What to know before buying Shopify stock

Shopify’s first-quarter 2026 earnings showed stronger-than-expected performance, with revenue and adjusted earnings per share both ahead of forecasts. The results offer useful insight for investors assessing the stock.

Shopify’s revenue increased by 34% year on year to around $3.17 billion.

Q2 revenue growth is in the high-20% range.

The company still trades at elevated earnings multiples, with a trailing P/E of around 114 and a forward P/E near 66.8.

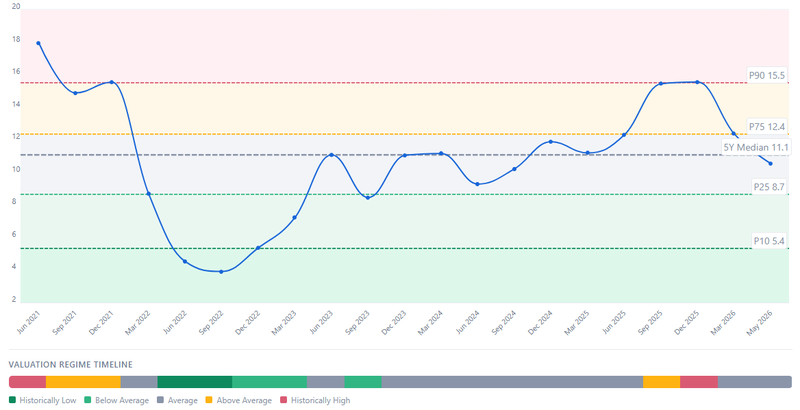

The quarter was strong, but the stock was priced for more

Shopify’s Q1 report was not weak. That is the important starting point. Revenue grew 34% year over year to about $3.17 billion, GMV cleared $100 billion, and free cash flow remained solid at $476 million. For most companies, that would be a very good quarter.

But Shopify is not priced like most companies.

The stock entered earnings with a premium-growth valuation, which means investors were not just looking for a beat. They were looking for proof that Shopify could keep growing at an exceptional pace while expanding margins and defending its long-term platform story.

That is where the reaction makes more sense. The selloff was less about Q1 itself and more about the market questioning how much growth is already priced in.

Guidance became the real problem

The main pressure point was forward guidance. Shopify said it expects Q2 revenue growth in the high-twenties percentage range, with gross profit dollars growing in the mid-twenties and free cash flow margin in the mid-teens.

For a normal business, high-twenties growth would look impressive. For Shopify, it raised a different question: is the company moving from hypergrowth into a more normalized growth phase?

That matters because valuation multiples are tied to future growth expectations. If investors were paying for sustained 30%-plus growth and management starts guiding below that level, the stock can fall even when the quarter itself beats estimates. Shopify did not disappoint the past. It disappointed investors who wanted more certainty about the future.

Transaction losses added another layer of concern

Another issue was rising transaction losses. These are costs linked to payment processing risk, fraud, chargebacks, merchant defaults and other losses that can come with a larger financial-services footprint.

This matters because Shopify is no longer just a simple e-commerce software provider. It is increasingly embedded in payments, merchant financing, fulfilment, point-of-sale systems and broader commerce infrastructure.

As Shopify processes more transactions across more merchants and more geographies, the absolute level of transaction losses can rise. The market can tolerate revenue growth and margin expansion stay strong. But when guidance points to slower growth, investors become more sensitive to anything that may pressure profitability. The concern is not that transaction losses are unmanageable today. The concern is whether they could become a larger drag on margins as Shopify scales deeper into financial products.

Valuation leaves very little room for mistakes

The company still trades at high earnings multiples, with P/E trailing around 114 and forward P/E near 66.8, based on the valuation framing provided. At those levels, investors are not paying for an ordinary software company. They are paying for a platform that can keep expanding revenue, protect margins, grow enterprise adoption and turn AI tools into a real commercial advantage.

Shopify needs merchant demand to stay strong. It needs GMV growth to remain elevated. It needs enterprise brands to continue adopting the platform. It needs AI tools to improve merchant productivity rather than simply becoming another cost layer. And it needs financial services expansion to support margins, not weaken them.

That is why the stock reaction was so sharp. When valuation is this high, the market does not wait for a major deterioration. A small shift in growth expectations can be enough to trigger multiple compression.

Source: Full Ratio

The market snapshot shows how much sentiment has changed

Shopify was trading near $109.25, down roughly 20% year to date. The 52-week range, around $88.14 to $182.19, shows how wide the sentiment swing has been.

That range tells the story. Investors still believe Shopify is a major long-term commerce platform, but they are no longer willing to price the stock as if every part of the story is risk-free.

The bullish case remains clear. Shopify is one of the most important infrastructure layers in global digital commerce. It continues to grow GMV, attract large brands and expand its product ecosystem.

The bearish case is also clear. Growth is slowing from very high levels, valuation remains demanding, and investors are becoming more focused on margin quality than headline revenue growth.

Source: Trading View

AI and enterprise win still support the long-term story

The strategic story has not disappeared. Shopify is still investing heavily in AI-powered commerce tools such as Shopify Magic and Sidekick, which are designed to help merchants create content, manage operations, automate workflows and improve productivity.

That matters because the next phase of commerce may be less about simply building online stores and more like helping merchants operate more efficiently across channels.

Shopify also continues to push deeper into enterprise retail. Recent enterprise wins included names such as Mulberry, Lands’ End and Balmain Paris, reinforcing the idea that Shopify is no longer viewed only as a small-business platform.

Institutional ownership can amplify the move

Shopify also has high institutional ownership, estimated to be roughly 70%. That matters because when large funds reduce exposure around earnings, price moves can become much sharper.

There were signs of distribution and defensive positioning heading into the report, which suggests some investors may have been reducing risk before the numbers. Once the guidance failed to clearly exceed expectations, that selling pressure likely intensified.

Analyst sentiment still appears broadly constructive, with the stock generally framed around a Moderate Buy consensus. But price-target views are becoming more sensitive to execution, margin sustainability and whether growth can remain strong enough to justify premium multiples.

Shopify’s story is still strong, but the bar is higher now

The selloff does not mean Shopify’s fundamentals are broken. Q1 showed strong revenue growth, healthy GMV, solid free cash flow and continued strategic progress in AI and enterprise commerce.

But the market is no longer rewarding Shopify simply for being a high-growth platform. It wants evidence that growth can remain strong even as the company gets larger, and that profitability can improve even as transaction-related risks rise.

That is the difference between a good company and a good stock at the wrong valuation.

Shopify still has the long-term story investors who want commerce infrastructure, AI tools, enterprise expansion and global merchant scale. But after the Q1 reaction, the message from the market is clear.

FAQs

Why did Shopify stock fall after strong earnings

Shopify stock fell because investors focused more on slowing future growth guidance and valuation concerns than on the strong Q1 results themselves.

What were Shopify’s Q1 2026 revenue numbers

Shopify reported approximately $3.17 billion in revenue for Q1 2026, representing roughly 34% year-over-year growth.

What is GMV in Shopify earnings

GMV, or gross merchandise volume, measures the total value of goods sold through Shopify merchants during a specific period.

Is Shopify still considered a growth stock

Yes. Shopify is still viewed as a major growth company, but investors are increasingly focused on whether growth can remain strong enough to justify its premium valuation.

What AI tools does Shopify use

Shopify has integrated AI tools such as Shopify Magic and Sidekick to help merchants automate store operations, content generation, and customer support.