Gold fails its haven test — now markets are questioning central bank demand

Gold’s sharp pullback since the Iran conflict began has exposed a familiar truth about the metal: in moments of stress, it can behave less like a sanctuary and more like a source of liquidity. That pattern is not new. What is new is the possibility that central banks — the dominant buyers of the past several years — may begin using parts of their gold stockpiles to fund rising energy and defense costs, potentially changing the market’s structure from a one-way accumulation story into a more bala

Gold has fallen about 15% since the Iran conflict began.

The pullback has weakened its image as an immediate geopolitical hedge.

Central banks may increasingly view gold as a usable reserve asset, not just a long-term store of value.

That could create a more balanced market, with official buyers and sellers both active.

Gold is failing its latest haven test

Gold’s retreat since the outbreak of the Iran conflict has unsettled one of the market’s oldest assumptions: that the metal automatically rises when geopolitical risk intensifies. Instead of behaving like a pure haven, gold has dropped sharply, even as war, shipping disruption and inflation fears dominate headlines.

That may feel counterintuitive, but it is not especially unusual. In moments of deep market stress, gold often acts as a liquidity valve. Investors sell what they can, not necessarily what they want. During both the 2008 financial crisis and the March 2020 Covid shock, gold initially fell before later recovering strongly.

The logic is simple. Gold is liquid, widely held and easy to monetize. When markets turn disorderly, it becomes one of the first assets investors can sell to raise cash. That makes it useful, but it also means it does not always behave like a clean shelter in the first phase of a crisis.

The bigger shift may be happening at central banks

The more important change now may not be the price drop itself, but what central banks do next.

Over the past four years, official institutions have been among the most powerful buyers in the gold market, helping drive prices higher and reinforcing the metal’s strategic status inside reserve portfolios. But rising energy costs, higher defense spending and growing fiscal strain in some countries are now creating a new incentive: using part of those holdings as a financial buffer.

That would not mean gold is losing relevance. Quite the opposite. It would mean central banks are treating it exactly as reserves are supposed to be treated — as assets that can be mobilized when national balance sheets come under pressure.

The piggy bank effect is becoming more visible

For countries under acute energy stress, especially those with limited domestic resources, the temptation is obvious. If gold has risen sharply over several years, selling a portion of it to meet urgent import or budget needs can look more rational than politically painful domestic austerity or aggressive borrowing.

That is what gives the current moment a different texture from past corrections. Gold is no longer only being accumulated as a hedge against sanctions, dollar dependence or geopolitical fragmentation. In some cases, it is starting to look like an emergency-use reserve — a piggy bank rather than a museum piece.

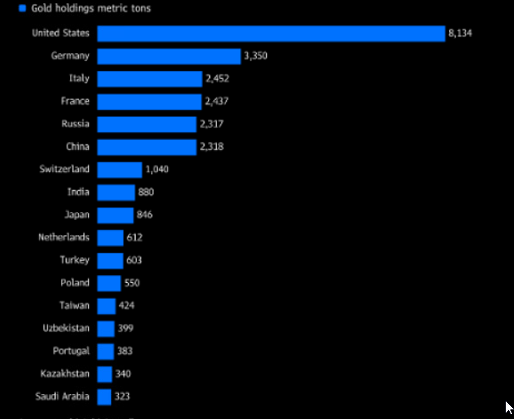

Central banks still hold enormous gold reserves, and those holdings have become a much more meaningful part of the global market than they used to be. If even a modest share of those institutions moves from pure buying toward tactical selling or collateral use, the market dynamic changes.

Source: Bloomberg

A one-way market may be giving way to two-way flows

For much of the recent rally, the story was relatively straightforward: central banks bought, private investors followed, and gold benefited from a persistent demand floor. That flow helped create the impression that official demand was almost structurally one-directional.

Now that assumption looks less safe.

Some countries may continue buying, especially at lower prices. Others may decide to sell selectively, pledge gold as collateral, or simply pause purchases while dealing with domestic pressures. The result would not necessarily be a collapse in gold demand, but a market that looks more balanced and less speculative than it did during the strongest phase of last year’s rally.

That matters because a more balanced market tends to trade differently. Upside momentum becomes harder to sustain, price swings become more sensitive to policy choices, and the metal starts behaving less like a pure conviction trade and more like a reserve asset with real-world uses.

Gold’s long-term role is not disappearing

None of this means gold’s strategic case is broken. Central banks still hold it because it remains politically neutral, globally recognized and outside the direct control of any single foreign government. That logic has not disappeared, especially in a world that continues to fragment geopolitically.

But the market may be entering a new phase in which gold is valued less as an untouchable symbol of safety and more as a usable financial resource. That is a subtle but important distinction.

Gold is still a store of value over time. It is just not always a straight-line haven in real time. And if central banks begin acting on that reality more openly, the metal may trade less like a sacred shield and more like what it has always also been: a reserve asset meant to be used when the pressure gets real.