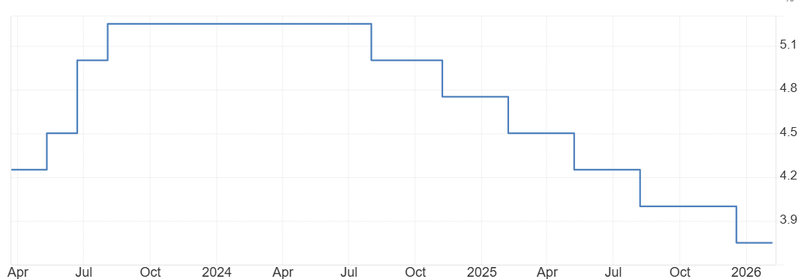

Bank of England set to hold rates

Attention is firmly on the upcoming decision from the Bank of England, where markets widely expect policymakers to hold interest rates at 3.75%. After an aggressive tightening cycle over the past two years, the central bank now faces a more delicate balance: inflation is easing, but economic momentum is clearly slowing.

UK recorded a trade surplus of £3.92 billion in January 2026.

Inflation has eased to 3%, moving closer to the Bank of England’s target.

Direction of policy will likely depend on which side of the economy becomes more dominant.

Mixed signals from the economy

The latest data highlights just how uneven the picture has become. On the external side, the UK recorded a trade surplus of £3.92 billion in January 2026, a sharp turnaround from a £4.34 billion deficit in the previous month. It also marks the first surplus since September 2024, suggesting that demand for UK exports has held up better than expected, or that imports have weakened alongside softer domestic consumption.

However, the strength in trade contrasts with a much weaker domestic backdrop. GDP stalled on a month-over-month basis in January, missing expectations for a 0.2% expansion and following a modest 0.1% increase in December. The details are more concerning than the headline figure. The services sector, which dominates the UK economy, showed no growth, with administrative and support service activities contracting by 2.3%, acting as the largest drag.

This combination points to an economy that is losing momentum beneath the surface, even if headline figures have yet to fully reflect it.

Source: Office for National Statistics

Labour market and inflation trends

The labour market is beginning to show clearer signs of strain as tighter financial conditions work their way through the economy. The unemployment rate has risen to 5.2%, its highest level since 2021, reflecting a gradual slowdown in hiring and a more cautious approach from businesses facing higher borrowing costs and softer demand. Vacancy levels have also been easing, suggesting that firms are becoming less aggressive in expanding their workforce. While the situation is not yet critical, the steady rise in unemployment points to a cooling in overall economic activity.

At the same time, inflation has eased to 3%, continuing its downward trend and moving closer to the Bank of England’s target. The moderation has been supported by softer energy prices and a gradual slowdown in goods inflation, although services inflation remains relatively sticky. This easing gives policymakers more room to pause after an extended period of rate hikes. However, with inflation still above target and underlying pressures not fully resolved, the central bank is likely to remain cautious, limiting how quickly it can shift towards rate cuts.

What markets are watching

Taken together, the data supports the case for a pause. Holding rates at 3.75% allows the Bank of England to assess how previous tightening continues to filter through the economy without adding further pressure in the near term.

The direction of policy will likely depend on which side of the economy becomes more dominant. If inflation continues to fall and growth remains weak, the conversation could gradually shift towards rate cuts later in 2026. On the other hand, if price pressures prove more persistent, policymakers may be forced to keep rates elevated for longer than markets currently expect.

The focus shifts from the decision itself to the tone of the guidance. Any signal that the Bank of England is becoming more concerned about growth could reinforce expectations of future easing. Conversely, a cautious stance on inflation would suggest a longer period of restrictive policy.

The current environment feels like a transition phase rather than a clear direction. The UK economy is no longer overheating, but it is not yet contracting sharply either. That leaves the central bank holding steady for now, while remaining prepared to adjust as economic conditions evolve through the year.

Source: Bank of England