ECB moves closer to June hike as oil shock reshapes the inflation debate

The ECB is moving closer to a possible rate hike at its June 11 meeting as the oil shock pushes inflation risks higher.

A rate hike as early as June 11 is now being treated as a serious possibility rather than a tail risk.

Shock is different from the 2022 energy crisis because it is more global in nature.

Christine Lagarde’s future, reports and speculation about a potential early exit.

The ECB is no longer just waiting

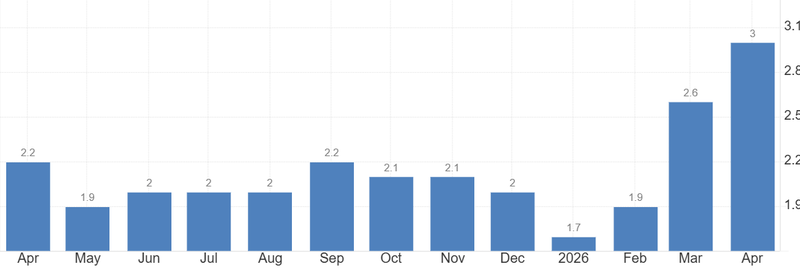

The European Central Bank is moving closer to a major shift in policy as the war-driven oil shock pushes inflation risks back to the center of the debate and rose to 3.0%. After months in which markets had focused mainly on when the ECB might eventually cut rates, the conversation has turned in the opposite direction. A rate hike as early as June 11 is now being treated as a serious possibility rather than a tail risk.

The ECB had been trying to hold policy steady while waiting for clearer evidence on inflation, growth and wages. But higher energy prices have made that holding pattern harder to defend. If the oil shock continues to feed through transport, production costs and household bills, the central bank may be forced to act even as the Eurozone economy remains weak. This is the uncomfortable policy mix now facing Frankfurt: inflation pressure is rising, but growth is not strong enough to make the decision easy.

Source: EUROSTAT

Nagel’s tone shows the debate has shifted

Bundesbank President Joachim Nagel captured that change clearly, saying ECB rate hikes are becoming “increasingly likely” as elevated energy prices move through the economy. That matters because Nagel’s comments are not just another hawkish warning. They reflect a broader shift inside the Governing Council toward treating the oil shock as a potential inflation problem, not just a temporary disruption.

The key issue is whether energy prices remain isolated or begin to affect broader inflation expectations. Central banks can usually look through short-term energy volatility. They have far less room to ignore it when households and companies start behaving as if higher prices will last.

Oil has turned the ECB’s old policy story upside down

The ECB’s earlier story was easier to understand. Inflation had been moving closer to target, growth was fragile, and the next major debate was supposed to be about how long rates should stay restrictive before cuts could begin.

The oil shock has complicated that

ECB Chief Economist Philip Lane warned that a global energy shock tied to the Iran war could require rate hikes if inflation pressures prove persistent. He also noted that this shock is different from the 2022 energy crisis because it is more global in nature, meaning Europe cannot simply rely on cheaper external supply to cushion the hit.

That is the deeper concern. If higher energy costs are hitting Europe, Asia and global manufacturing supply chains at the same time, the inflation impulse may be harder to contain. Imported goods, transport costs and industrial inputs could all become more expensive together.

Markets are having to reprice the ECB path

Markets had become used to thinking about ECB policy through the lens of cuts. That assumption is now being challenged. A Reuters poll conducted in May showed most economists expecting the ECB to raise rates in June, with many also seeing the possibility of another hike later in the year as war-led inflation pressure builds.

The reprice is not happening because the Eurozone economy suddenly looks strong. It is happening because inflation risk is becoming harder to dismiss.

That distinction matters. A rate hike driven by strong demand would usually signal confidence in the economy. A rate hike driven by an oil shock is different. It reflects a central bank trying to defend price stability in a weaker growth environment. That is a much less comfortable backdrop for markets, households and governments.

Lagarde rumors add another layer of uncertainty

The policy debate is also unfolding while questions continue to circulate around Christine Lagarde’s future. Reports and speculation about a potential early exit have created an additional layer of uncertainty around the ECB’s leadership, even though no final succession decision has been confirmed. Lagarde said in April that leaving early was not currently an option for her, while separate reporting has suggested that discussions around her future have not fully disappeared.

For markets, the leadership issue matters because the ECB is entering a more politically sensitive phase. Raising rates into weak growth is never easy. Doing so while energy prices are already squeezing households makes the communication challenge even harder.

If the ECB appears divided on both policy and leadership, investors may start demanding a higher risk premium around European assets.