Gold under pressure from policy and inflation

Gold dropped 2% as US plans to blockade the Strait of Hormuz following failed weekend talks with Iran heightened concerns over a worsening global energy crisis. The restrictions will apply only to vessels entering or leaving Iranian ports starting at 10 a.m. Eastern Time.

Gold still benefits from fear, but only if that fear does not translate into tighter monetary conditions.

The market has shifted from expecting rate cuts to pricing a “higher for longer” stance, with even a small probability of an “insurance hike”.

Turkey has been selling gold, increasing supply in the market.

Geopolitical risk is no longer enough

Markets are reacting to stalled ceasefire talks in the Middle East and the renewed threat of a blockade in the Strait of Hormuz events that would typically push gold higher. Instead, the reaction has been muted, even negative at times the reason lies in how the market is interpreting these risks. This is no longer just a “flight to safety” story.

The potential disruption to Hormuz, which handles a significant share of global oil flows, is being treated primarily as a supply shock. That shifts the focus from uncertainty to inflation. Investors are not just asking how risky the situation is, they are asking what it means for prices, policy and financial conditions.

This shift matters because it breaks the traditional relationship between gold and geopolitics. Gold still benefits from fear, but only if that fear does not translate into tighter monetary conditions. In this case, it does.

Inflation and oil are reshaping the narrative

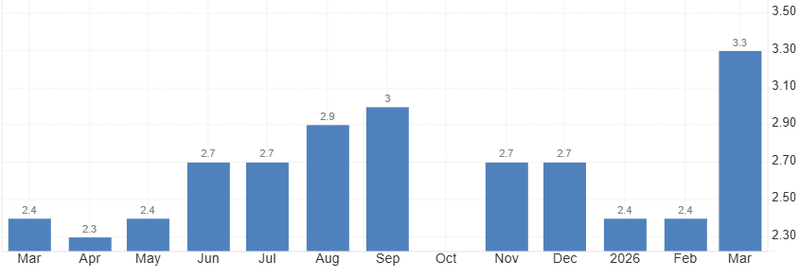

Oil remains above $100, and that is central to the current dynamic. Energy prices have already pushed inflation higher, with CPI rising to 3.3% from 2.4%. More importantly, markets expect this pressure to continue. Even if the geopolitical situation stabilizes, the lagged effects of higher oil prices will keep inflation elevated into the coming months.

Energy acts as a transmission channel. It feeds directly into fuel costs, transport, logistics and eventually food. That creates a second wave of inflation that spreads beyond the initial shock. Markets are looking forward-looking, so they are already pricing this next phase.

For gold, this creates a problem. Inflation alone is not enough to support prices if it leads to tighter policy expectations. In the current setup, higher oil is not just raising inflation, it is raising the risk that inflation remains persistent. That is a very different environment from one where inflation is seen as temporary.

Source: U.S. Bureau of Labor Statistics

The Fed, the dollar and the pressure on gold

The most important driver of gold right now is not geopolitics or even inflation directly it is monetary policy. The Federal Reserve is facing a more difficult environment, where inflation is rising again while growth remains uncertain. The market has shifted from expecting rate cuts to pricing a “higher for longer” stance, with even a small probability of an “insurance hike” if inflation continues to climb.

That shift supports both Treasury yields and the US dollar. Higher yields increase the opportunity cost of holding gold, while a stronger dollar makes gold more expensive for global buyers. Together, these forces create a strong headwind.

This is why gold has struggled despite elevating geopolitical risk. Investors are choosing yield and liquidity over traditional safe havens. The dollar, in particular, is capturing flows that might otherwise have gone into gold.

China have narrowed as retail demand slows, indicating that high prices are beginning to weigh on consumption, official-sector flows add another layer. Turkey has been selling gold, increasing supply in the market at a time when investor demand is already cautious. These flows do not define the trend, but they can amplify short-term weakness.