US market caught between rates and risk

From March 18 through to the end of the month, flows turned decisively negative, with a sustained stretch of net outflows and several days exceeding $10bn. This was not simply profit-taking it aligned with a broader repricing of macro risk.

The tone shifted again at the start of April. Bullish inflows have returned.

The underlying driver of this volatility is the interaction between geopolitical risk and monetary policy expectations.

The more probable outcome is continued volatility in flows. Inflows on dips, outflows on macro shocks.

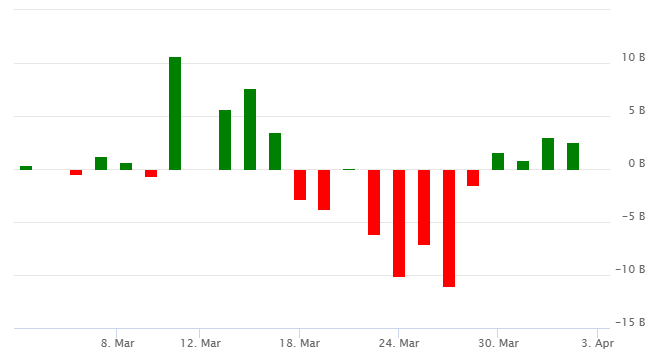

VOO from conviction to hesitation

VOO’s flow profile over the past month reflects a clear shift in investor behaviour from steady accumulation to more conditional positioning. Early March still carried the hallmarks of passive conviction, with large inflows, including a surge of over $10bn in a single session, reinforcing the idea that equity exposure via low-cost index funds remained the default allocation. At that stage, weakness in the S&P 500 was being treated as an opportunity rather than a warning.

That narrative, however, broke down mid-month. From March 18 through to the end of the month, flows turned decisively negative, with a sustained stretch of net outflows and several days exceeding $10bn. This was not simply profit-taking it aligned with a broader repricing of macro risk, particularly around rates and geopolitical tensions. What stands out is the persistence: this was not a one-off liquidation, but a consistent withdrawal of capital, suggesting a shift in positioning rather than a temporary adjustment.

The tone shifted again at the start of April. Bullish inflows have returned, but in a different form more measured and selective. Rather than aggressive accumulation, investors are stepping back in cautiously, treating dips as opportunities while remaining sensitive to macro signals. The behaviour has changed: conviction has given way to conditional participation.

Source: ETFdb

Caught between geopolitics and rates

The underlying driver of this volatility is the interaction between geopolitical risk and monetary policy expectations. Rising tensions have pushed oil prices higher, reintroducing inflation concerns just as markets were beginning to price a more benign path. For investors, this creates an uncomfortable backdrop. Higher energy prices act as a tax on consumption and corporate margins, while also feeding into inflation expectations.

At the same time, rate expectations have shifted materially. The earlier narrative of imminent easing has been replaced by a “higher-for-longer” reality. Real yields remain elevated, and the opportunity cost of holding equities, especially at relatively high valuations has increased. This is where VOO becomes particularly sensitive. As a broad market ETF, it sits directly at the intersection of growth expectations and discount rates. When yields rise or cuts are pushed out, flows tend to weaken. When those pressures ease, inflows return. The result is a push-and-pull dynamic rather than a clear trend.

Flows become tactical, not structural

The era of uninterrupted passive inflows appears, at least temporarily, to be giving way to a more reactive regime. Investors are no longer simply allocating they are adjusting.

If geopolitical tensions stabilize and oil prices retreat, inflation concerns could ease, allowing rate expectations to shift back toward gradual cuts. In that scenario, VOO could see a renewed wave of inflows, supported by both valuation stability and improved risk sentiment. However, if energy prices remain elevated and inflation proves sticky, the Federal Reserve is likely to maintain a restrictive stance. That would keep real yields high and limit the upside for equities, particularly through the discount-rate channel.

The more probable outcome is continued volatility in flows. Inflows on dips, outflows on macro shocks. VOO remains a core holding for many portfolios, but the behaviour around it has changed. What was once automatic is now conditional.