RBA raises rates again as inflation keeps pressure on policymakers

The Reserve Bank of Australia raised its official cash rate by 25 basis points to 4.35%, reinforcing the message that policymakers are becoming increasingly uncomfortable with persistent inflation.

The Bank raised the rate by 25 basis points to 4.35%.

Australia’s inflation rate climbed to 4.6%.

Bullock said inflation was already “too high” even before the latest energy shock.

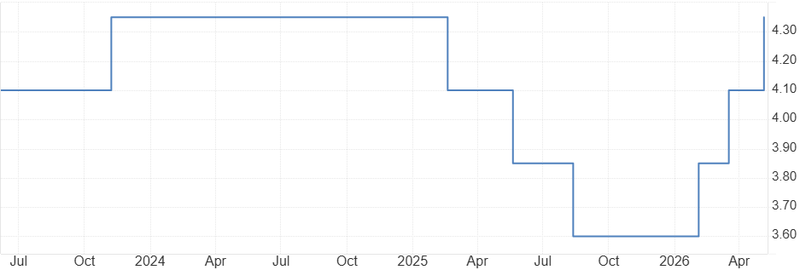

Decision voting shift after March

The Bank raised the rate by 25 basis points to 4.35%, but what matters more is how that decision was reached. The decision passed by an 8–1 majority, a notable shift from the much narrower 5–4 split at the March meeting. That change matters because it suggests the RBA is moving toward a stronger internal consensus that policy still needs to remain restrictive despite growing concerns about slowing economic activity.

Source: RBA

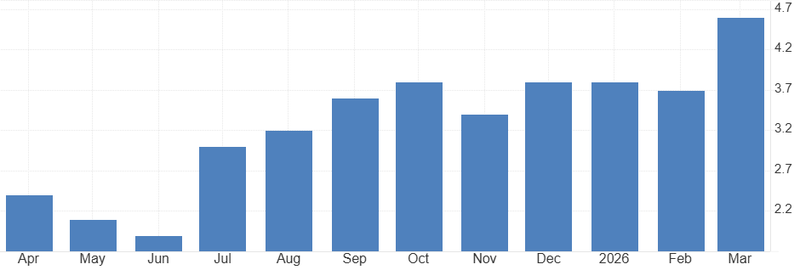

Inflation remains the central issue.

Australia’s inflation rate climbed to 4.6% in the year through March, still well above the RBA’s 2–3% target range and far enough from target to keep policymakers under pressure. The bank appears increasingly worried that inflation is proving more persistent than previously expected, especially as global energy markets become more unstable again.

Source: Australian Bureau of Statistics

Michele Bullock made that concern clear

She said inflation was already “too high” even before the latest energy shock tied to the Middle East conflict. That is an important distinction because it means the RBA does not view current inflation pressures as purely temporary or externally driven. Instead, policymakers believe that underlying domestic inflation remains strong enough on its own to justify tighter policy.

Bullock noted that labour conditions remain tight, keeping capacity pressures elevated. In practical terms, that means businesses are still competing for workers, wage pressures remain firm, and domestic inflation has room to stay sticky even if global cost pressures ease.

That creates a more difficult policy path

A strong labor market gives the RBA room to tighten further, if necessary, but it also increases the risk that inflation becomes more embedded through wages and services. That is the cycle central banks try to prevent before it becomes self-sustaining.

The larger voting margin suggests more policymakers are now leaning toward the second risk, markets had previously hoped the RBA was nearing the end of its tightening cycle as growth moderated earlier in the year. But the latest inflation data, combined with renewed geopolitical energy risks, appears to have shifted the conversation back toward inflation control rather than policy normalization.

RBA also seems increasingly aligned with the broader tone emerging from other major central banks. The ECB, Bank of England and parts of the Federal Reserve have all recently signaled greater concern about inflation persistence following the latest oil and energy shock. That global shift matters because central banks are becoming less willing to assume that inflation will continue falling smoothly from here.

RBA no longer appears focused on when it can eventually cut rates. Right now, the priority is making sure inflation does not regain momentum before the earlier tightening cycle is fully worked through the economy.