US stocks set new highs amid hopes of conflict resolution in the Middle East

The S&P 500 and Nasdaq 100 indices have scaled record highs, propelled by growing optimism regarding potential diplomatic deliberations in Pakistan aimed at resolving the US-Israel-Iran conflict. Simultaneously, a significant drawdown in US energy inventories suggests a strengthening in demand, while a mounting political pressure on Federal Reserve Chair Jerome Powell raises critical questions regarding the continued independence of the central bank.

The S&P 500 and Nasdaq 100 achieved record valuations, with the S&P 500 closing above the significant 7,000 threshold for the first time, buoyed by hopes of geopolitical stability.

Reports of prospective peace talks between the United States and Iran in Pakistan have invigorated market sentiment, despite the absence of official confirmation and the presence of fundamentally divergent state demands.

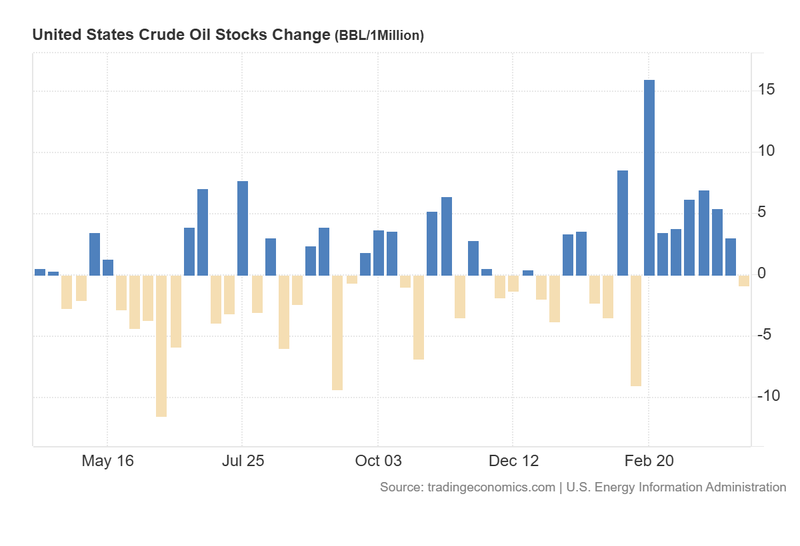

Data from the Energy Information Administration (EIA) reveals a substantial contraction in gasoline stocks by 6.3 million barrels, indicating robust demand amidst persistent global supply chain disruptions.

US president Trump has issued threats regarding the removal of Federal Reserve Chair Jerome Powell by 15 May, sparking widespread concern over the long-term autonomy of US monetary policy.

US stock markets reach record highs amidst rising hopes of conflict resolution in the Middle East

The S&P 500 and Nasdaq 100 indices concluded the latest trading session at record levels, driven by burgeoning hopes for a diplomatic resolution to the US-Israel-Iran conflict. According to reports from CNBC, a second round of discussions between US and Iranian representatives is potentially scheduled to convene next week in Pakistan—a nation that has increasingly functioned as a strategic mediator—citing sources with direct knowledge of the deliberations. However, an official confirmation of the meeting is currently pending.

While the proposed talks remain unconfirmed, market participants appear to be pricing in a de-escalation of hostilities, under the assumption that a peace agreement may be attainable in the near term. Nevertheless, it is pertinent to observe that the core requirements of the United States and Iran remain fundamentally opposed; consequently, there is a high probability that significant friction will persist, particularly as previous diplomatic efforts have concluded without resolution.

In terms of market performance, the S&P 500 rose by 0.80%, surpassing the 7,000 level for the first time to close at 7,022 points. The Nasdaq 100 similarly advanced by 1.40%, reaching a new record of 26,204 points, underscoring the dominance of the technology sector. Conversely, the Dow Jones Industrial Average retreated by 0.15% to 48,463 points, suggesting that investor appetite remains skewed toward growth-oriented enterprises rather than mature industrial entities.

US crude and gasoline inventories fall below expectations; Oil benchmarks remain stable

Weekly data from the US Energy Information Administration (EIA) indicates that crude oil inventories contracted by 0.913 million barrels, contrasting with analyst expectations of a 0.2-million-barrel increase. Although this figure does not represent a radical departure from market consensus, it marks the first inventory contraction in eight weeks, suggesting that the recent period of stock accumulation may have reached its conclusion. Concurrently, gasoline stocks plummeted by 6.328 million barrels, a figure significantly deeper than the anticipated 2.1-million-barrel drawdown. This sharp contraction in inventories points toward an uptick in demand, likely exacerbated by increased requirements from European nations currently affected by supply disruptions in the Strait of Hormuz.

Despite these notable inventory drawdowns, oil prices remained largely static. The Brent crude futures contract (BRNM6) saw a marginal increase of 0.15%, trading at $94.93, while the West Texas Intermediate (WTI) futures contract (CLK6) declined slightly by 0.07% to settle at $91.21 per barrel.

Figure 1. US Crude Oil Stocks Change (2025–2026). Source: Data from the US Energy Information Administration; Figure obtained from Trading Economics.

Trump pressures early departure of Powell, fuelling concerns over Federal Reserve autonomy

Apprehensions regarding the independence of the Federal Reserve remain acute. According to reports from Reuters, US President Donald Trump has renewed threats to remove Jerome Powell from his seat on the Federal Reserve’s Board of Governors, should Powell refuse to vacate the post on 15 May, the scheduled conclusion of his term as Chairman.

While the legal probability of a forced removal remains a subject of debate, the rhetoric alone has unsettled observers concerned with the preservation of the central bank's autonomy. A shift toward a more "dovish" composition within the Federal Open Market Committee (FOMC) would provide greater latitude for Kevin Warsh—the President’s nominee to succeed Powell—to implement monetary actions wanted by the current administration.