US retail sales, manufacturing PMI, and ADP beat forecasts as stocks climb

US equity indices advanced in tandem following a series of robust economic data releases. Retail sales growth accelerated, the ISM Manufacturing PMI reached its highest level since August 2022, and the ADP employment report surpassed analyst consensus. Despite these gains, market participants remain cautious regarding the potential inflationary impact of a sharp spike in energy prices.

US retail sales rose from 3.2% to 3.7% on a year-on-year basis, bolstered by significant gains in department stores, clothing, and the health and personal care sectors.

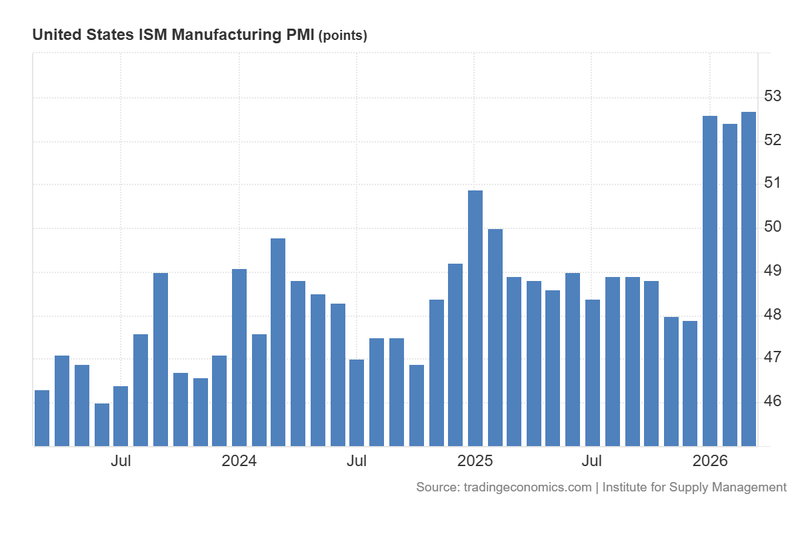

The ISM Manufacturing PMI reached 52.7 points, its highest reading since August 2022, indicating a sustained expansion supported by strong production figures.

The ADP National Employment Report indicated a slight moderation in private payroll growth to 62,000; however, the figure remained notably above analyst forecasts.

US mortgage rates have reached 6.57%—the highest level since August 2025—amid fears that persistent inflation may compel the Federal Reserve to maintain a restrictive "higher for longer" policy stance.

Robust economic data supports daily recovery in equity markets

A series of influential economic indicators released today provided a significant tailwind for the US stock market, reinforcing confidence in the resilience of the domestic economy.

The US Census Bureau reported that retail sales exceeded analyst expectations with a monthly increase of 0.6%, outperforming the forecasted 0.5%. Consequently, year-on-year (YoY) performance climbed from 3.2% in January to 3.7% in February—the strongest reading since October 2025. According to analysis from Trading Economics, the most substantial gains were recorded in department stores (+3%), health and personal care (+2.3%), and clothing (+2%). Reuters reports suggest this uptick in consumer spending was partially fueled by the seasonal distribution of tax refunds. Looking ahead, however, analysts suggest that domestic consumption may soften during the first half of the year due to global geopolitical volatility, though a recovery is anticipated should energy prices stabilise.

Simultaneously, the Institute for Supply Management (ISM) revealed that the Manufacturing PMI rose from 52.4 in February to 52.7 in March, marking its highest level since August 2022. The report highlighted a sharp increase in production (rising from 53.5 to 55.1). In contrast, new orders saw a slight deceleration (from 55.8 to 53.5), while the employment component remained in contraction territory, easing from 48.8 to 48.7. Notably, purchasing managers cited growing risks stemming from the escalating conflict between the US, Israel and Iran. This Middle Eastern instability has caused significant disruptions to energy supply chains, driving oil prices up by approximately 50% in March and impacting the global shipment of aluminium and fertilisers.

In the labour market, Automatic Data Processing (ADP) Inc. reported that private payroll additions moderated slightly from 66,000 in February to 62,000 in March. Nevertheless, the result comfortably beat the analyst estimate of 40,000. While the ADP report is traditionally viewed as a precursor to the official non-farm payrolls data (released on the first Friday of each month), its predictive accuracy has been inconsistent in recent months during periods of economic contraction.

Following these releases, major benchmarks climbed as expectations for the US economic outlook improved. The S&P 500 index rose by 0.72% to 6,575 points, the Dow Jones Industrial Average gained 0.48% to reach 46,565, and the Nasdaq 100 appreciated by 1.18% to close at 24,019 points.

Figure 1. US ISM Manufacturing PMI (2023–2026). Source: Data from the Institute for Supply Management; Figure obtained from Trading Economics.

US mortgage rates reach highest level since August 2025 amid inflationary risks

According to the Mortgage Bankers Association, the average rate for a 30-year fixed-rate mortgage increased by 14 basis points to 6.57% for the week ending 27 March—as reported by Reuters. This represents the highest level since August 2025, posing a significant challenge to a real estate sector that relies on more accommodative lending conditions to sustain growth. This surge is largely attributed to the rise in long-term Treasury bond yields, which serve as the primary benchmark for mortgage pricing.

US government bond yields have climbed by approximately 40 basis points since the intensification of Middle Eastern tensions on 28 February. The combination of rising inflation risks and the possibility of the Federal Reserve adopting a more restrictive "higher for longer" stance, has pushed yields upward. Consequently, mortgage rates have followed suit, increasing by approximately 48 basis points over the same period.