ECB shift, inflation persistence and rate hike risk

The shift of the 2.0% target into 2027 matters more than the number itself. It effectively extends the ECB’s policy horizon and reduces its flexibility.

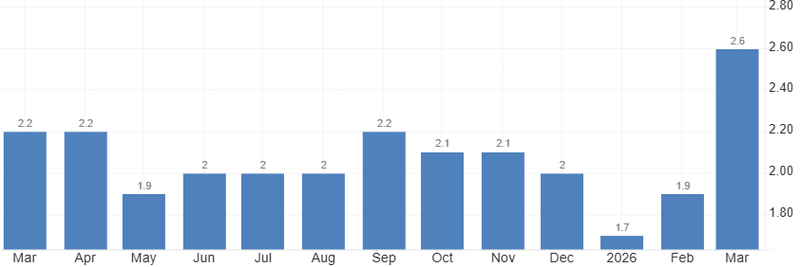

Inflation rise to 2.6%, up from 2.0%.

Yields remain supported as rate cuts are pushed further out.

June hike is now a live probability, fluctuating between roughly 53% and 68%.

Delayed target raises questions

Inflation for 2026 is now seen at 2.6%, up from 2.0%. That is not a marginal adjustment. it is a signal that the disinflation process is losing momentum at a stage where it was expected to become more predictable. Instead of converging cleanly toward target, inflation is showing persistence, particularly in components that tend to be slower-moving and more sensitive to domestic dynamics.

The shift of the 2.0% target into 2027 matters more than the number itself. It effectively extends the ECB’s policy horizon and reduces its flexibility. When inflation is expected to normalize quickly, policymakers can afford to look through short-term shocks. When that timeline stretches, credibility becomes part of the equation. The central bank is no longer just guiding inflation lower; it is defending the idea that it will eventually reach target at all.

Source: EUROSTAT

Unemployment crosses into the inflation path

The ECB’s concern is not simply that inflation is above target… it is that it risks becoming self-sustaining through second-round effects. Once price pressures begin feeding into wage negotiations, the transmission mechanism changes. Inflation is no longer imported or temporarily; it becomes domestically reinforced.

The revised unemployment forecast at 6.3% sits right in the middle of that dynamic. It does not point to overheating, but it does not signal enough slack to naturally dampen wage growth either. That middle ground is uncomfortable for policymakers. A clearly weak labor market would ease pressure on wages. A clearly tight one would justify aggressive tightening. What the ECB is facing instead is a labour market that is stable enough to sustain income growth, but not weak enough to break the inflation cycle.

That creates policy asymmetry. The central bank cannot rely on demand on its own. It has to actively lean against the risk that wages begin to adjust upward in response to past inflation.

Source: EUROSTAT

The June hike is no longer theoretical

Markets have started to reflect that shift. A June hike is no longer priced as an outlier scenario… it is now a live probability, fluctuating between roughly 53% and 68%. That range itself is telling. It reflects a market that is not fully convinced, but no longer comfortable with the idea that the next move is easing.

Until recently, the policy path was framed around timing the first cut. Now the discussion is moving toward whether the ECB might need to maintain or even extend restrictive conditions before it can pivot. That does not require a full tightening cycle… but it does reopen the door to additional action if inflation expectations fail to stabilize.

The key shift is psychological as much as numerical. Once markets start questioning the timing of cuts, the entire rate path is repriced, not just the next meeting.

In the short term, the impact is relatively clear. Front-end yields remain supported as rate cuts are pushed further out, and the euro finds some stability from a more hawkish repricing. The market is effectively removing some of the easing that had been priced too early.

If the ECB keeps policy restrictive for longer while growth momentum softens, the risk shifts from inflation persistence to policy over-tightening. Europe’s growth profile is already fragile compared to the U.S., and prolonged restriction could begin to weigh on credit conditions, investment, and consumption.

Ease too early, and inflation risks becoming embedded. Tighten or hold too long, and growth begins to deteriorate in a more structural way. Central banks can manage one side of that balance with relative clarity. Managing both simultaneously is where volatility tends to emerge.