DXY surges as fed tone turns hawkish

The US Dollar Index has pushed to its highest level since 11 months, as global markets shift back toward safety, the dollar is being supported by a combination of geopolitical tension, rising energy prices, and a more hawkish Federal Reserve.

US administration under Donald Trump taking a firmer stance and Iranian officials pushing back.

Inflationary consequences are becoming more visible. Elevated energy costs are feeding into private-sector PMI data.

Interest rate pricing now reflects a more hawkish outlook. While cuts were previously expected in 2026.

Geopolitics driving dollar strength

The primary catalyst behind the recent strength in the US Dollar Index is the escalating tension between the US and Iran, which is increasingly being viewed as a direct risk to global stability rather than a contained regional issue.

The situation has moved beyond short-term headlines. With the US administration under Donald Trump taking a firmer stance and Iranian officials pushing back, markets are beginning to price in a more prolonged period of uncertainty. This shift is important it suggests that the risk premium in global markets is becoming more structural rather than temporary.

In this environment, the dollar is benefiting on two fronts. First, it remains the world’s primary liquidity anchor, attracting flows during periods of uncertainty. Second, as energy prices rise on fears of supply disruption, the US gains relative strength compared to energy-importing economies in Europe and Asia.

Oil prices strengthen the dollar

Energy dynamics have further reinforced the strength of the US Dollar Index, with WTI crude oil holding firmly above $100 per barrel throughout March. That level matters not only for energy markets but for currency flows. As oil and LNG trade remains overwhelmingly priced in dollars, higher prices mechanically increase global demand for the currency. Each incremental rise in crude or gas prices forces importers to secure more dollars, tightening global dollar liquidity and lending structural support to DXY.

For emerging markets and large importers such as the Eurozone, this creates a reinforcing cycle. Weaker local currencies must be sold in greater quantities to fund energy imports, putting additional downward pressure on exchange rates while simultaneously pushing the dollar higher. The expansion of LNG trade particularly as countries seek alternatives to traditional pipeline supply has only amplified this effect, broadening the base of dollar demand across regions.

At the same time, the inflationary consequences are becoming more visible. Elevated energy costs are feeding into private-sector PMI data, where rising input prices in manufacturing and logistics point to emerging second-round effects. These pressures risk stalling, if not reversing, the disinflationary trend of recent years, leaving central banks in a difficult position and further underpinning the dollar’s relative strength.

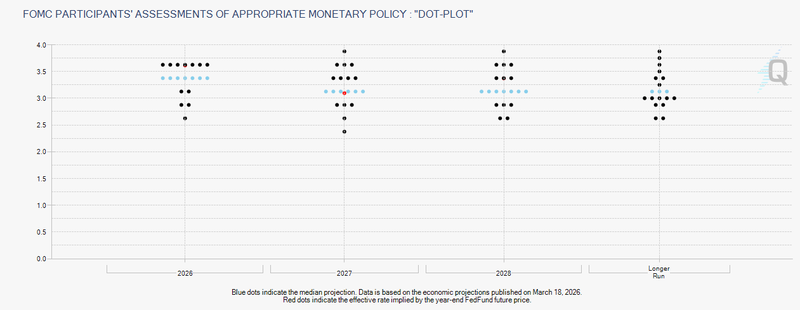

Fed policy turns more cautious and hawkish

The Federal Reserve is expected to hold interest rates steady in the near term, but the tone has clearly shifted. Jerome Powell has indicated that policymakers are prepared to wait and assess how the Iran conflict impacts inflation and growth.

Importantly, Powell suggested that the Fed can “look through” short-term shocks, but markets are not fully convinced. With labour market conditions still strong and inflation risks rising again, expectations are changing.

Interest rate pricing now reflects a more hawkish outlook. While cuts were previously expected in 2026, markets are now considering the possibility of a rate hike after June, particularly if inflation moves back toward or above 4%.

If current conditions persist ongoing geopolitical tension, elevated oil prices, and a cautious Federal Reserve, the dollar is likely to remain strong in the near term.

A further escalation in the Middle East or additional disruption to energy supply could push DXY even higher, as markets seek safety and liquidity. On the other hand, any clear signs of de-escalation or a sharp drop in oil prices could trigger a pullback.

Source: CME Group