Oil market between options market and supply concerns

Brent crude closed yesterday at $103.76 per barrel, up 5.42% in a single day and a staggering 47.88% over the past month. With Middle East tensions, Russian supply disruptions, and record options positioning, the market is grappling with risks that could easily push prices into uncharted territory. Here’s a deeper look at the forces at play.

Call options on the Intercontinental Exchange has exploded to 28,941 contracts up from just 3,374 a month ago.

Strait of Hormuz remains the world’s most critical energy chokepoint, handling 27–29% of global seaborne oil trade in recent years.

Russia’s oil export infrastructure is taking a brutal beating from Ukraine’s drone campaign.

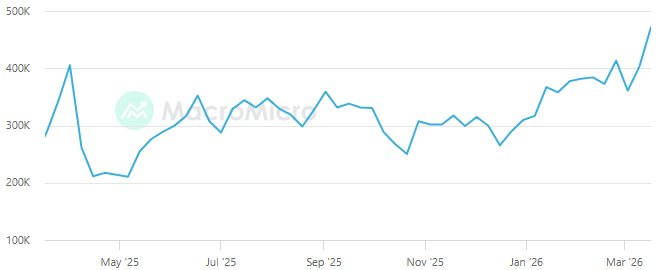

Options market tail risks dominate

The derivatives desk tells the real story of trader anxiety. Open interest in April $150 Brent call options on the Intercontinental Exchange (ICE) has exploded to 28,941 contracts up from just 3,374 a month ago. At 1,000 barrels per contract, that’s exposure to nearly 29 million barrels, or roughly $3 billion at current levels.

These aren’t speculative moonshots; they’re insurance against catastrophe. Brent’s all-time high hit $147.50 in July 2008, so $150 strikes mean serious players are hedging for a break above that historic peak. Put another way, the market is pricing in the potential for oil to double from today’s levels in weeks.

Source: MacroMicro

Strait of Hormuz easing, but still a powder keg

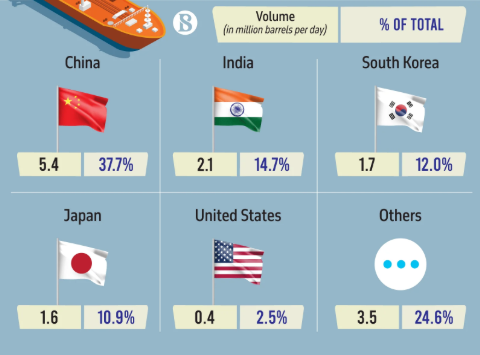

Early signs of de-escalation are emerging. COSCO Shipping has restarted Asia–Gulf routes, pointing to slight improvements in shipping conditions tied to Iran negotiations. Yet the Strait of Hormuz remains the world’s most critical energy chokepoint, handling 27–29% of global seaborne oil trade in recent years.

Asia bears the brunt: 89.2% of Hormuz flows go there, with China alone taking 37.7%, followed by India (14.7%), South Korea (12.0%), and Japan (10.9%). Insurance premiums are still elevated, tanker traffic cautious, and one misstep could halt 20+ million barrels per day.

Source: TBSnews

IEA mobilizes, governments step in

Japan’s Prime Minister Sanae Takaishi just called on the IEA to prep for a second emergency release after the agency unleashed over 400 million barrels two weeks back the biggest coordinated dump since the 1973 Arab oil embargo.

Japan’s playing it in stages: first tapping 15 days of private company stockpiles, then rolling into one full month of government-held reserves from its massive 254-day hoard (with 146 days under direct government control). That’s Japan buying time while keeping its industrial base humming despite the supply squeeze.

The U.S. led the first round with a hefty 172.2 million barrels pulled from the Strategic Petroleum Reserve leaving SPR levels at their lowest in decades. These moves blunt the immediate pain, but they also expose just how razor-thin the line is between manageable disruption and outright crisis. Everyone knows strategic stocks aren’t infinite, and burning through them this fast signal nobody expects this mess to resolve anytime soon.

Russia’s supply crisis deepens

Russia’s oil export infrastructure is taking a brutal beating from Ukraine’s drone campaign. Strikes have knocked out roughly 40% of Russia’s export capacity, equivalent to about 2 million barrels per day. Key hits include Baltic Sea hubs like Primorsk (1.4 million bpd capacity) and Ust-Luga (1.3 million bpd), plus Black Sea terminals at Novorossiysk (700,000 bpd), and even damage to the Druzhba pipeline network that feeds Europe. This is the largest short-term disruption to Russian exports in modern history, catching the market at the worst possible moment when global spare capacity languishes below 3 million bpd. Russia was already running at 95%+ utilization on its shadow fleet before this, and now Urals crude trades at a $15–20 discount to Brent the widest gap since late 2022 sanctions kicked in.

OPEC+ can barely fill the void: Saudi Arabia’s spare capacity tops out around 2.5 million bpd, but they’ve signaled reluctance to flood the market given their own fiscal needs. Meanwhile, Russia’s shadow tanker fleet (now 600+ vessels shuttling 3.5 million bpd to Asia) faces skyrocketing insurance costs and port bans, turning every voyage into a logistical nightmare.