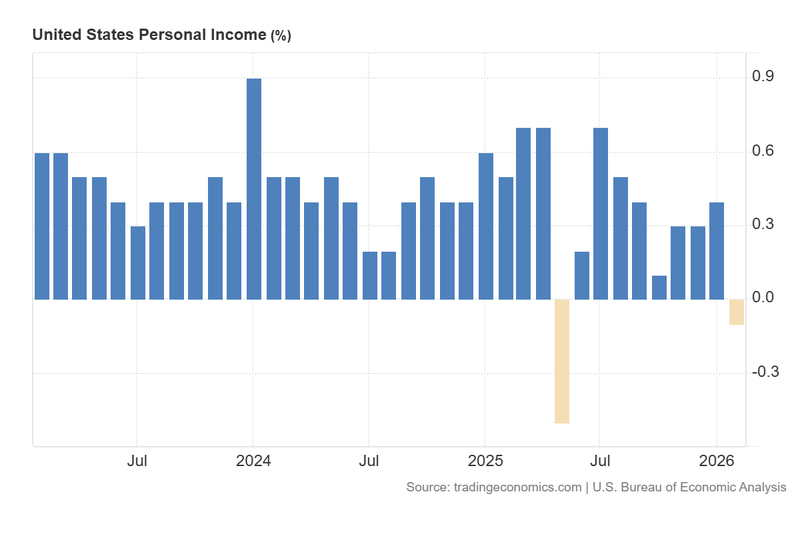

US personal income recorded its first decline since May 2025, falling by 0.1% in February. Concurrently, real income dipped by 0.5%, posing a potential risk to future consumer discretionary spending.

Fourth-quarter GDP was revised downward to 0.5% growth—a sharp deceleration from the 4.4% expansion recorded in Q3—attributed primarily to the historic government shutdown and concerns regarding trade tariffs.

Despite weak domestic data, markets rose by hopes of a diplomatic resolution in the US-Israel-Iran conflict following a temporary two-week ceasefire agreement.

While Core PCE cooled to 3% in February, investors remain wary of a potential inflationary spike in March, with projections reaching 3.3% due to rising energy costs stemming from geopolitical volatility.

US personal income marks first decrease since May 2025; GDP revised downward

According to data released by the US Bureau of Economic Analysis (BEA), personal income in February decreased by 0.1% on a month-on-month basis. This result fell short of the market consensus, which had anticipated an increase of 0.3%, and marked the first contraction since May 2025. Conversely, personal spending rose by 0.5%, aligning with analysts' estimates and slightly exceeding the prior reading of 0.3%. An analysis from Trading Economics suggests that the primary downward pressures originated from personal dividend income and current transfer receipts. These were partially offset by income gains in compensation (wages and salaries) and farm proprietors’ income, the latter supported by the Farmer Bridge Assistance Programme. However, real personal income dropped by 0.5%, a figure that could deteriorate further should inflationary pressures persist.

The latest releases suggest that a sustained decline in personal income could eventually dampen personal spending in the coming months. Historically, households attempt to maintain standard spending levels until income constraints become prolonged—a significant concern given the current decline in real purchasing power.

Concurrently, the BEA published its final adjustment for US GDP for the fourth quarter. Economic growth decelerated from 4.4% in Q3 to 0.5% in Q4, falling below the previous estimate of 0.7%. Economists attribute this deceleration to the government shutdown at the end of 2025—the longest in history—which prompted a significant contraction in government expenditure. Furthermore, uncertainty regarding the implementation of new tariffs weighed on domestic consumption and private investment.

Despite the inherent weakness in the income and GDP data, US stock markets advanced as sentiment was bolstered by hopes of a resolution in the conflict involving the US, Israel, and Iran. While a two-week ceasefire remains in place, the agreement appears fragile following continued strikes of Israel on Lebanon. Nevertheless, potential talks in the coming days have sustained market optimism. Consequently, the S&P 500 rose 0.62% to 6,824 points, the Dow Jones Industrial Average increased by 0.58% to 48,185, and the Nasdaq 100 appreciated by 0.72% to 25,082 points.

Figure 1. US Personal Income (2023-2026). Source: Data from the Bureau of Economic Analysis; Figure obtained from Trading Economics.

US PCE Index remains unchanged in February, in line with market expectations

Data from the BEA indicates that the year-on-year PCE Price Index—the Federal Reserve’s preferred inflation metric—remained unchanged at 2.8% in February, meeting analyst expectations. In contrast, the Core PCE Price Index (YoY) decelerated slightly from 3.1% in January to 3.0% in February, also in line with the market consensus.

Investors have now shifted their focus to the March inflation data, scheduled for release tomorrow, Friday, April 10th. The market consensus anticipates that the headline inflation rate will accelerate from 2.4% to 3.3%, driven largely by a sharp increase in energy prices resulting from recent geopolitical disruptions.