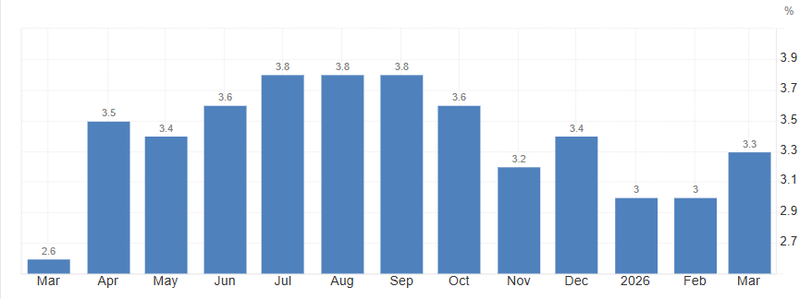

The BoE felt the first impact of the Iran war as inflation rose to 3.3%

Inflation rose to 3.3% in March from 3.0% in February, according to official data showing the first impact on prices from the Iran war which the Bank of England worries could lead to a return of persistently high inflation.

Inflation rose to an annual rate of 3.3% in March from 3.0%.

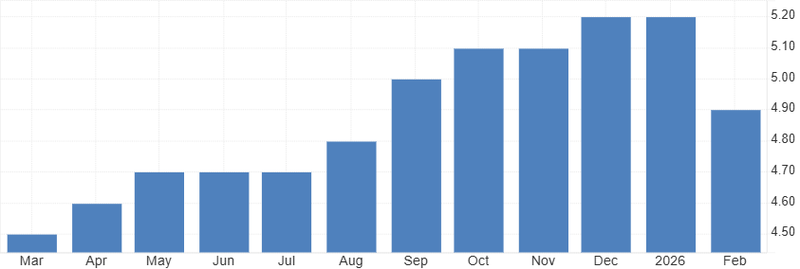

The recent drop on unemployment rate to 4.9% is not because of stronger work environment but because of economic inactivity.

No change in 2026 and resuming the rate cuts on 2027.

Rising inflation meets slowing growth

Inflation rose to an annual rate of 3.3% in March from 3.0%, before the U.S. Iran tension began the expectations of BoE was likely to be close to the 2% target in April, but the increase in inflation due the energy price shock changed the prediction of the BoE to inflation rise to 3.5% in the middle of 2026, and that it would peak to 4% too.

Stagflation is the serious concern of the BoE as they’re caught between higher energy prices and flatlining domestic economy, the latest tensions and the delay on reaching a peace deal is pressuring the oil supplies and prices that forcing inflation to rise again to 3.3% with expectations to see second round of spikes on April print.

On the other hand, economic growth has slowed with expectations for 2026 to be between 0.7% - 0.8% with he higher for longer tone that leaves the BoE in a pressure position of that high interest rate to control inflation and the risk of triggering recession again.

Source: Office for National Statistics

A fragile in labour market

The other main pressure facing the BoE is the labour market as the job vacancies drops to the lowest level since 2021 and businesses are scaling back recruitments in response to higher costs and economic uncertainty; on the same time the annual wage growth slowed to 3.6% and its lowest level since 2020.

The recent drop on unemployment rate to 4.9% is not because of stronger work environment but because of economic inactivity and that creates a tight market where businesses struggle to find the balance between finding staff on the current average wages that will force them to hike wages and the acceptance of higher for longer interest rate that is shaking businesses.

The dilemma of the BoE is keeping the interest rate high to reduce business investment and hiring to lower wage pressure and bring inflation down again, but the dilemma is if they hike rate while the economy already stagnating the risk will be a hard landing with higher unemployment.

Source: Office for National Statistics

BoE holds steady, but stagflation risks rise

Governor Andrew Bailey has stated the Bank will not "rush" to hike rates despite the energy shock, but the risk of this statement is the risk of stagflation with an extra pressure from the labour market with vacancies at a five-year low.

The uncertainty that’s happening inside the BoE makes the equation of balancing between rising inflation and weak labour market is the hard thing, what’s crystal known is that April meeting the interest rate will be on hold, but the middle of 2026 expectations to see 1 to 2 hike rates as an insurance hike to control the inflation shock, but policy makers such as Sarah Breeden and Alan Taylor said they have a high bar for hiking rates but prefer to wait for more data if the energy prices will go deep in the wages and price spirals.

However, if we see fall on the energy price back to the average of $65-$70, it would remove the primary driver that pushing inflation but the problem is from the supply market as energy will not react to peace deal or ceasefire but will react when the supply chain and production flow is back to normal, and that’s what is making the BoE cautious about a second round effect after even the war is end, that they will wait for several months after the cool on the energy prices, and to see a no change in 2026 and resuming the rate cuts on 2027.