Oil has repriced but the risk hasn’t gone away

Oil’s outlook has shifted from extreme supply panic to cautious stabilisation. The peak crisis premium has eased, but the market is still likely to trade with a structurally higher risk floor, reflecting the fragility of the ceasefire, constrained supply flexibility and the enduring strategic vulnerability of Hormuz.

Brent fell sharply below $100, while WTI recorded its steepest decline in years.

The World Bank has already warned that the war is likely to leave the global economy facing some combination of slower growth and higher inflation.

The market has already learned how narrow the margin of safety can become when Hormuz is threatened.

From risk premium to real supply shock

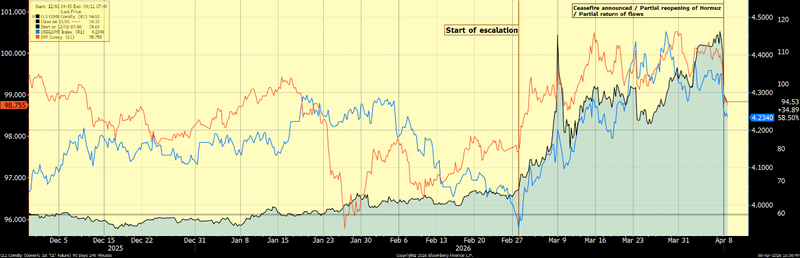

Oil has undergone the most dramatic change in outlook of any major asset class recently. At the height of the Hormuz crisis, the market was no longer merely pricing a geopolitical premium, it was pricing a genuine physical supply shock.

Reuters reported that physical crude prices approached $150 per barrel, with around 12 million barrels per day disrupted as the Strait of Hormuz situation intensified and refiners scrambled for prompt barrels. That phase of the market reflected not financial anxiety alone, but a tangible breakdown in immediate supply availability.

The decisive shift came with the announcement of a two-week ceasefire between the United States and Iran on April 7, accompanied by signals that safe passage through Hormuz would be possible during that period. The market response was immediate and dramatic: Brent fell sharply below $100, while WTI recorded its steepest decline in years. This was not simply a correction in speculative excess; it was a wholesale repricing from a scenario of prolonged physical dislocation toward one of temporary operational relief.

Lingering risks beneath the surface

Even so, the new outlook should not be interpreted as a return to normality. The ceasefire may have removed the most acute tail-risk scenario, but it has not erased the broader geopolitical risk premium embedded in crude. Iran has outlined demanding preconditions for lasting peace and the region’s energy arteries remain politically exposed.

Meanwhile, OPEC+ dynamics continue to reinforce a structurally tight backdrop. Iraq, the UAE, Kazakhstan and Oman have submitted updated compensation plans extending through to June, while the group’s planned May output increase is seen as largely symbolic under current logistical constraints.

Beyond the immediate effects, this has implications for the broader economy. The earlier oil shock had materially altered global inflation thinking, prompting concerns that central banks would be forced to stay restrictive for longer. The temporary collapse in crude has relieved some of that pressure, but not enough to fully normalise the policy outlook. The World Bank has already warned that the war is likely to leave the global economy facing some combination of slower growth and higher inflation, even if the conflict begins to ease.

What this means for Q2

For Q2, the most appropriate framework is no longer “enduring supply shock,” but rather elevated volatility above a higher geopolitical floor. Prices may continue to retreat from crisis highs if the ceasefire holds and trapped flows begin to normalise, but oil is unlikely to revert quickly to its pre-conflict equilibrium. The market has already learned how narrow the margin of safety can become when Hormuz is threatened and that lesson is unlikely to disappear within a matter of weeks.

WTI crude before, during and after the Hormuz crisis / ceasefire