Hormuz blockade threat revives oil shock fears

President Donald Trump’s threat to impose a US blockade on the Strait of Hormuz has jolted markets back into worst-case mode, just days after ceasefire hopes briefly calmed energy prices. The move, if carried through, would sharply raise the risk of higher oil, slower growth and renewed inflation pressure across the global economy.

Trump says the US will begin a Hormuz blockade on April 13 after talks with Iran collapsed.

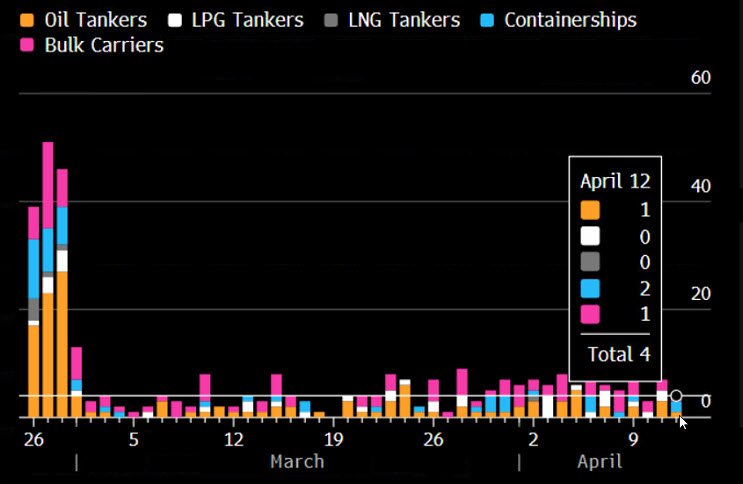

Oil tankers are already steering clear of the strait ahead of the announced move.

A blockade would deepen an already severe disruption in one of the world’s most important energy chokepoints.

The economic risk now tilts back toward higher inflation, tighter energy supply and weaker global growth.

A new escalation pushes markets back toward downside risk

The threat of a US blockade of the Strait of Hormuz has shifted the market narrative sharply back toward economic downside. After a brief period in which investors hoped diplomacy might stabilize the conflict, the collapse of peace talks and Trump’s blockade announcement have brought back the risk of a more serious supply shock in oil and gas.

This matters because Hormuz is not a marginal route. It is one of the world’s central energy arteries, and even before the latest US threat, maritime traffic through the passage was already severely constrained. Bloomberg previously reported that Iran had effectively closed the strait to all but approved vessels, while Reuters now says tankers are avoiding the route ahead of the planned US action.

The blockade threat is aimed at Iran, but the economic shock is global

The White House’s apparent objective is to squeeze Iranian exports and force new concessions after talks failed. But the economic consequences would not stop at Iran. Any formal blockade, or even a partially enforced one, would add to the disruption already choking flows of crude, LNG and refined products through the Gulf.

Reuters reported that the US says the blockade would target maritime traffic to and from Iranian ports rather than ships bound for non-Iranian ports. Even so, that distinction may not reassure shipowners, insurers or traders. In practice, once military risk rises around a chokepoint like Hormuz, the market starts pricing the disruption as regional, not narrowly legal.

Oil may not need a full closure to spike further

The most immediate effect would be on oil prices. Reuters reported that Trump’s blockade threat helped push Brent up 8% to $102.80 a barrel, highlighting how quickly the market reacts to any signal that Gulf supply could tighten further.

That is the visible part of the shock. The more dangerous part is the escalation risk behind it. A blockade could be interpreted in Tehran as a direct act of war, raising the probability of retaliation against regional infrastructure, tankers or alternative export routes. That would widen the supply hit beyond current flows and leave markets facing not just lost Iranian barrels, but a broader regional energy disruption. That risk is precisely why Reuters described the announcement as an escalation of the six-week conflict and a trigger for renewed market anxiety.

Shipping risk is now becoming the market

The most telling sign is what shipping companies are already doing. Reuters reported that oil tankers are steering clear of Hormuz ahead of the announced blockade, while some vessels reversed course rather than risk entering the Gulf.

Source: Bloomberg

That behavior matters because markets do not wait for official enforcement to price disruption. Once commercial shipping starts acting as though access is unsafe or unreliable, the supply shock begins before the policy is fully implemented. At that point, the economic damage is driven as much by fear and insurance constraints as by the formal blockade itself. Reuters also reported that the UK will not support the US-led blockade, underlining how diplomatically isolated and operationally fraught the move could become.

Growth slows, inflation rises — the worst mix is back

For the global economy, the concern is not only higher oil but the type of shock it creates. Energy spikes hit consumers directly, raise transport and input costs, and tighten financial conditions just as central banks are already struggling with sticky inflation. The result is the classic ugly mix: weaker growth and stronger price pressure at the same time.

That is why this latest turn is especially damaging for markets. It reopens the stagflation question just when investors had started hoping the worst of the war-driven energy shock might be behind them. Reuters’ reporting makes clear that the blockade threat is being read as an event with broad consequences for oil, inflation and market stability, not just as a tactical military signal.

Trump may still be bluffing, but the risk premium is real

There is still a possibility that the blockade threat is designed more to pressure Iran than to become a sustained operational reality. Reuters noted that repeated brinkmanship has already complicated the feasibility of such a move and increased fears of miscalculation.

But even if the threat is partly coercive theater, the market can no longer dismiss it casually. The lesson from the past several weeks is that every new ultimatum around Hormuz now carries immediate consequences for tanker behavior, oil pricing and inflation expectations. Whether Trump follows through fully or not, the damage from the threat itself is already being felt.