Fed faces a new test as war and oil reshape the rates expectations

The Federal Reserve is entering a far more complicated phase of its policy cycle. What once looked like a gradual move toward rate cuts has shifted into a wait-and-see stance, as rising oil prices and ongoing geopolitical tensions begin to reshape inflation expectations.

Fed expects real GDP to grow 2.4% in 2026 and 2.3% in 2027.

Concern for policymakers is not just the current level of inflation, but the risk that progress stalls.

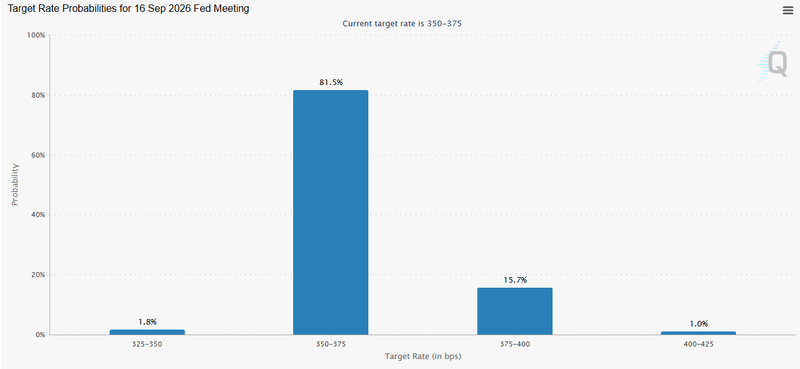

Pricing now reflects roughly a 10% chance of a rate hike across key meetings in mid-2026.

If oil prices stabilize and inflation continues to ease, the Fed could still move toward cuts later in the year.

Growth holding up, for now

Despite tighter financial conditions, the US economy continues to show resilience. The Fed now expects real GDP to grow 2.4% in 2026 and 2.3% in 2027, slightly stronger than earlier projections.

That strength gives policymakers room to pause. There is no immediate pressure to stimulate growth, and for now, the economy appears capable of absorbing higher rates without slipping into contraction.

But this resilience also complicates the picture. A stronger economy can keep demand elevated, which in turn makes it harder to fully bring inflation back to target, especially if new external pressures emerge.

Inflation cooling, but not comfortable

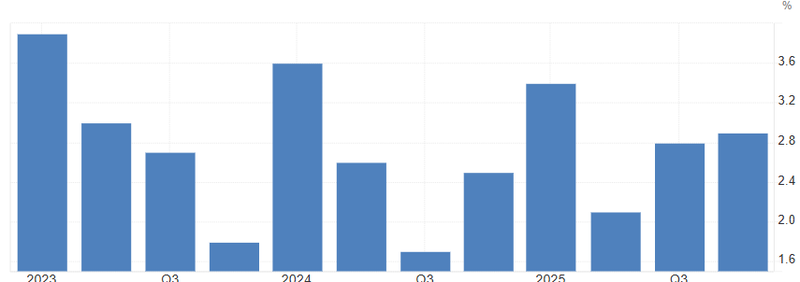

Inflation has come a long way from its 2022 highs, but it is still not fully under control. The latest data shows headline PCE inflation at 2.8% year-on-year, with core PCE at 3.0%, both still sitting above the Federal Reserve’s 2% target. On a monthly basis, price pressures have also shown signs of stabilizing rather than continuing a steady decline, suggesting that the last stretch of disinflation may be more difficult.

Digging deeper, goods inflation remains uneven. While some categories have cooled, others are holding firm, partly due to lingering effects from tariffs and supply-side adjustments. Services inflation, although gradually easing, is still elevated, reflecting wage pressures and steady consumer demand.

More recently, energy has re-emerged as a key driver. Oil prices have moved back above $100 per barrel amid supply disruptions tied to tensions involving Iran and the broader Middle East. This has already started to feed into fuel and transportation costs, which tend to pass through to broader prices with a lag.

The concern for policymakers is not just the current level of inflation, but the risk that progress stalls. After a period of steady declines, even a temporary rebound, especially driven by external factors like energy, can shift expectations and make it harder to anchor inflation near target.

Source: U.S. Bureau of Economic Analysis

Market expectations shift quickly

One of the biggest changes has been in how markets are pricing the Fed’s next moves. Earlier this year, expectations were firmly tilted toward two rate cuts in 2026, but that view has almost completely evaporated. In its place, markets are leaning toward no cuts, with even a small but growing probability of a 25-point hike roughly 10% at the June, July, or September meetings.

The real question now is why expectations have shifted so quickly. Headline PCE inflation remains at 2.8%, with core PCE at 3.0%, still above the Fed’s 2% longer-run goal. The spike in oil prices recently trading above $100 per barrel due to Middle East tensions and disruptions around Iran has added to near-term inflation risks. This has led markets to wonder whether the Fed’s stance reflects genuine concern about persistent inflation, the geopolitical shock to energy markets, or simply a cautious interpretation of Jerome Powell’s messaging.

Powell has repeatedly emphasized that policy will remain data-dependent, noting that while inflation has eased from mid-2022 highs, upside risks remain, particularly from energy costs and goods inflation linked to tariffs. Analysts suggest the Fed is not making a mistake but rather signaling that any premature easing could risk inflation overshooting again.

Source: CME Group

The path ahead, narrow and uncertain

Fed is choosing patience. Holding rates steadily allows time to see whether the current rise in inflation expectations is temporary or something more persistent.

But the margin for error is shrinking. If oil prices stabilize and inflation continues to ease, the Fed could still move toward cuts later in the year. If not, the conversation may shift again this time toward keeping rates higher for longer or even tightening further.

What makes this cycle different is that the Fed is no longer just responding to domestic data. It is navigating a global environment where geopolitics, energy markets, and supply disruptions are playing a much larger role.

The direction of policy is no longer a straight line. It is becoming conditional, reactive, and increasingly dependent on forces outside the Fed’s control.