Japan hit by inflation, policy and trade pressures

Japan’s economic outlook is tightening, as persistent inflation, energy-driven uncertainty and weakening trade dynamics come together to create a more constrained and less predictable environment.

The most likely outcome is a one-off effect, but with delayed transmission, keeping inflation elevated into Q2 before gradually easing.

The BOJ is unlikely to react mechanically to oil prices alone.

The external sector is unlikely to contract sharply, but its role is changing. Rather than driving growth, it is gradually becoming more of a constraint.

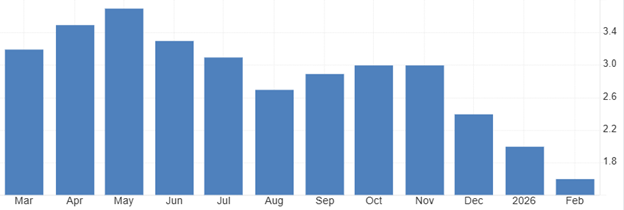

Imported inflation with delayed relief

The yen’s move toward 160 is adding to imported inflation, but the real story lies in how those costs are being passed through. Energy and food remain the first channels, but second-round effects are picking up. Higher import costs are now feeding more quickly into intermediate goods and retail prices, rather than being absorbed by companies.

This points to a structural shift. The deflationary mindset that once limited pricing power is fading and firms are becoming more willing to pass on higher costs, embedding external shocks into domestic inflation. Even if commodity prices stabilise, yen weakness alone could keep core-core inflation near 2%, especially if wage growth does not accelerate enough to offset pressure on real incomes. This leaves Japan in a fragile position, with persistent inflation but limited demand support.

Recent geopolitical developments, including a temporary ceasefire, are unlikely to bring immediate relief. Shipments still need to pass through the Strait of Hormuz and energy supply takes time to normalise. More importantly, the pace of any decline in oil prices will determine how quickly the impact fades.

The most likely outcome is a one-off effect, but with delayed transmission, keeping inflation elevated into Q2 before gradually easing.

Source: Statistics Bureau of Japan

Energy shocks complicate the BOJ’s path

Energy shocks are making the Bank of Japan’s gradual approach harder to sustain. Japan imports around 90% of its oil from the Middle East, leaving it highly exposed to any disruption around the Strait of Hormuz.

Even with the ceasefire and the sharp pullback in Brent, any inflation relief will not be immediate. There are clear delays. Cargoes still need time to move through shipping routes, insurers and shipowners remain cautious and damaged energy infrastructure cannot recover overnight. Lower oil prices on paper do not translate straight into lower import costs for Japan.

At the same time, yen weakness is amplifying the impact. Higher fuel costs are already feeding into transport, industrial inputs and overall business sentiment. The BOJ has also warned that the Middle East conflict could weigh on regional economic conditions. Markets are still pricing in around a 70% chance of a rate hike in April, even as the BOJ debates whether this is a temporary shock or something more persistent.

Looking ahead, the bar for tightening is lower than it was a year ago. The BOJ is unlikely to react mechanically to oil prices alone, but if yen weakness continues to drive imported inflation and services prices remain firm, policy normalisation could come sooner than previously expected.

Japan’s export model under pressure

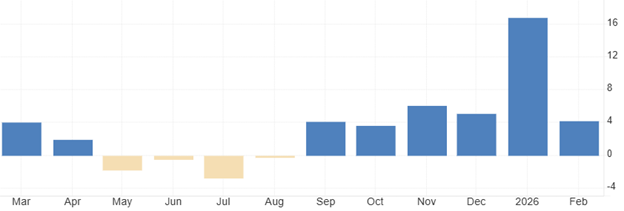

Trade tensions with China are becoming a structural challenge rather than a cyclical risk. China still accounts for around a fifth of Japan’s exports, but the relationship is growing more complex as geopolitical and technological frictions intensify.

Restrictions on critical minerals, semiconductors and dual-use goods are no longer marginal. They are now binding constraints on production. Japanese firms are being pushed to diversify supply chains and production bases, often at higher cost and with lower efficiency, gradually eroding the gains of the previous globalisation model.

Recent data is already pointing to a slowdown. Exports rose 4.2% year-on-year in February 2026 to JPY 9.6 trillion, down sharply from 16.8% the month before and marking the weakest growth since October. The slowdown reflects softer demand from both China and the US, suggesting external support is fading even before any sharper deterioration.

Looking ahead, this adjustment is likely to deepen at the margin. Trade volumes may remain relatively stable, but profitability is expected to come under pressure as firms absorb higher input costs and accelerate supply chain shifts.

The external sector is unlikely to contract sharply, but its role is changing. Rather than driving growth, it is gradually becoming more of a constraint.

Source: Ministry of Finance