Oracle expands margins amid hyperscale investments

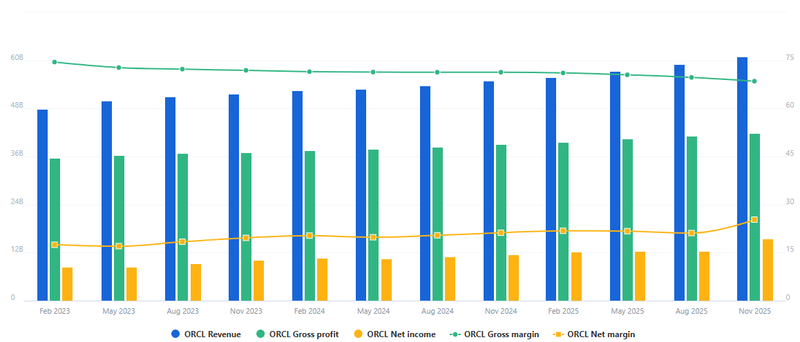

Oracle currently trades on a P/E of 27.6x, above the software industry average of 25.4x, net income increased 33% year-on-year and 24% sequentially, reflecting strong execution across cloud services, software, and enterprise solutions.

Net margin improved 20% from the prior quarter.

Estimates a reasonable P/E of 53.1x for Oracle.

If Oracle delivers consistent growth and margin improvement, the next earnings report could support a higher valuation.

Current price is viewed by many as a deep value opportunity relative to its AI growth trajectory.

Strong earnings

Oracle delivered a strong quarter, with net income up 33% YoY and 24% sequentially, supported by cloud, software, and enterprise growth. Revenue rose 11% YoY and 3.4% QoQ, while operating income increased 11% YoY and 2.8% sequentially. Margins remain healthy, with net margin up 20% QoQ and 19% YoY, reflecting disciplined cost management alongside recurring cloud revenue growth.

Investments in data centers, AI-enabled cloud services, and strategic partnerships continue to support long-term expansion. Oracle trades at a P/E of 27.6x, below the peer average of 53.5x, signaling potential upside if revenue momentum and margin gains persist. Looking ahead, the company’s next earnings report may reflect continued strength in cloud adoption and operational leverage, with margins and recurring revenue likely key drivers for investor confidence.

Source: Fullratio

Valuation perspective

Oracle currently trades at a P/E of 27.6x, slightly above the software industry average of 25.4x but well below the broader peer group average of 53.5x. This valuation gap reflects a mix of solid execution, strong cash flows, and investor caution around broader macro and tech sector risks. Simply Wall St’s “Fair Ratio”, which incorporates earnings growth, market capitalization, profit margins, and company-specific risk factors, suggests a reasonable P/E of 53.1x for Oracle. The difference between the current P/E and the Fair Ratio indicates potential upside if Oracle continues to deliver strong cloud adoption, expand its hyperscale partnerships, and maintain cost discipline. For investors, this means that while the stock is not deeply undervalued, there is room for a re-rating over the next few quarters, particularly if upcoming earnings reports confirm sustained revenue growth, margin expansion, and successful execution on strategic projects such as the Michigan data center and other enterprise initiatives.

Source: Fullratio

Strategic initiatives and upcoming earnings

Investments in hyperscale projects, including the Michigan data center, continue to be a central focus for Oracle. Investors and analysts are closely monitoring the company’s ability to deliver repeatable project structures and secure named partnerships, which could translate into predictable, long-term revenue streams. Effective execution in these initiatives would not only strengthen Oracle’s position in the competitive cloud market but also provide additional operational leverage, supporting margin expansion in upcoming quarters. If Oracle can demonstrate consistent results from these hyperscale projects, it may reinforce investor confidence and contribute to a potential re-rating of the stock, complementing ongoing growth in software and enterprise segments.

Upcoming earnings

Revenue growth momentum cloud and enterprise software sales maintain their current pace. A continuation of the ~11% YoY growth could reinforce confidence in Oracle’s recurring revenue model, if the net margin gains are sustainable, especially as hyperscale investments scale up.

Any updates on cloud project completions, partnerships, or pipeline visibility will likely influence expectations for the next quarter.

If Oracle delivers consistent growth and margin improvement, the next earnings report could support a higher valuation relative to its current P/E, bridging the gap toward the Fair Ratio of 53.1x. Conversely, delays in project execution or softer-than-expected cloud adoption may temper investor enthusiasm, keeping the stock in a cautious range.

Technical outlook

price is trading well below its major moving averages, with the 50-day average near $178 and the 200-day average around $227. This breakdown indicates a loss of intermediate-term momentum, though several indicators suggest the selling may be overextended. The Relative Strength Index (RSI) is currently hovering near 28–30, a level historically associated with "oversold" conditions that often precede a technical bounce or period of consolidation.

Oracle’s $523 billion RPO (backlog) as a massive economic anchor that could catalyze a sharp "mean reversion" once the current emotional sell-off exhausts itself. The consensus remains "Moderate Buy" among institutional analysts, with an average price target of approximately $290, suggesting that while the "falling knife" is still in motion, the current price is viewed by many as a deep value opportunity relative to its AI growth trajectory.

Source: Trading View