BOJ holds rates in split vote

The Bank of Japan left interest rates unchanged at 0.75%, but the decision looked more hawkish than a simple hold. A rare 6-3 split, a sharp upgrade to inflation forecasts and subtle changes in the policy statement all pointed to growing internal pressure for another move, leaving markets increasingly convinced that June is now the most likely window for the next rate hike.

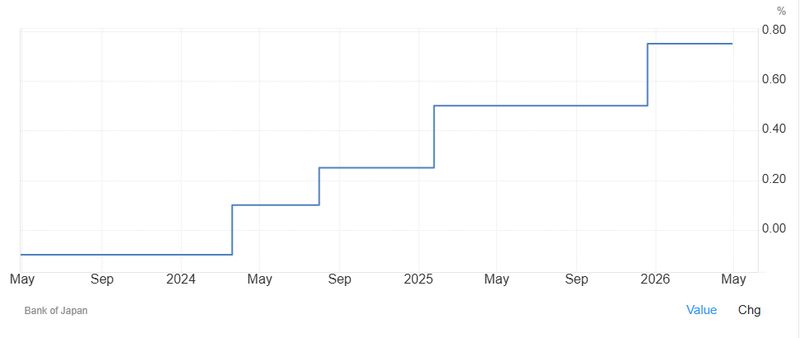

The BOJ kept its policy rate unchanged at 0.75% in a 6-3 split vote.

The unusually divided board strengthened market expectations for a June rate hike.

The central bank lifted its core inflation forecast for this fiscal year to 2.8%.

The yen strengthened as investors read the decision as a hawkish hold, not a dovish pause.

A hold, but not a soft one

The Bank of Japan left its benchmark rate unchanged on Tuesday, but the message beneath the decision was firmer than the headline suggested. The central bank kept the policy rate at 0.75% after its two-day meeting, yet the unusually split vote, upgraded inflation forecasts and more flexible tightening language all made the decision look like a pause on the way to the next move rather than a signal of retreat.

The 6-3 vote marked the biggest division on the policy board since Kazuo Ueda became governor, underscoring how much pressure is building inside the BOJ to keep normalizing policy after years of ultra-loose settings.

Source: TradingEconomics

The split matters more than the hold

What stood out most was not that rates stayed unchanged, but how many board members wanted to move immediately. Three policymakers voted for a hike at this meeting, including hawkish members Hajime Takata and Naoki Tamura, joined by Junko Nakagawa, who is generally seen as more centrist.

That kind of split matters because it shifts the conversation from whether the BOJ is ready to hike again to how soon it chooses to do so. Markets responded accordingly. Traders moved to price a high probability of a June increase, and the yen strengthened as investors interpreted the decision as distinctly hawkish.

Inflation was revised up, growth was revised down

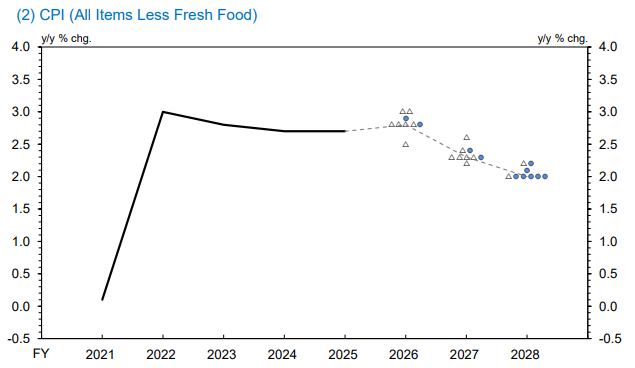

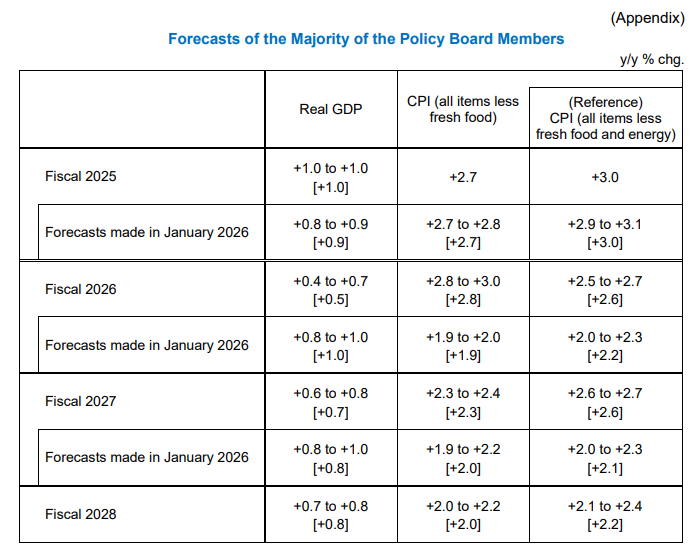

The BOJ reinforced that message in its quarterly outlook report. It raised its forecast for core inflation for the current fiscal year to 2.8%, a bigger increase than many had expected.

