Inflation acceleration brings the Fed back to a 2021 scenario

Today’s March CPI report is expected inflation rising to 3.4% year on year from 2.4% in February, also for a 0.9% monthly gain, which would be the largest since the 2022 energy shock.

Today’s March CPI report is expected inflation to rise to 3.4% year on year from 2.4%.

Gasoline doesn't just stay "energy"; it becomes the cost foundation for 70% of PCE services.

Markets are pricing an average 70% probability of no rate cuts until December.

In the upcoming months a move toward 5% would not just delay cuts; it would change the entire policy conversation.

Inflation is no longer sticky it is being re-energized

Today’s March CPI report is expected inflation rising to 3.4% year on year from 2.4% in February, also for a 0.9% monthly gain, which would be the largest since the 2022 energy shock. That would not be a routine rebound. It would signal that disinflation has not only stalled, but that a new inflation impulse may already be built before the old one was fully absorbed.

The reason is not just domestic price pressure. It is the combination of still-firm core inflation and a fresh energy shock arriving at exactly the wrong time. Reuters reported that February core PCE, the Fed’s preferred underlying gauge, rose 3.0% year on year after 3.1% in January, which already showed inflation was running too hot before March’s oil surge fully fed through. In that sense, the CPI report is not arriving at a cooling inflation backdrop; it is arriving at a fragile one.

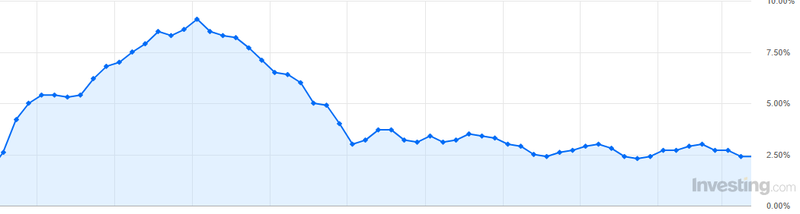

Source: Investing.com

Energy shock persistent inflation pressures

Oil is the immediate trigger, but the second-round effects are what embed inflation deeper into the system. The war with Iran drove crude sharply higher, pushing U.S. gasoline above $4 a gallon while Strait of Hormuz disruption fears spiked costs across freight, shipping, insurance, and core input prices. Even with a two-week ceasefire calming the worst headlines, the inflation pipeline doesn't empty overnight, it's primed and flowing.

Energy shocks always start at the pump, hitting consumers first, but they cascade fast: higher transport surcharges lift grocery bills, manufacturers pass on logistics hikes, and utilities flow into rent and services pricing. Gasoline doesn't just stay "energy"; it becomes the cost foundation for 70% of PCE services inflation through trucking, warehousing, and distribution chains.

The New York Fed's March survey captured it perfectly: one-year inflation expectations jumped to 3.4%, with gasoline outlooks surging 25%, signaling households aren't treating this as temporary. Once families budget $4+ gas, they cut discretionary spending, demand higher wages to offset it, and slow velocity which ironically can make core inflation stickier as firms protect margins amid softer demand.

If CPI prints above 3.4%, the Fed hardens fast

A higher-than-expected CPI print will likely reinforce the shift already visible inside the Fed. March meeting minutes showed growing openness among policymakers to the idea of further tightening if inflation proves persistent, even if the official baseline still points more toward limited easing than an immediate hike. A stronger CPI would support higher Treasury yields, a firmer dollar, and renewed pressure on equities, especially rate-sensitive sectors and companies that rely on cheap financing.

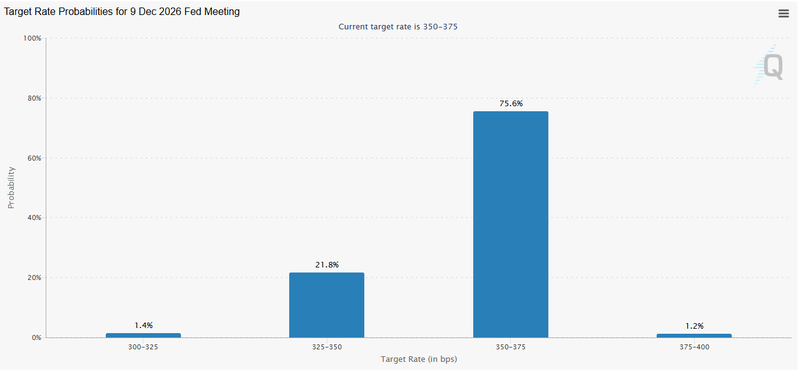

The key point is that the Fed does not need inflation to return to 2022-style extremes to become restrictive again. It only needs evidence that inflation is no longer improving. With current expectations around 3.4%, markets are pricing an average 70% probability of no rate cuts until December, and if CPI stays above that level for several months, that unchanged policy view shifts from base case to firm expectation.

Source: CME Group

If inflation keeps climbing toward 5%, the regime changes

A move toward 5% would not just delay cuts; it would change the entire policy conversation. At that point, the issue would no longer be timing, but credibility. The Fed would face a much harder trade-off between defending its inflation mandate and protecting growth, especially because the labour market is still resilient, with unemployment claims low and job creation holding up better than expected.

That creates a classic stagflation risk: higher prices, weaker real spending, and a central bank unable to ease. If CPI reaches 5% in the upcoming months, the Fed could likely deliver an insurance rate hike to regain control and anchor expectations. In that environment, the market would need to price a more defensive Fed, tighter financial conditions, and less support for risk assets. A softer CPI today could buy the Fed some time, but if inflation remains above 3.4% and continues drifting higher, higher-for-longer stops being a narrative and becomes the working assumption.