Global stocks drop on geopolitical tensions; Fed may turn more restrictive

Global equity markets have retreated sharply amid escalating inflation risks and the potential for a broader economic impact resulting from the intensifying US-Israel-Iran conflict. Concurrently, the CME FedWatch Tool is signalling a significant shift in market expectations regarding future Federal Reserve interest rate decisions, where participants now pricing out previous forecasts for rate cuts.

Global stock markets fell in response to renewed inflationary pressures and the prospect of central banks adopting a more restrictive monetary stance should Middle Eastern hostilities persist.

The CME FedWatch Tool reflects a hawkish turn in market sentiment, with the probability of interest rate cuts during 2026 effectively eliminated.

Iraq has announced a cessation of oil production as domestic inventories reach overcapacity, further straining global energy markets.

Global stock markets drop as Middle East conflict persists

Global equity markets fell in tandem this week as the US-Israel-Iran conflict escalated into a wider regional crisis. Bilateral strikes between the primary combatants have impacted critical energy infrastructure in Qatar, Kuwait, the United Arab Emirates, Saudi Arabia, and Bahrain—nations not directly involved in the hostilities. This escalation followed a coordinated strike by US and Israeli forces on Iranian territory and energy assets.

Furthermore, global markets are contending with the growing risk that central banks may be forced to combat a potential resurgent inflation driven by soaring energy costs. Over the past month, Brent and WTI crude futures have surged by an average of 50%, while gasoline futures have climbed by 45%. Concurrently, various liquefied natural gas (LNG) benchmarks have spiked, intensifying concerns that monetary policy must shift toward further restriction.

Equity markets are currently facing a "double pressure" scenario: the threat of diminished global economic growth and the likelihood of hawkish central bank interventions to mitigate inflationary spikes.

At the market close, the S&P 500—the primary US benchmark—fell by 1.51% to 6,506 points. In Europe, the French CAC 40 dropped 1.82% to 7,665 points, the British FTSE 100 fell 1.44% to 9,918, the Spanish IBEX 35 decreased by 1.14% to 16,713, and the German DAX 40 depreciated by 2.01% to 22,380. Asian markets followed suit, with the FTSE China A50 decreasing by 0.86% to 14,598, the Hang Seng in Hong Kong dropping 2.08% to 24,725, and the Japanese Nikkei 225 sliding 3.38% to 53,372 points.

Fed could shift to restrictive stance amid renewed inflation risks

According to data from the CME FedWatch Tool, market expectations for the Federal Reserve’s upcoming monetary policy decisions have shifted fundamentally. For the past three months, the indicator had signalled expectations for two interest rate cuts during 2026; however, current data suggests that the market no longer anticipates any easing this year. This shift is largely attributed to the sharp spike in energy prices, which has reignited fears of long-term inflation should the conflict in the Middle East continue to escalate.

Iraq announces significant reduction in energy exports: Oil prices rise

As reported by Reuters, “Iraq has declared force majeure on all oilfields developed by foreign oil companies.” This drastic measure follows severe overcapacity issues in Iraqi storage facilities, which have reached their physical limits due to the closure of the Strait of Hormuz. The most critical implication is a substantial decrease in Iraqi oil exports, threatening severe disruptions to the global energy supply chain.

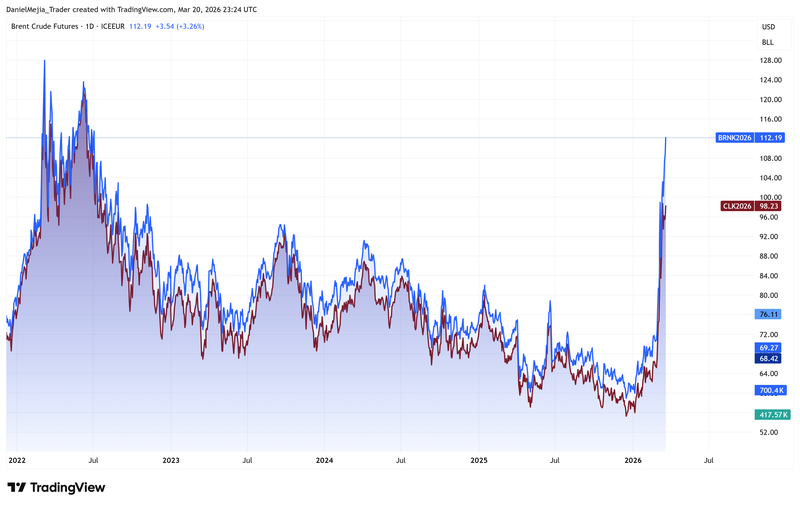

In response, the primary oil benchmarks, Brent and West Texas Intermediate (WTI), rose in tandem to their highest levels since July 2022. The Brent futures contract (BRNK6) climbed 3.26% to $112.19 per barrel, while the WTI futures contract (CLK6) appreciated by 2.80% to $98.23 per barrel. Additionally, gasoline futures (RBK6) increased by 4.33% to $3.23 per unit.

Figure 1. Brent and WTI Futures Contracts (2022-2026). Source: Data from the NYMEX and ICE-EUR Exchanges; Own analysis conducted via TradingView.