European natural gas sparks supply fears

Qatar's Ras Laffan suspension and a choked Strait of Hormuz have delivered the most disruptive supply shock to global gas markets, European natural gas futures rising more than 5% to trade above €56 per megawatt-hour levels not seen in over three years. In just two days, prices have surged roughly 60%, a move that underscores how fragile the global energy balance remains.

Europe imported roughly 15–17% of its LNG from Qatar.

EU’s plan to eliminate Russian gas imports entirely by the end of 2027.

ECB will look beyond the headline figure. Energy-driven increases are often treated as temporary supply shocks.

Europe problem

EU gas storage levels are currently near 62–65% full, according to recent industry estimates lower than the same period last year when inventories were closer to 75%. After winter withdrawals, the bloc was expected to rebuild stocks steadily through the summer to meet the EU’s 90% storage target before November.

If Qatari LNG cargoes remain offline for weeks rather than days, that restocking path becomes far less certain. Europe imported roughly 15–17% of its LNG from Qatar in 2024. Losing that supply, even temporarily, tightens an already competitive global market.

China, the world’s largest LNG importer at over 70 million tonnes annually, has reportedly urged all sides to ensure safe maritime transit. That response highlights how interconnected the LNG trade has become. When one major export hub pauses, Asia and Europe immediately compete for alternative cargoes.

Source: IEA

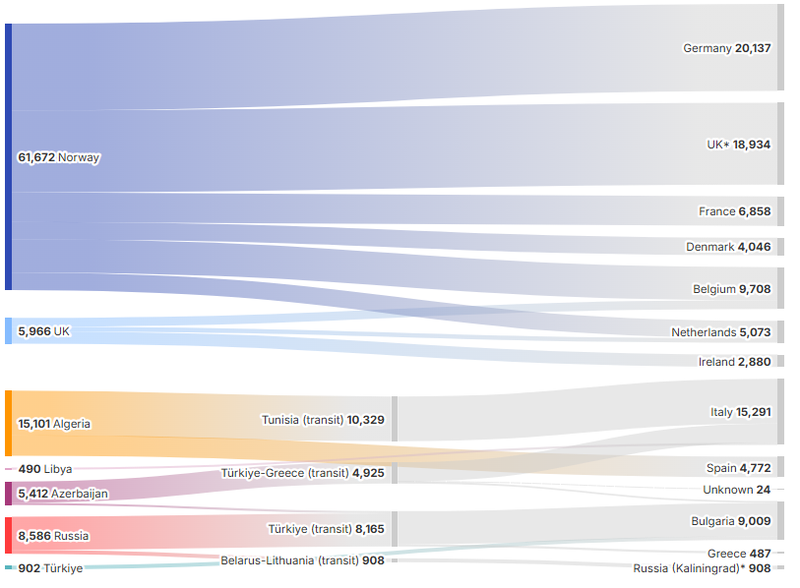

Europe new supply map under strain

Since cutting reliance on Russian gas following the invasion of Ukraine, the European Union has redrawn its supply map. Norway has emerged as the bloc’s largest pipeline supplier, accounting for about 55% of EU pipeline imports in the first half of 2025. Algeria follows at roughly 19%. LNG particularly from the United States and Qatar has filled much of the remaining gap.

Yet the EU’s plan to eliminate Russian gas imports entirely by the end of 2027 now faces a real-world stress test. While official policy remains firm, Russian pipeline flows via Türkiye have gradually increased in recent years. Meanwhile, Lithuania continues to allow transit of Russian gas to Kaliningrad under a contract with Gazprom that expires in December 2025.

If LNG shortages persist and TTF prices push toward €65–€70/MWh, political debates within Europe could intensify. Energy security, especially ahead of winter, has a way of reshaping priorities.

Source: IEA

Energy risks intersect the ECB’s path

Inflation is sitting just under the European Central Bank’s 2% target. On paper, that gives policymakers some breathing room. Inflation is no longer running above target, and the broad disinflation trend remains intact.

However, the ECB will look beyond the headline figure. Energy-driven increases are often treated as temporary supply shocks. If gas prices spike but core inflation, which excludes energy and food, continues to lower, the central bank may choose to look through short-term volatility rather than react immediately.

The real concern would be second-round effects. If higher energy costs start feeding into wages and services prices, inflation could become sticky again. In that case, even though inflation is currently below 2%, forward-looking risks could complicate policy decisions.

Source: EUROSTAT