Micron rides AI demand while betting big on future growth

Micron Technology continues to position itself at the center of the AI-driven semiconductor cycle, delivering strong results while doubling down on long-term expansion. The company’s latest numbers highlight both current momentum and the scale of its ambitions in a market, increasingly shaped by data centers and artificial intelligence.

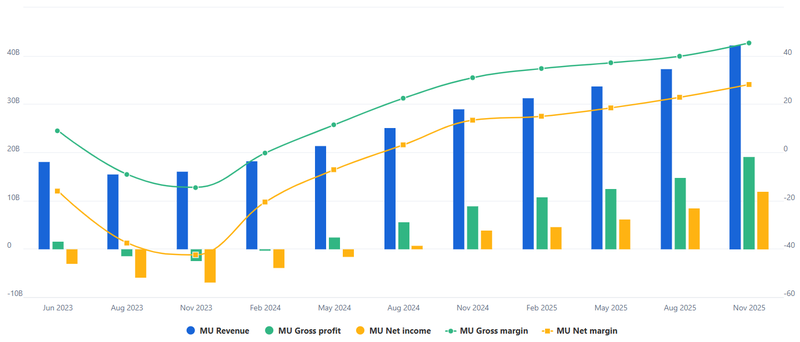

Micron reported adjusted earnings of $12.20 per share on $23.86 billion in revenue.

The company is planning to have more than $25 billion in capital expenditures in 2026.

Micron is not just riding the current wave it is investing heavily to shape the next one.

Strong results backed by AI demand

For the quarter ending February 26, Micron reported adjusted earnings of $12.20 per share on $23.86 billion in revenue, reflecting strong demand across memory products. The performance was largely driven by continued strength in high-bandwidth memory (HBM), which has become a critical component in AI infrastructure.

Looking ahead, guidance points to even stronger momentum. For the fiscal third quarter, Micron expects revenue of around $33.5 billion (± $750 million) and adjusted earnings near $19.15 per share, with gross margins projected at an impressive 81%. These figures suggest that pricing power remains firmly in the company’s favour, supported by tight supply and surging demand from hyperscale data center operators.

The board also approved a 30% increase in the quarterly dividend, raising it to 15 cents per share, signaling confidence in both cash flow and future earnings visibility.

Source: Fullratio

Capital spending signals long-term strategy

Beyond the headline results, the bigger story lies in Micron’s forward strategy. The company is planning more than $25 billion in capital expenditures in 2026, a clear indication that it sees the current demand environment as more than just a short-term cycle.

Key investments include new fabrication facilities in Boise, Idaho, and New York, with initial production expected between 2027 and 2030. These projects are aimed at expanding capacity for next-generation memory, particularly as AI workloads continue to scale rapidly.

This level of spending is significant, even by semiconductor industry standards. It reflects a deliberate move to secure long-term market share and ensure supply can meet what Micron expects to sustain demand growth over the next decade.

One of the clearest signals of this shift is the changing composition of demand. In 2026, data centre demand for DRAM and NAND is expected to exceed 50% of the total addressable market for the first time. This marks a structural change in how memory is consumed, with AI and cloud infrastructure now driving the majority of growth.

Micron’s focus on high-performance memory products, particularly HBM, places it in a strong position to benefit from this trend. As AI models grow more complex and require greater processing power, the need for advanced memory solutions is likely to increase further.

Technical outlook

solid upward trend, recently breaking out of a sideways range and moving into a new growth phase. After finding a steady floor around $363.81, the price pushed past the $435.82 level, which suggests the upward move is picking up speed toward the current high of $461.73. The RSI is at 64.25, indicating strong buying interest, though it hasn't reached the extreme levels that usually signal a pullback. However, because the price has moved so far above its previous support levels, it wouldn't be unusual to see a brief dip back toward the $435.00 area to test that old resistance. Overall, the technical setup looks positive as long as the price stays above that $435 mark, with the next major area of interest appearing near $480.00.

Source: Trading View

Growth story still building

Key question is whether current demand can be sustained. If AI adopts at its current pace, Micron’s aggressive expansion strategy could prove well-timed, allowing it to capture a larger share of a rapidly growing market.

However, the memory industry has historically been cyclical, and any slowdown in demand or oversupply from industry-wide expansion could impact pricing and margins. For now, though, the balance appears to favour continued strength.

Micron is not just riding the current wave it is investing heavily to shape the next one. If its assumptions about AI-driven demand hold, the company could remain a central player in the semiconductor landscape for years to come.