Europe stocks rebound on hopes of Middle East de-escalation

The conflict in the Middle East has experienced a momentary de-escalation, leading to a potential normalisation of energy prices. Consequently, European equity markets closed with significant recoveries, while major crude oil benchmarks recorded substantial depreciations. Concurrently, Chinese trade data for February significantly exceeded market expectations, signalling a robust reconfiguration of international trade flows.

Major oil benchmarks depreciated by more than 11% following renewed optimism regarding a possible de-escalation in the Middle East.

European indices closed with prominent gains, as the prospect of stable energy prices provides a tailwind for the Eurozone economy, which remains heavily reliant on oil and gas imports.

Chinese exports rose by 21.8% while imports increased by 19.8% year-on-year; both indicators represent the highest growth levels observed in the last four years.

European indices recover at market close on hopes of Middle Eastern de-escalation

European stock markets advanced in tandem following comments from US President Donald Trump regarding the Middle East conflict. In recent weeks, military exchanges involving the US, Israel, and Iran have caused severe disruptions to oil and natural gas supply chains, stoking global concerns over price stability. European nations are particularly sensitive to energy price spikes given their status as net energy importers.

Following a period of sustained depreciation, European equities staged a considerable recovery after president Trump declared that "the war is nearing its end." Furthermore, according to reports from Reuters, the Trump administration has indicated the possibility of lifting oil sanctions against Russia. While these declarations have yet to be formalised, the information has opened the door for a potential normalisation of global oil supply chains.

In response, the energy markets saw a sharp correction: the Brent futures contract (BRNK26) depreciated by 11.28% to $87.80 per barrel, while the WTI futures contract (CLJ26) fell by 11.94% to $83.45 per barrel. However, the Strait of Hormuz remains closed, and bilateral hostilities between the involved parties persist. Future movements in energy prices remain contingent upon developments in the US-Israel-Iran standoff, which continues to be characterised by conflicting objectives and rhetoric.

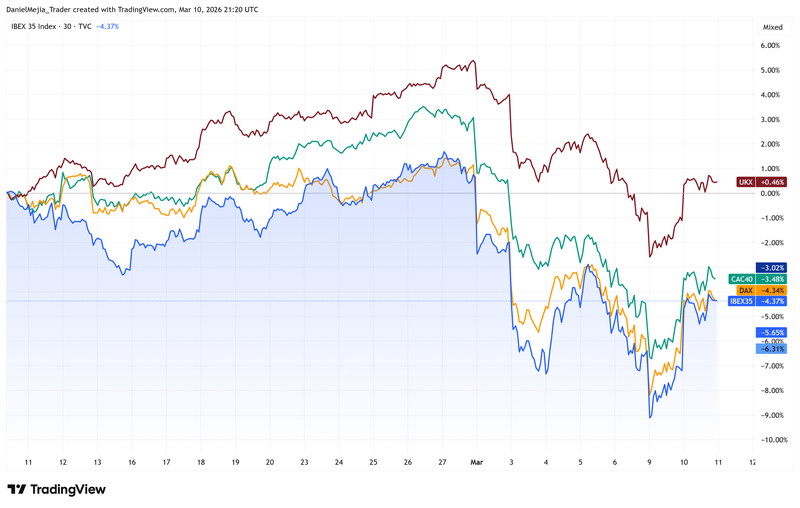

Supported by the prospect of energy price stabilisation, major European indices closed firmly in the green. The IBEX 35 appreciated by 3.05% to 17,445 points, the FTSE 100 rose by 1.59% to 10,412, the DAX 40 increased by 2.39% to 23,968, and the CAC 40 gained 1.79% to close at 8,057 points.

Figure 1. IBEX-35, FTSE-100, DAX-40, and CAC-40 indices (over the last month). Source: Own analysis conducted via TradingView.

Chinese exports and imports surpass expectations

According to data released by the General Administration of Customs of China, year-on-year (YoY) exports surged by 21.8% in February, vastly exceeding the 7.1% forecast and the previous reading of 6.6%. Similarly, YoY imports rose by 19.8% during the same period, well above the market consensus of 6.3% and the prior release of 5.7%. Both figures represent the highest levels since February 2022, serving as a significant indicator of strengthening economic performance.

Data from Trading Economics highlights that the most substantial increases in Chinese outbound trade were directed toward ASEAN countries (+29.4%), Australia (+29.4%), Taiwan (+28.7%), the European Union (+27.8%), South Korea (+27%), and Japan (+8.9%). Conversely, US imports from China declined by 11%. On the import side, China saw increased volumes from South Korea (+35.8%), Japan (+26.5%), Taiwan (+19.2%), ASEAN nations (+12.9%), and the European Union (+11.7%), while imports from the United States dropped by 26.7%.

These trade indicators follow Monday’s inflation data, which showed the consumer price index (CPI) accelerating from 0.2% in January to 1.3% in February—its highest level since February 2023. Buoyed by these signs of economic acceleration, Chinese equity indices closed with notable gains; the FTSE China A50 rose by 1.36% to 14,710, while the Hang Seng index appreciated by 2.50% to 25,900 points.