Trump ultimatum hits stocks; US durable goods down, Canada PMI contracts

Western equity markets are under significant pressure as the deadline for President Trump’s ultimatum to Iran regarding the Strait of Hormuz approaches. Concurrently, US durable goods orders retreated in February amidst broader economic instability, while Canada’s Ivey PMI slumped into contractionary territory, driven by escalating energy costs and persistent supply chain disruptions.

The nearing expiry of the US ultimatum concerning the Strait of Hormuz, coupled with reports of strikes within Iran, threatens global energy security and has heightened fears of stagflation.

US durable goods orders fell by 1.4% in February, underperforming expectations and signalling a deterioration in consumer and corporate confidence.

The Ivey PMI dropped to 49.7 in March, entering contractionary territory as rising energy prices and logistical bottlenecks impact the domestic economy.

Western stocks retreat amid concerns over Trump's Iranian deadline

Western stock markets closed lower as geopolitical tensions between the United States and Iran intensified. US President Donald Trump has issued an ultimatum demanding the reopening of the Strait of Hormuz—a critical maritime chokepoint through which approximately 20% of the global oil and natural gas supply transits—by the end of Tuesday, 7 April. Iranian officials have stated that while the nation is prepared for a diplomatic resolution, it remains equally ready for intensified conflict if deemed necessary.

According to reports from Reuters, Iranian media has indicated that military strikes have escalated, damaging essential infrastructure including railway and road bridges, an airport, and a petrochemical plant. In response, Tehran has declared that it may target key infrastructure in neighbouring Gulf states, stoking fears of a broader regional conflict and severe energy supply chain disruptions.

Even in the event of a successful negotiation to reopen the Strait, energy-related headwinds are expected to persist. The US Energy Information Administration (EIA) has cautioned that fuel prices may continue to rise for several months following a potential cessation of hostilities. This volatility has weighed heavily on equity valuations; a sustained spike in energy costs could drive global inflation higher, compelling central banks to adopt more restrictive monetary stances and potentially triggering a period of stagflation—characterised by high interest rates and economic stagnation.

Regarding the market reaction, the Dow Jones Industrial Average in the US fell by 0.18%, whereas the S&P 500 and Nasdaq 100 managed marginal gains of 0.08% and 0.04%, respectively. European markets experienced sharper declines: the French CAC 40 lost 0.67%, the UK FTSE 100 dropped 0.84%, and the Spanish IBEX 35 fell 0.64%. Germany’s DAX 40 saw the steepest decline at 1.06%, reflecting the continent's acute dependence on energy imports from the Middle East and Asia.

US durable goods orders drop below expectations amid economic instability

Data released by the US Census Bureau revealed that durable goods orders contracted by 1.4% month-on-month in February, significantly underperforming the anticipated 0.5% decline and following a prior contraction of 0.5%. This updated indicator represents the third consecutive monthly decrease, suggesting that consumer and business appetite for long-term capital investments is cooling amidst heightening economic uncertainty.

Analysis from Trading Economics suggests the primary driver of this contraction was the transportation equipment sector, which fell by 5.4% in monthly terms. Notably, orders for non-defence aircraft and parts plummeted by 28.6%, further highlighting the impact of current instability on capital-intensive industries.

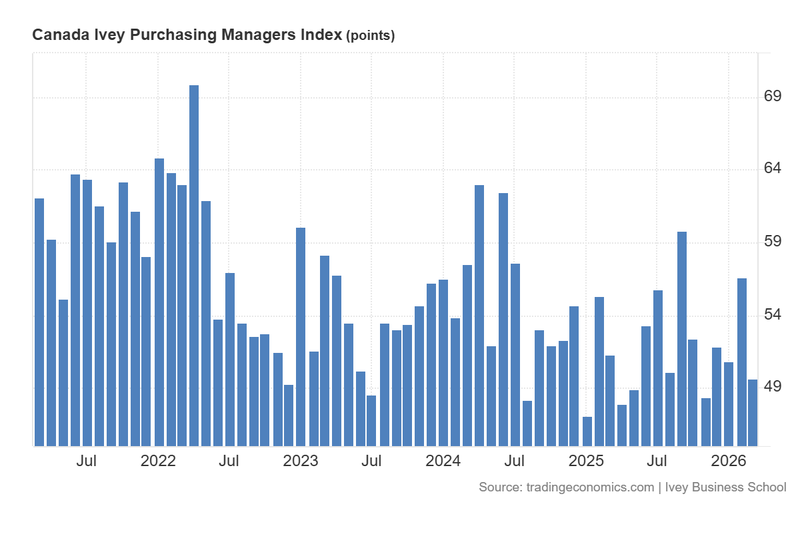

Canadian Ivey PMI enters contraction territory amid rising energy costs

According to the Ivey Business School, Canada’s Purchasing Managers' Index (PMI) plummeted from 56.6 in February to 49.7 in March, falling below the critical 50.0 threshold into contractionary territory. This result underscores a sustained five-year downward trend in the Canadian indicator.

The Ivey report highlighted a sharp spike in the price index—rising from 63.4 in February to 75.7 in March—while the employment index saw a marginal increase from 49.4 to 51.1. Conversely, inventories retreated from 57.2 to 49.4, and supplier deliveries slowed from 45.2 to 38.8. This deterioration coincides with heightened geopolitical instability and growing concerns regarding the global economic fallout from the US-Israel-Iran conflict, which has severely disrupted energy supplies and inflated prices.

Figure 1. Canada Ivey PMI (2021-2026). Source: Data from the Ivey Business School; Figure obtained from Trading Economics.