BoJ walks a tightrope between yen weakness and inflation risk

The policy tone in Japan is starting to shift, even if action has not followed yet. At the latest discussions, Kazuo Ueda, Governor of the Bank of Japan, made it clear that currency movements are becoming increasingly important for policy decisions.

Waiting too long could allow imported inflation to spread into wider parts of the economy.

BoJ is trying to judge whether inflation is temporary noise or the start of a more persistent trend.

BoJ is being pushed toward a more active role in managing inflation risk.

How fast should the BoJ move

The Bank of Japan is facing a much more complicated policy mix than it did earlier in the year. Inflation is no longer being driven only by domestic demand conditions or gradual wage improvement; it is now being pushed by external forces such as higher oil prices, a weaker yen, and rising import costs that feed directly into everyday prices. That is why the discussion inside the BoJ has started to shift from “whether tightening is needed” to “how quickly it should happen,” because waiting too long could allow imported inflation to spread into wider parts of the economy.

Why the debate is shifting

At the March meeting, BoJ policymakers openly debated the risk of falling behind the inflation curve if surging energy costs and yen weakness start feeding into wages and entrenched price expectations. This marks a departure from earlier caution board members highlighted how imported inflation from oil could combine with 3%+ wage demands in spring negotiations to create a self-reinforcing cycle.

Japan faces more than a one-off shock. Households are losing purchasing power as food and utility bills climb 5-7% year-on-year, while firms face margin pressure from 20% higher input costs since late 2025. Companies like Toyota and major retailers have already signaled plans to pass costs through more aggressively if energy stays elevated.

Core CPI hit 1.6% in February 2026 modest globally but uncomfortably close to the BoJ's 2% target after stripping out fresh food and energy. A repeat oil spike could easily push headline inflation toward 3%+ by summer, especially with the yen hovering near ¥155/USD, making every imported barrel sting more.

If Q1 wage deals exceed 3.2% the BoJ may view this as confirmation that inflation is broadening beyond imports. Markets are pricing a 65% chance of a May hike to 1.00%, but sustained oil above $110 could force an emergency move by April or back-to-back hikes in H2 2026 the first aggressive cycle since the 2000s.

The BoJ's judgment call is whether this is temporary noise or persistent trend. Policymakers leaning hawkish argue waiting risks needing 200bps total hikes by 2027; doves counter that premature action could tip Japan back into stagnation. The data by April meeting will likely settle it.

Policy timing

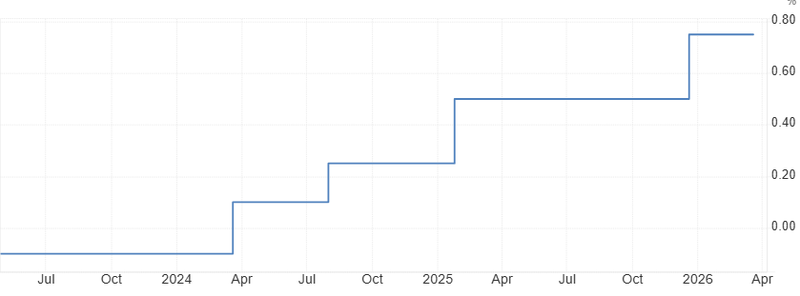

For now, the BoJ has left rates unchanged at 0.75%, but the tone has clearly become more hawkish and less patient. The problem is that the window for action is narrowing: if the BoJ waits too long and energy prices remain elevated, it may have to tighten more aggressively later; if it moves too early, it risks weakening a still-fragile recovery that has not fully stabilized across households and businesses. That is why a hike as early as May is now being discussed as a realistic possibility, especially if oil stays high and the yen keeps sliding. The market is therefore watching not just the next meeting, but the signals the BoJ sends about how much inflation pain it is willing to tolerate before it responds.

The BoJ is no longer debating tightening in theory; it is debating the pace, the timing, and how much damage it can afford to accept before acting. If oil remains elevated, the yen stays weak, and wage growth continues to improve, the central bank may conclude that moving sooner is safer than waiting for inflation to become more entrenched. If energy prices stabilize and growth softens, however, policymakers may decide they still have room to pause and gather more evidence. The key point is that Japan’s policy regime is changing: the old low-inflation mindset is fading, and the BoJ is being pushed toward a more active role in managing inflation risk.

Source: Bank of Japan