Oil between ceasefire relief and supply reality

WTI’s plunge is historic, but the move only makes sense once panic pricing is separated from underlying supply risk. The two-week ceasefire conditional on reopening the Strait of Hormuz.

15% drop reflects not just relief, but a rapid repricing of probabilities.

Refiners and traders will not assume uninterrupted flows immediately; they will wait for confirmation through actual cargo movement and delivery reliability.

This is not the start of an oversupply cycle, it is a transition from panic pricing to conditional, fragile stability.

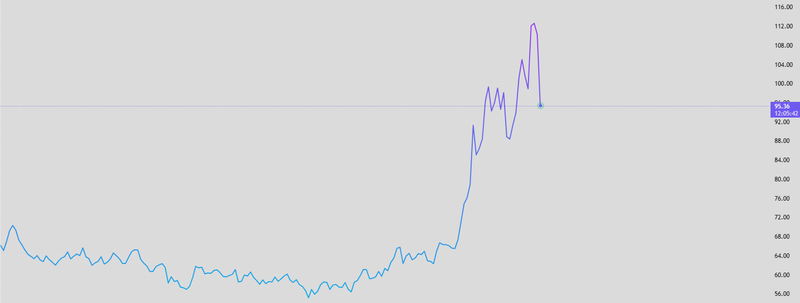

Ceasefire crushed the panic trade

WTI’s plunge is historic, but the move only makes sense once panic pricing is separated from underlying supply risk. The two-week ceasefire conditional on reopening the Strait of Hormuz removed the market’s most extreme scenario: a prolonged choke point in global oil flows that would have disrupted a meaningful share of seaborne crude. That tail risk had been heavily priced in, particularly in front-month contracts and physical differentials, where refiners were bidding aggressively for prompt barrels. The result was a market skewer toward scarcity. Once even a temporary reopening became credible, that extreme premium unwound quickly, triggering a sharp and disorderly price adjustment.

A nearly 15% drop reflects not just relief, but a rapid repricing of probabilities. The market shifted from pricing sustained disruption to a temporary de-escalation. However, crude remains well above pre-war levels, which is the more important signal. This is not a return to normal it is a recalibration of risk.

The geopolitical premium has narrowed, but it has not disappeared. The ceasefire is temporary, conditional and fragile, with no guarantee of durability or broader regional alignment. Until there is clearer evidence of stability, a residual premium will remain embedded in prices. What has been removed is panic not uncertainty.

Source: Trading View

Physical oil will heal more slowly than futures imply

The deeper constraint lies in the physical market, not the futures curve. Financial markets can reprice within minutes, but oil supply chains operate on timelines measured in days and weeks. Tankers that were delayed or rerouted during the escalation must still clear congested routes, and ports need to process backlogs before normal loading schedules resume. Shipping lanes must demonstrate consistent, repeatable safety, not just a one-off passage before volumes normalize. Insurers remain cautious, war-risk premiums are still elevated, and major shipping operators require more than a ceasefire headline to restore full operations. The system needs proof of stability, not just the absence of conflict.

Even if the Strait of Hormuz is technically open, functional normalization depends on confidence, not access alone. Refiners and traders will not assume uninterrupted flows immediately; they will wait for confirmation through actual cargo movement and delivery reliability. This creates a lag where physical tightness can persist even as futures prices fall sharply. In effect, the paper market has moved ahead of the real economy.

The next leg lower in oil prices depends less on diplomacy and more on execution: whether ships move smoothly, queues clear, insurance costs ease and delivery schedules stabilize. Until that happens, the market remains vulnerable to renewed volatility despite the apparent easing in headline risk.

Relief, but not a full reset

Over the coming three weeks, the most likely outcome is partial relief rather than a full reset. If shipping through Hormuz resumes gradually and without incident, stranded barrels will begin to re-enter the market, easing immediate supply tightness and softening prompt spreads. At the same time, OPEC+’s planned output increase from May adds incremental weight to the supply narrative, reinforcing the idea that the market is not structurally short of oil. However, these forces do not translate instantly into lower prices they operate with a clear lag between policy, logistics and physical delivery.

The market needs to see sustained, uninterrupted transit flows before it can confidently strip out the remaining geopolitical premium. In practical terms, two weeks of ceasefire is not enough. Normalization of flows, recalibration of insurance costs and the rebuilding of trader confidence typically require closer to three weeks or more of stable, incident-free conditions. Until that threshold is met, participants will price in a buffer against renewed disruption.

The result is a market that trades softer, but not comfortably lower. WTI is likely to remain highly reactive, with downside capped by residual uncertainty and upside driven by any disruption. This is not the start of an oversupply cycle, it is a transition from panic pricing to conditional, fragile stability.