Silver caught between structural demand and macro pressure

Silver is moving through a complicated phase. On one side, the long-term story remains strong, driven by technology, clean energy, and industrial demand. On the other hand, short-term market behaviour is being shaped by geopolitics, oil prices, and stronger dollar factors that are pulling attention away from metals.

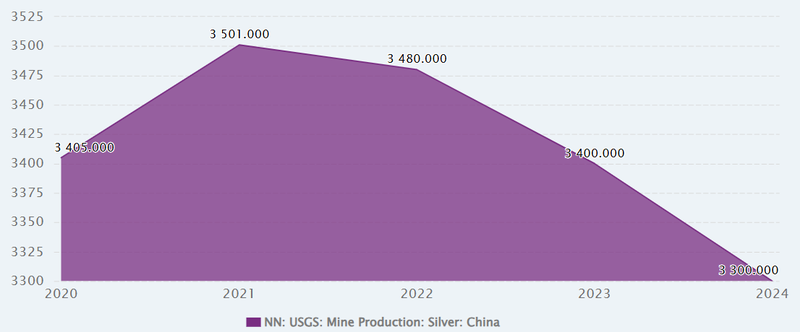

China produces roughly 3,000–3,300 metric tons of silver annually.

Electricity demand is expected to rise sharply, potentially reaching 8–11% of national usage by 2035.

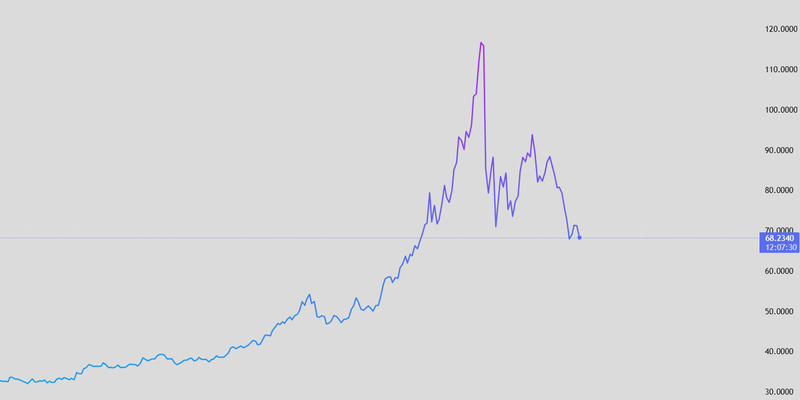

Silver is still struggling to fully express its fundamentals in price. Ongoing tensions involving Iran and the run‑up in oil prices.

China tightens control

A potentially major structural shift is unfolding in China the world’s largest silver refiner and a key exporter. The Ministry of Commerce recently listed 44 companies authorized to export silver for 2026–2027, replacing a previously open export system.

China produces roughly 3,000–3,300 metric tons of silver annually, accounting for about 20% of global refined supply. Export restrictions could tighten liquidity in global markets, especially since the Shanghai Futures Exchange inventories have already declined by nearly 15% since mid-2025.

Controlled export framework is controlled to reduce flexibility and make global supply more policy sensitive. If domestic demand rises particularly from the Chinese solar and electronics sectors fewer tons may reach the international market. While not an immediate shock, this regulatory move signals a gradual shift toward supply rigidity, which can amplify price responses to demand spikes later this decade.

With Shanghai Futures Exchange inventories already down by about 15% since mid‑2025, the market is heading into this new regime with less of a buffer than usual. A controlled export framework reduces flexibility and makes global supply more policy‑sensitive. If domestic demand continues to rise particularly from solar and electronics manufacturers fewer tons may actually leave China. It is not a sudden shock, but it is a clear shift toward supply rigidity that could amplify price moves the next time demand spikes.

Source: CEICDATA

AI, data centers, and energy

On the demand side, the long-term picture remains strong. In Australia, the government has introduced a new framework for expanding data centers, requiring tech companies to invest in renewable energy and infrastructure.

With more than 200 data centers already operating, electricity demand is expected to rise sharply, potentially reaching 8–11% of national usage by 2035. This directly supports demand for silver, given its unmatched electrical conductivity.

From solar panels to AI-driven computing systems, silver is becoming increasingly important. As adoption accelerates, demand is not just growing, it’s becoming more embedded in the global economy.

Market pressure and the Dollar

Silver is still struggling to fully express its fundamentals in price. Ongoing tensions involving Iran and the run‑up in oil prices have shifted the market’s attention toward energy and away from metals. When oil spikes, capital often rotates toward energy plays and into the US dollar, which is still seen as a macro hedge.

Higher oil prices also muddy the inflation outlook, supporting a stronger dollar and adding another layer of pressure on silver and other precious metals priced in USD. They have also altered the interest‑rate narrative: where markets were previously pricing in two rate cuts for this year, expectations have shifted toward no cuts at all, with even a non‑trivial 16% probability of a rate hike in September now on the table. That repricing keeps real yields under upward pressure, something that typically weighs on non‑yielding assets like silver.

There is a liquidity side to this as well: in periods of geopolitical stress, investors frequently move up the safety ladder, favoring cash, short‑term paper, or very liquid benchmarks. Silver, which sits awkwardly between an industrial metal and a defensive asset, tends to get caught in the middle. Since early 2026, ETF holdings in silver have edged lower – roughly a 3% drop – a sign that some investors are de‑risking or waiting for clearer macro signals before re‑engaging. Since the war started, silver has dropped more than 20%, underlining how far market pricing has diverged from the metal’s improving structural demand story.

As long as the dollar stays firm, rate‑cut expectations remain priced out, and geopolitics keep volatility high elsewhere, silver may continue to lag its own structural story. The long‑term demand trends are still building underneath the surface; for now, though, the macro tide is setting the pace.

Source: Trading View