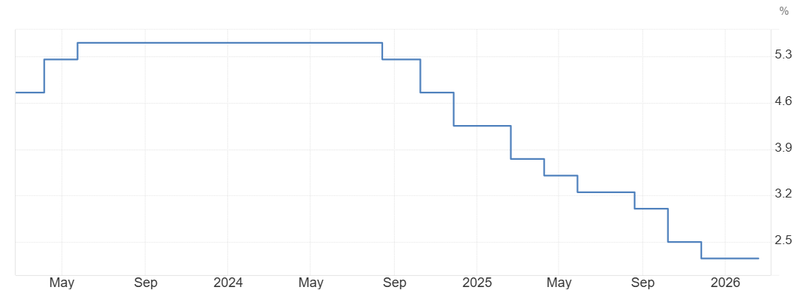

Weak trade balance reinforces rate hold in New Zealand

Last week, Governor Anna Breman signaled that the economy has room to recover this year without reigniting inflation, reinforcing the central bank’s patient stance. The RBNZ kept its cash rate unchanged and stressed that policy needs to remain accommodative for now. Following those comments, markets sharply scaled back expectations of an imminent hike, with investors now seeing only a small chance of the first increase before December.

Unemployment rising to 5.4%, the highest level since 2016.

Inflation remains stubborn around 3%.

New Zealand’s trade balance recorded a NZD -519 million deficit.

Small probability of a rate hike before December.

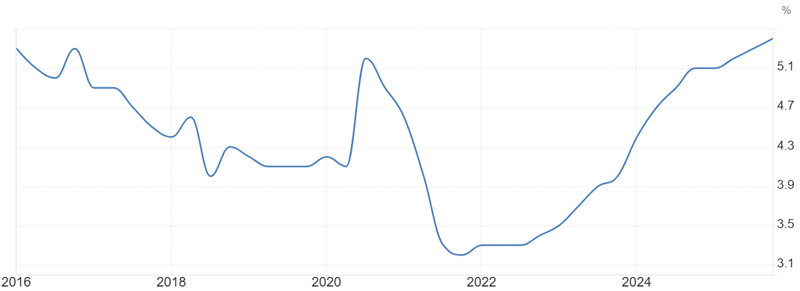

Labour market weakness builds

The latest data showed unemployment rising to 5.4%, the highest level since 2016, a clear sign that labor market momentum is fading. Just a year ago, New Zealand was operating close to full employment, with firms struggling to find workers. Now, hiring intentions have softened, job vacancies have declined, and some sectors particularly construction and retail are reporting weaker demand.

The shift reflects slower domestic consumption, tighter financial conditions from past rate hikes, and softer external demand. Businesses appear increasingly cautious, choosing to delay expansion plans and control labor costs as economic visibility narrows.

While wage growth remains relatively firm, it has started to stabilize rather than accelerate. That distinction is important for policymakers. A gradual cooling in employment conditions reduces the risk of a wage-price spiral, which was a major concern during the peak of inflation.

For the Reserve Bank of New Zealand, the rise in unemployment provides breathing room. It suggests that restrictive policy is working its way through the economy, dampening excess demand without triggering a sharp contraction. As long as unemployment increases in an orderly manner and inflation trends gradually lower, the central bank can justify keeping rates on hold rather than rushing into further tightening.

Source: Statistics New Zealand

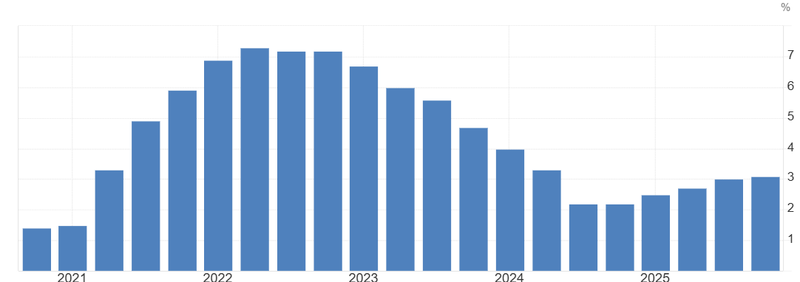

Inflation is still sticky

Inflation remains stubborn around 3%, slightly above the midpoint of the target range set by the Reserve Bank of New Zealand. While headline price growth has cooled significantly from its post-pandemic highs, the last phase of disinflation is proving more persistent especially in services, rents, insurance, and other housing-related costs. These components tend to adjust slowly and are closely linked to domestic wage dynamics, which explains why inflation is not falling as quickly as goods prices did.

Imported inflation has eased thanks to softer global supply pressures, but domestically generated inflation remains sticky. That distinction matters. It suggests that while external shocks are fading, internal cost structures are still adjusting.

This creates a delicate policy balance. Inflation is not low enough to justify easing yet rising unemployment and slowing growth make further rate hikes difficult to defend. Tightening too aggressively risks deepening the labor market slowdown, while easing too soon could allow inflation expectations to re-anchor above target.

Source: Statistics New Zealand

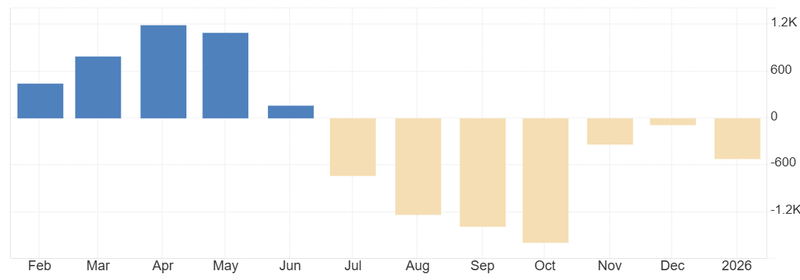

Trade balance and monetary policy expectations

New Zealand’s trade balance recorded a NZD -519 million deficit, underlining mounting external pressures on the economy. Softer export demand particularly from key Asian partners alongside volatile commodity prices has weakened the country’s external position. Given New Zealand’s reliance on agricultural and commodity exports, even modest shifts in global demand can materially affect trade flows and income growth.

A persistent trade deficit also exerts downward pressure on the New Zealand dollar, which complicates the inflation outlook. While a weaker currency can support exporters, it raises the cost of imports, potentially slowing the pace of disinflation. This dynamic makes the policy outlook more complex for the Reserve Bank of New Zealand.

Source: Statistics New Zealand

Rate hike in December

From a monetary policy perspective, the trade data reinforces expectations of a prolonged pause. As long as external demand remains fragile and the currency faces depreciation pressures, the RBNZ is unlikely to tighten aggressively. Markets currently see only a small probability of a rate hike before December, reflecting confidence that policymakers will prioritize economic stabilization over preemptive tightening.

However, if currency weakness begins feeding back into domestic inflation particularly through imported goods and fuel, the central bank could be forced to reconsider. For now, trade softness strengthens the case for patience, anchoring expectations that monetary policy will remain steady while the economy navigates external headwinds.

Source: RBNZ