ECB faces a new inflation challenge

The European Central Bank is once again at the center of market attention as inflation in the euro area shows signs of reacceleration. Preliminary data for March put headline inflation at 2.5%, while the increase is not dramatic, the drivers behind it are more concerned.

If headline inflation rises above 4.5% by June, the ECB could be forced into a 25-basis-point hike.

Markets now assign an 84% chance of at least one rate hike in 2026.

European natural gas prices are doubling to around €45/MWh.

Lagarde signals readiness, but not urgency

The escalation between the US and Iran has sent shockwaves through energy markets, with Brent crude surging above $120 per barrel and European natural gas prices doubling to around €45/MWh. This sudden spike is feeding directly into eurozone inflation, reversing months of gradual disinflation. The impact is already visible across the data German producer prices jumped 7.2% year-on-year in March, while French core goods inflation reached 4.1%, highlighting how quickly energy costs are filtering through the economy.

At the policy level, Christine Lagarde has struck a careful tone. The deposit rate remains at 3.25%, and for now, there is no immediate move. Still, the message is clear the ECB is watching closely. If these energy-driven pressures begin to embed into broader inflation, the central bank is ready to respond. Current thresholds remain just below critical levels, with core inflation at 2.7%.

The risks are increasingly skewed markets are pricing roughly a 55% chance that tensions persist, potentially disrupting 8–12% of global oil supply through Q3. If headline inflation rises above 4.5% by June, the ECB could be forced into a 25-basis-point hike as early as July, a scenario currently priced at around 40%. That path would likely push rate cuts further out, possibly into 2027, while slowing growth toward 0.5% and lifting bond yields above 3%.

On the other hand, if oil stabilizes near $130 and keeps core inflation closer to 3.2%, the ECB may lean toward a “higher for longer” stance, potentially lifting rates toward 3.50%. Either way, the margin for policy flexibility is narrowing, and energy markets are once again dictating the direction of monetary policy.

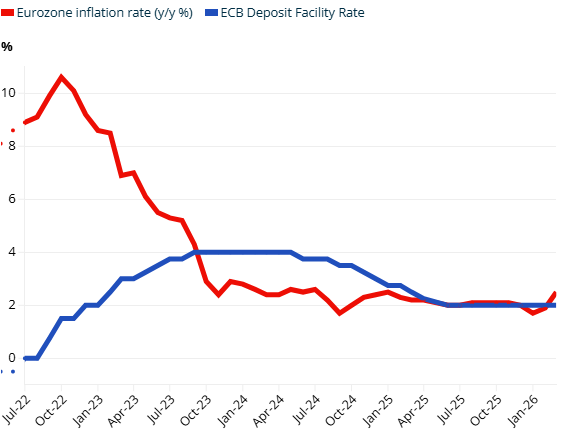

Source: Eurostat

Markets begin to price in “Insurance hikes”

What has changed more noticeably is market positioning. Investors are increasingly pricing in the possibility of “insurance hikes” rate increases aimed not at slowing growth, but at preventing inflation expectations from drifting higher.

The probability of a rate hike at the April meeting currently stands at 36.2%, meaning a hold remains the base case. But by June, expectations shift significantly, with a 76% probability of a 25-basis-point increase.

Markets now assign an 84% chance of at least one rate hike in 2026, a sharp shift from earlier expectations of policy easing. This reflects growing concern that inflation, even if driven by energy, may not fade as quickly as previously assumed.

Inflation expectations and shift toward tightening

The ECB’s challenge is not just current inflation, its expectations wage growth has only recently aligned with the 2% target, and policymakers are wary of losing control of that progress.

If households and businesses begin to expect higher inflation, it can quickly become self-reinforcing. That is why even temporary shocks, like energy price spikes, can trigger a policy response.

ECB is likely to hold steady, using time to assess whether energy-driven inflation spills into broader price pressures. But the tone is clearly shifting.

If oil prices remain elevated and inflation edges higher in the coming months, a June rate hike looks increasingly likely. On the other hand, if energy markets stabilize and inflation cools again, the ECB may delay action.

Either way, the direction is becoming clearer. The ECB is no longer thinking about easing it is preparing, cautiously, for the possibility that tightening may not be over just yet.