US Dollar gains on geopolitical risk but eyes on Labour data for direction

The US dollar strengthened at the start of the week as escalating tensions in the Middle East drove investors toward safe-haven assets. Military actions involving the United States, Israel, and Iran over the weekend have intensified regional instability. Aerial strikes are continuing, with Iranian missiles reportedly targeting Tel Aviv and parts of the Persian Gulf.

Higher energy costs may reinforce inflation expectations.

The unemployment rate is projected to remain steady at 4.3%.

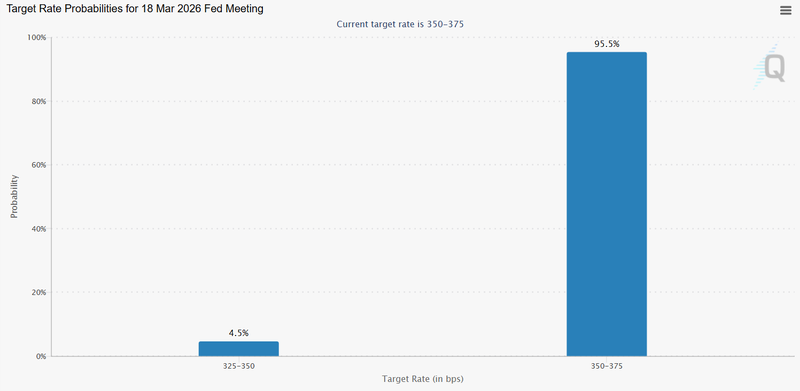

Markets are already pricing in a very high likelihood of no change.

Fed policy considerations

While geopolitical tensions are offering short-term support to the dollar, their real importance lies in how they influence Federal Reserve policy expectations. The most direct transmission channel is energy. If Middle East tensions continue to push oil prices higher, gasoline and transportation costs could rise in the coming weeks, potentially slowing the recent progress on disinflation.

For policymakers, the concern is not just headlining inflation but expectations. A sustained increase in energy prices can filter into broader pricing behavior from shipping and manufacturing to consumer sentiment. If businesses begin adjusting prices preemptively and households anticipate higher living costs, inflation expectations could become less anchored. That would complicate the Fed’s job at a delicate stage of the cycle.

On the other hand, Fed officials are well aware that energy shocks can be temporary. If tensions stabilize and commodity markets retrace, the inflation impact may fade quickly, allowing the central bank to maintain its current policy trajectory without reacting to short-term volatility.

March Interest Rate Decision in Focus

Federal Reserve’s March interest rate decision. Markets are overwhelmingly pricing in a hold, with policymakers expected to keep the federal funds rate unchanged as they assess both inflation progress and labor market stability.

The unemployment rate is projected to remain steady at 4.3%, reinforcing the narrative of a labor market that is gradually cooling but not deteriorating. That level suggests moderation rather than stress a key distinction for policymakers trying to engineer a soft landing.

If Friday’s Nonfarm Payrolls report confirms steady job creation and stable wage growth, it would solidify the case for maintaining current rates through March. A resilient employment backdrop, paired with inflation still hovering above the 2% target, leaves the Fed with little urgency to pivot toward cuts. In this scenario, the central bank can afford patience, keeping policy restrictive while monitoring further disinflation.

However, the tone could shift quickly if the data disappoints. A rise in unemployment above 4.3% or a meaningful slowdown in average hourly earnings would signal that labor conditions are softening faster than anticipated. Even if March still results in a hold, markets will likely begin pricing a higher probability of easing in the second quarter.

Source: Tradingeconomics

Policy expectations

A rate held in March remains the most probable outcome, with markets pricing in little chance of a change. The Federal Reserve appears comfortable keeping policy steady while assessing inflation trends, growth momentum, financial conditions, and global risks.

The focus now is less on the decision itself and more on the tone. If inflation risks including energy pressures remain elevated, the Fed may reinforce a “higher for longer” stance. If price pressures continue easing across sectors, expectations for cuts later in 2026 could slowly build.

March is unlikely to deliver a surprise move, but the forward guidance will shape market expectations for the months ahead.

Source: CME Group