US services PMI, ADP jobs surprise to the upside; Stocks rally

US equity markets closed with a significant recovery, rebounding from recent losses driven by geopolitical and economic uncertainty. The ISM Services PMI reached its highest level since August 2022, while the ADP National Employment Report simultaneously showed private-sector job growth exceeding analyst forecasts.

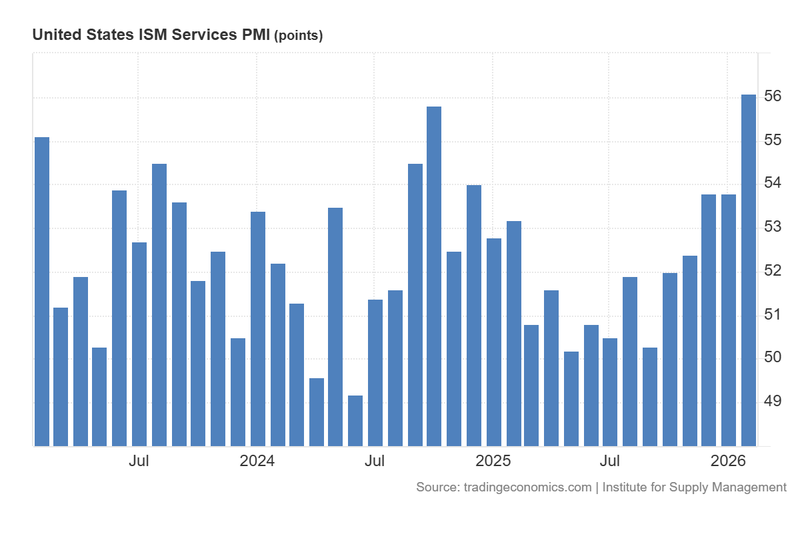

The ISM Services PMI delivered a robust reading of 56.1, marking its strongest performance since mid-2022.

ADP private employment data indicated job creation surpassed market expectations, signalling continued resilience in the US workforce.

Major US indices closed higher, bolstered by signs of rising productivity and the broader economic resilience of the United States.

Both manufacturing and non-manufacturing PMI readings in China remained below the 50.0 threshold, suggesting the economy is still struggling to regain momentum.

Australia's Q4 GDP surpassed consensus estimates, providing support for the Australian dollar, which appreciated 0.55% against the US greenback.

US services PMI and ADP report exceed forecasts: Equity markets rebound

According to data from the Institute for Supply Management (ISM), the US Services PMI increased substantially from 53.8 in January to 56.1 in February, significantly outperforming the consensus forecast of 53.5. This latest reading represents the highest level since August 2022, indicating a notable acceleration in productivity within the services sector.

This strong performance follows the ISM Manufacturing PMI released on Monday, which was updated to 52.4—exceeding the analyst forecast of 51.8. As readings above the 50.0 threshold signal expansion, both indicators currently place the US industrial and services sectors in expansionary territory. However, it should be noted that these surveys were conducted prior to the recent escalation of geopolitical conflict in the Middle East. With energy prices rising since the data collection, future manager expectations may be tempered by increasing uncertainty.

Concurrently, data from Automatic Data Processing, Inc. (ADP) revealed that private-sector employment growth accelerated from 11,000 in January to 63,000 in February, surpassing the forecast of 50,000. The "Education and Health Services" sector led the gains (+58,000), while "Professional and Business Services" saw the weakest performance (-30,000). While the ADP report is limited to private-sector payrolls, it is frequently viewed as a leading indicator for the official Non-Farm Payroll (NFP) report released on the first Friday of each month.

Buoyed by the robust Services PMI and a resilient labour market, US equity indices recovered from recent geopolitical-driven sell-offs. The S&P 500 rose by 0.78% to 6,869, the Dow Jones Industrial Average increased by 0.49% to 48,739, while the Nasdaq 100 appreciated by 1.51% at 25,093 points.

Figure 1. United States ISM Services PMI (2023–2026). Source: Data from the Institute for Supply Management; Figure obtained from Trading Economics.

Chinese manufacturing PMI edges lower, missing analyst estimates

Data from the National Bureau of Statistics (NBS) of China showed the manufacturing PMI decreasing slightly from 49.3 in January to 49.0 in February, missing the analyst forecast of 49.1. Conversely, the non-manufacturing PMI rose marginally from 49.4 to 49.5 over the same period, though this remained below the estimate of 49.8. Because both readings remain below the 50.0 neutral threshold, they indicate a continued contraction in productivity, suggesting that the Chinese economy is facing persistent difficulties in generating a renewed growth impulse.

In terms of market reaction, the FTSE China A50 index rose by 0.59% to 14,529, while the Hang Seng index increased by 1.60% to 25,534. Both indices saw a technical rebound following two days of sharp declines linked to rising geopolitical tensions and energy security concerns.

Australian GDP growth surpasses forecasts; Australian dollar recovers

According to the Australian Bureau of Statistics, Gross Domestic Product (GDP) grew by 0.8% in the fourth quarter of 2025. This exceeded the 0.5% recorded in the third quarter and beat the analyst forecast of 0.6%. Consequently, the year-on-year (YoY) growth rate accelerated from 2.1% to 2.6%. Following this positive surprise in economic activity, the AUD/USD pair appreciated by 0.55%, reaching 0.7072.