Europe inflation jumps, China PMI expands, US job openings decline

March data highlights a diverging global landscape: while European headline inflation surged to 2.5%, fuelled by energy price volatility, the US labour market continued its multi-year cooling trend with a notable dip in job vacancies. Amidst these shifts, China’s manufacturing sector returned to expansionary territory, offering a signal of industrial recovery for an economy long hampered by sluggish domestic demand.

European Headline inflation rose from 1.9% to 2.5%, primarily driven by escalating energy costs following heightened geopolitical tensions between the US, Israel, and Iran.

Chinese manufacturing Purchasing Managers' Index (PMI) moved into expansion in March, sparking optimism for a recovery in an economy constantly constrained by weak domestic consumption.

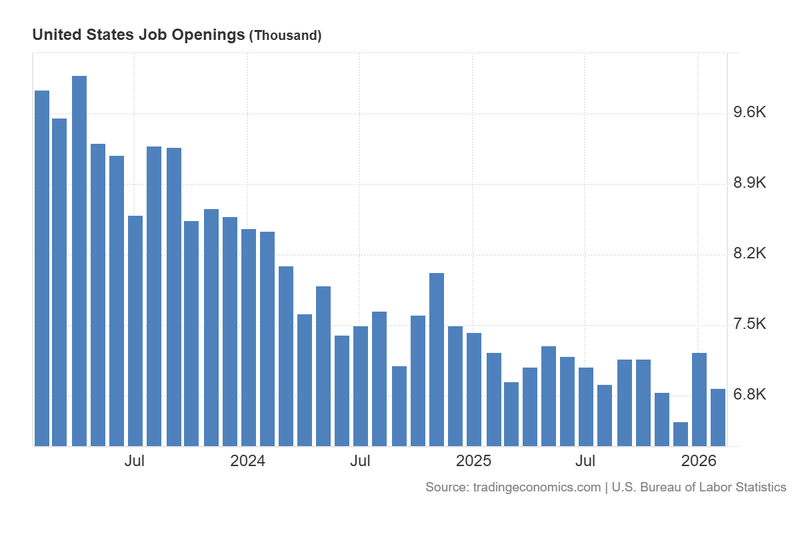

US JOLTs job openings fell below analyst estimates in February, maintaining a consistent downward trajectory established over the last four years.

European inflation jumps, though figures remain slightly below estimates

According to data from Eurostat, headline inflation rose from 1.9% in February to 2.5% in March. Although this represents a significant acceleration in consumer prices, the figure arrived slightly below analyst forecasts of 2.6%. This current inflation rate is the highest recorded since January 2025 and was primarily driven by energy costs, which surged 4.9% on an annual basis due to the ongoing conflict involving the US, Israel, and Iran in the Middle East. Analysis from Trading Economics indicates that the most pronounced accelerations occurred in Germany (rising from 2% to 2.8%), France (from 1.1% to 1.9%), and Spain (from 2.5% to 3.3%).

Conversely, European core inflation—which excludes volatile energy and unprocessed food prices—decelerated from 2.4% to 2.3% during the same period. Economic debate is now centred on whether rising energy costs will be absorbed by European firms or if workers will demand higher wages to offset the loss of purchasing power. Both scenarios present an upside risk to the inflationary outlook.

In response to the data, the EUR/USD pair appreciated by 0.80% to $1.1555. Elevated inflation typically compels central banks to adopt a more restrictive monetary stance. The European Central Bank (ECB) has indicated its readiness to pivot toward a more hawkish position should energy prices continue to exert upward pressure on headline figures. According to reports from Reuters, markets now anticipate that the ECB could implement up to three interest rate hikes in 2026, with the initial increase potentially occurring in April or June.

Chinese manufacturing PMI expands beyond forecasts

Data from the National Bureau of Statistics (NBS) of China revealed that the manufacturing PMI increased from 49.0 in February to 50.4 in March, surpassing the analyst estimate of 50.1. This reading marks the first expansionary movement since March 2025, as the indicator climbed above the neutral 50.0 threshold. Regarding the broader economic outlook, this improvement in the manufacturing sector provides a glimmer of hope for a potential recovery, particularly as the "Asian giant" has struggled to stimulate growth and domestic consumption in recent years.

Market reaction was notably positive: the FTSE China A-50 index rose by 1.23% to 14,715 points, while the Hang Seng index appreciated by 1.76% to reach 25,191 points.

US JOLTs job openings fall short of expectations

According to the US Bureau of Labour Statistics (BLS), JOLTs job openings declined from 7.24 million in January to 6.88 million in February, missing the analyst consensus of 6.92 million. While the decrease is not transformative in isolation, it confirms a persistent downward trend in vacancies that first emerged in 2022. Over recent months, the US labour market has displayed mixed signals, alternating between periods of significant easing and sporadic indicators of resilience. Market participants are now shifting their focus to the comprehensive monthly labour report due from the BLS on Friday, 3 April, where a marginal improvement in non-farm payrolls is anticipated.

Regarding the market response, US equity indices advanced in tandem, largely supported by speculative optimism regarding a potential resolution to Middle Eastern tensions. The S&P 500 increased by 2.91% to 6,528, the Dow Jones Industrial Average rose by 2.49% to 46,341, and the Nasdaq 100 jumped 3.43% to 23,740 points.

Figure 1. US JOLTs Job Openings (2025-2026). Source: Data from the Bureau of Labour Statistics; Figure obtained from Trading Economics.