Global markets tense as Trump weighs Iran action

Markets remain on edge as Donald Trump considers military action against Iran, global trade diplomacy stalls, and mixed economic signals from the UK, Japan, and China challenge central banks’ next moves.

Trump to decide within two weeks on US military involvement in Iran conflict

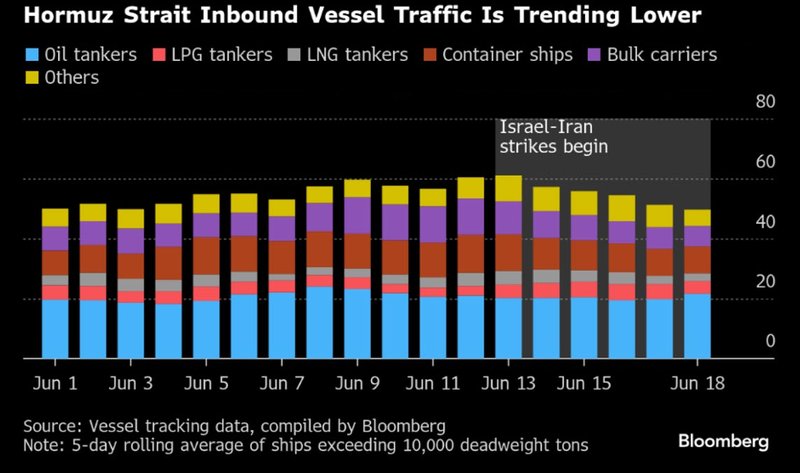

Strait of Hormuz traffic drops; oil tankers steady for now

EU and Canada show diverging trade paths with US amid tariff threats

UK retail sales plunge 2.7% in May; GfK sentiment shows fragile recovery

Japan core inflation hits 2-year high; China holds rates amid mixed data

Trump weighs military response as oil flows come under scrutiny

Donald Trump will decide within two weeks whether the US will support strikes against Iran, raising fears of a broader regional conflict. Satellite imagery reveals Iran is accelerating oil exports and stockpiling supplies, suggesting Tehran is bracing for potential disruptions. While container and bulk carrier traffic through the Strait of Hormuz has declined, oil tanker arrivals remain stable—for now—indicating that markets are anxiously monitoring developments without yet pricing in supply shocks.

The geopolitical stakes are high. Any US involvement could escalate the conflict dramatically, triggering sanctions, disrupting oil flows, and potentially prompting retaliatory attacks on regional energy infrastructure. Markets have not yet fully adjusted, but risk premia may rise sharply should tensions escalate.

Trade diplomacy sends mixed signals

While the EU signaled progress in trade talks with the US, Canada has warned it could raise tariffs on American steel and aluminum as early as July 21 if negotiations fail.

UK retail pain deepens despite rebound in sentiment

Retail sales in the UK fell sharply by 2.7% month-on-month in May, the worst drop since December 2023. The decline was led by a 5% fall in food store sales—marking the biggest plunge since May 2021—amid signs of subdued consumer spending and inflation fatigue. Non-food sectors also weakened, with retailers citing softer demand for clothing and home goods. The drop comes despite an uptick in consumer confidence to -18, the highest since December, according to GfK.

The dissonance between sentiment and spending reflects a still-fragile economic landscape. With BoE unchanged rates this week and inflation at 3.4%, the market is now leaning toward a potential move in August, though risks remain tilted toward later action if retail weakness persists.

Asia: Japan’s inflation puzzle and China’s cautious stance

In Japan, headline inflation eased to 3.5% in May—the lowest since November—but core inflation rose to 3.7%, its highest in over two years. A surge in rice prices, up more than 100%, underscores how selective price pressures are defying broader trends. The data may constrain the Bank of Japan’s policy flexibility ahead of the summer election, especially as wage growth remains tepid.

Meanwhile, the People’s Bank of China (PBoC) kept its loan prime rates steady after cutting them in May. The one-year LPR remains at 3.0%, and the five-year at 3.5%. Despite retail sales posting their strongest gain in 15 months, industrial output and new lending underwhelmed. The mixed data suggests the Chinese economy is still adjusting to US tariff headwinds, and authorities appear focused on preserving monetary ammunition while leaning on state banks to sustain momentum.

Markets remain in a precarious position. From rising tensions in the Middle East to stalled trade negotiations and uneven consumer demand, the global outlook is increasingly shaped by geopolitics and non-linear macro signals. With monetary policy paths diverging across major economies, investors face a summer of heightened uncertainty. The next decisive move may not come from a central bank—but from the corridors of political power.