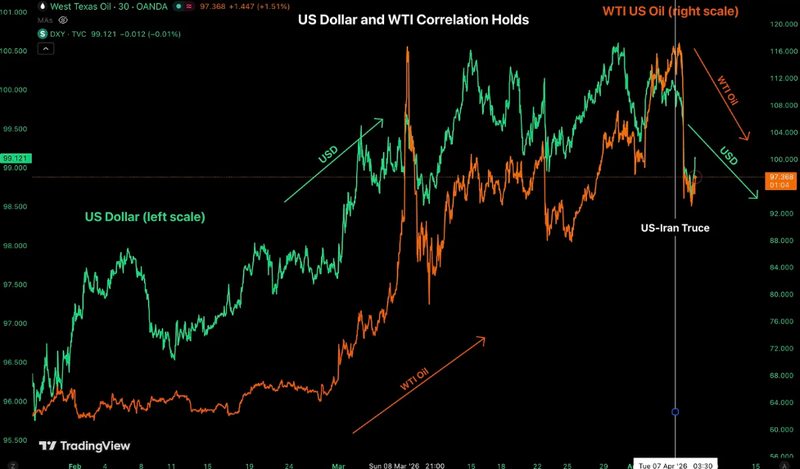

DXY from energy bid to policy test

The US dollar’s strength over the past two months has been less about domestic growth and more about global stress. The surge in crude at one point doubling from mid-February highs reignited the classic petrodollar dynamic: energy priced in dollars forces importing economies to convert local currency into USD.

Oil pulling back after ceasefire headlines, the mechanical demand for dollars tied to energy flows is easing.

The dollar’s next move depends less on oil and more on inflation data.

This places the dollar in a low-conviction zone around 99.00, with support near 98.70 and resistance around 99.50–100.50.

The petrodollar trade drove the surge, but it may have peaked

The US dollar’s strength over the past two months has been less about domestic growth and more about global stress. The surge in crude at one point doubling from mid-February highs reignited the classic petrodollar dynamic: energy priced in dollars forces importing economies to convert local currency into USD, creating a mechanical bid. The near disruption of the Strait of Hormuz, which handles roughly 20% of global oil flows, intensified that effect. Countries rushed to secure supply, hedge exposure and fund higher import costs, reinforcing demand for the dollar.

At the same time, positioning amplified the move. Markets entered this period with meaningful short-dollar exposure, which was quickly squeezed as oil surged and inflation expectations repriced higher. The dollar rally, therefore, was not purely fundamental, it was also technical and flow driven.

But that impulse may now be fading. With oil pulling back after ceasefire headlines, the mechanical demand for dollars tied to energy flows is easing. The dollar is no longer being bid by urgency, but reassessed based on sustainability.

Source: MarketPulse

From energy-driven strength to Fed-dependent direction

As the energy shock stabilizes, the dollar’s direction shifts back toward monetary policy. Minutes from the Federal Reserve’s March meeting showed that while rate cuts remain the base case, some policymakers are considering the possibility of further tightening if inflation proves persistent. That shift matters.

The dollar’s next move depends less on oil and more on inflation data. Markets are now focused on upcoming CPI, expected around 3.3% year-on-year. A higher print would reinforce the “higher for longer” narrative, supporting yields and extending dollar strength. A softer print, however, could expose how much of the recent rally was driven by temporary factors.

Technical outlook

DXY is no longer in a clean trend but in a compression phase that reflects deeper macro indecision, a clear break of the January uptrend, yet price has not followed through to the downside. Instead, it is holding above a longer-term rising trendline while being capped by descending resistance, forming a tightening triangle. This places the dollar in a low-conviction zone around 99.00, with support near 98.70 and resistance around 99.50–100.50. The structure suggests not weakness, but a pause market are waiting for a catalyst.

That catalyst is inflation. If upcoming data prints higher, reinforcing a “higher for longer” stance from the Federal Reserve, yields would likely rise and DXY could reclaim resistance, turning the recent breakdown into a false move and pushing back toward 100–101 and beyond. Conversely, softer inflation would expose the downside, with a break below 98.70 opening a move toward 97 and confirming a broader trend shift. In essence, the dollar is no longer driving markets it is reacting to them, with inflation data now determining direction.

Source: Trading View