Source: Bank of Japan

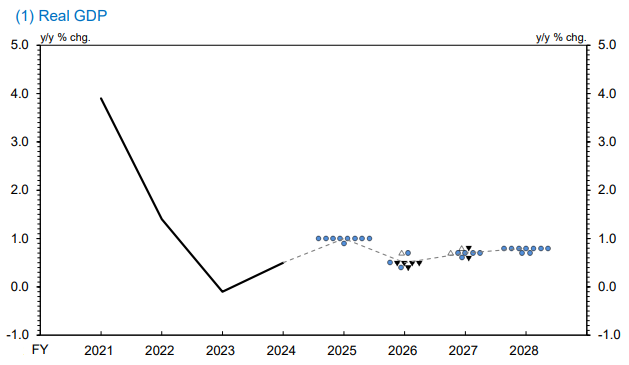

At the same time, it cut its growth forecast to 0.5% from 1%.

Source: Bank of Japan

That combination is uncomfortable, but important. It shows the BOJ is becoming more concerned that inflation pressures are proving stronger and more persistent, even as growth softens. In other words, the bank is no longer operating in a world where weak activity automatically argues for patience. If inflation remains sticky enough, it may still choose to tighten into a slower economy.

Source: Bank of Japan

The Middle East remains the key uncertainty

The central bank made clear that developments in the Middle East and oil prices remain central to its thinking. The war involving Iran and the United States disrupted what had earlier been a market consensus that April could deliver the next hike. Since then, expectations have shifted toward June, largely because policymakers want more time to assess how the energy shock will affect Japan’s economy, inflation path and currency.

That caution was reflected in the statement, which explicitly said the BOJ needs to pay particular attention to the impact of the Middle East situation on financial markets, foreign exchange, economic activity and prices.

That is not the language of a central bank turning dovish. It is the language of one that still wants to tighten, but would prefer not to do so blindly into a volatile geopolitical shock.

A subtle wording change sent a stronger signal

The BOJ also adjusted an important part of its forward guidance. Previously, it signaled that higher rates would come if the economy showed “improvement.” This time, the bank said it would continue responding to “developments” in the economy.

That may sound minor, but it broadens the scope for action. “Improvement” implies clearer economic strength. “Developments” leaves more room for a hike even in a mixed backdrop where growth is slowing but inflation pressures remain uncomfortably high.

That wording shift, combined with the upgraded inflation outlook, helps explain why the market treated the decision as hawkish even without an actual rate increase.

The yen takes the hint

The yen strengthened after the announcement, briefly pushing through the ¥159 per dollar level and moving further away from the territory that previously prompted official intervention. That reaction reflected more than just the split vote. It also reflected the sense that Ueda cannot easily ignore the rising number of board members who now want tighter policy.

This makes the governor’s press conference especially important. Investors will be listening closely for whether he leans into the hawkish signal from the board, or tries to soften it by emphasizing uncertainty and flexibility on timing.

June is now the market’s base case

After the meeting, overnight swaps pricing pointed to a strong chance of a June rate hike. That fits with the broader shift in expectations over recent weeks. April has effectively passed as a missed opportunity, but Tuesday’s decision kept June very much alive.

The logic is straightforward. The BOJ now has a clearer inflation problem, a visibly divided board, and a policy statement that still points toward further normalization if its outlook holds. Unless the Middle East shock deteriorates sharply or growth weakens much more than expected, June increasingly looks like the path of least resistance.

Politics may still complicate the path

The main complication is not inside the boardroom alone. It also sits in Tokyo. Prime Minister Sanae Takaichi’s preference for continued stimulus creates a more difficult political backdrop for normalization, and new reflation-leaning voices are entering the BOJ board.

That may make Ueda more cautious about signaling a fixed timetable. But it does not erase the underlying pressure. If anything, the stronger inflation forecast and the 6-3 vote suggest the internal case for higher rates is building faster than the political environment would prefer.

A pause that points forward

This was not a dovish hold. It was a hold that kept the next hike very much in sight. The BOJ chose not to move in April, but it also chose not to dilute the tightening story. Instead, it upgraded inflation, tolerated a larger public split inside the board, adjusted its language and left the market with a clear impression: the pause was tactical, not strategic.

Unless the Middle East shock materially worsens, June now looks less like a possibility and more like the meeting the BOJ is trying to reach.

Three policymakers voted for a hike at this meeting