GBP caught between slowing economy and trade strength

Attention is firmly on the upcoming Bank of England (BoE) interest rate decision, with markets widely expecting rates to be held at 3.75%. After an extended period of tightening over the past two years, policymakers now face a delicate balancing act: inflation is moderating, but growth is faltering, and the labour market is beginning to show signs of strain.

Retail and construction sectors are similarly subdued, with household spending constrained by weaker real incomes and elevated borrowing costs.

Any hint of concern over slowing growth could reinforce expectations for eventual easing.

Resistance lies near 1.35674, a level that requires either stronger UK data or a weaker US dollar for a sustained breakout.

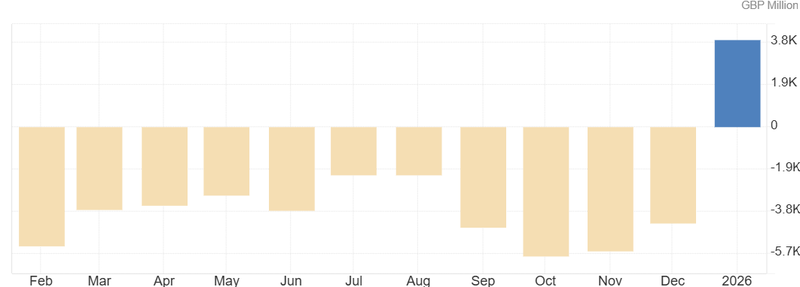

Trade surplus provides near-term support

A notable highlight for markets is the UK’s trade surplus of £3.92 billion in January 2026, reversing sharply from a £4.34 billion deficit in December. This is the first surplus since September 2024 and signals a positive shift in the country’s external accounts. Export demand to key partners, including the EU and the US, has remained steady, while imports have fallen, likely reflecting weaker domestic consumption and investment.

From a market standpoint, the UK’s trade surplus should normally give the pound some support, as it reflects more money coming into the country and less reliance on foreign borrowing. But traders are taking a cautious view. Much of the surplus appears to come from weaker imports rather than stronger exports, suggesting that domestic demand is softening. Sterling may get a short-term lift, yet without a genuine rebound in exports, the improvement in the trade balance might not be enough to drive sustained gains.

Source: Office for National Statistics

Structural pressures in the domestic economy

Beneath the surface, the UK economy is showing signs of deeper structural stress, which could influence sterling beyond headline trade figures. While the trade surplus of £3.92 billion offers temporary support, it masks underlying fragilities. GDP stalled month-on-month in January, missing forecasts, and key sectors such as services particularly administrative and support activities contracted by 2.3%. This suggests that productivity and business activity are struggling to gain momentum in areas that drive long-term growth.

Retail and construction sectors are similarly subdued, with household spending constrained by weaker real incomes and elevated borrowing costs. Business investment remains cautious, as firms delay expansion or technological upgrades amid uncertainty over financing conditions and consumer demand. The combination of soft domestic demand, sectoral underperformance, and delayed capital investment creates a structural headwind for sterling, limiting the pound’s ability to benefit fully from the trade surplus.

While the external position may support the pound in the short term, the persistent underperformance in domestic activity raises the risk that any gains could prove fleeting. A sustained divergence between export strength and domestic stagnation increases the likelihood of volatility around central bank decisions and macroeconomic releases.

Market implications

Data points to a likely pause in rates, with the BoE expected to hold at 3.75%. This allows the central bank to see how previous tightening measures are affecting the economy without adding further strain. Looking ahead, the path of monetary policy will depend on which economic forces dominate. If inflation continues to ease and growth slows further, the BoE could gradually shift toward cuts later in 2026. On the other hand, persistent price pressures might keep rates higher for longer than markets currently expect.

Investors and traders will focus heavily on the tone of the BoE’s guidance. Any signal that policymakers are more concerned about slowing growth could reinforce expectations of future easing, putting near-term pressure on GBP/USD. Conversely, a cautious stance on inflation would suggest a longer period of restrictive policy, offering temporary support to sterling. The upcoming decision is less about the actual rate and more about the narrative the BoE sets for the remainder of the year.

Technical outlook

GBP/USD is consolidating between 1.32 and 1.34, reflecting uncertainty over UK economic data and US monetary policy. Support near 1.3200 has held so far, acting as a key floor for short-term trading. A break below this level could signal a shift toward a bearish trend, especially if domestic growth disappoints further or the BoE adopts a dovish tone.

Resistance sits around 1.3567, which would require either stronger UK data or a weaker US dollar for a sustained breakout. The Relative Strength Index (RSI) currently sits at 40, indicating mild bearish momentum without the pair being oversold. Momentum indicators suggest a cautious, wait-and-see approach until the BoE’s decision and accompanying guidance provide clearer direction for the pound.

Source: Trading View