US inflation accelerates beyond expectations while oil prices rebound

US inflation accelerated to 3.8% in April, primarily driven by surging fuel costs and escalating geopolitical instability in the Middle East. With WTI crude surpassing the $100 threshold and rising inflation risks, market expectations suggest the Federal Reserve may be compelled to maintain or even increase interest rates throughout the 2026–2027 period.

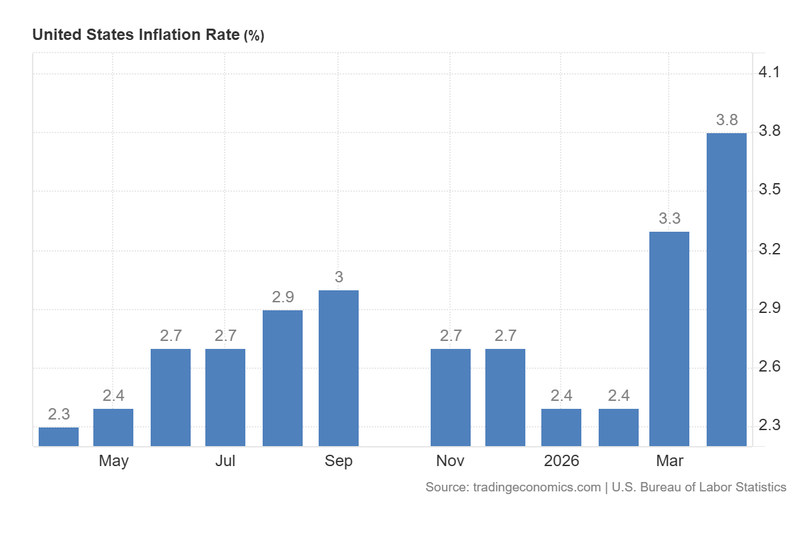

US headline CPI reached 3.8% in April, exceeding analyst forecasts and prompting expectations that the Federal Reserve will forgo rate cuts for the duration of 2026.

Geopolitical volatility pushed Brent oil to $107.70, as tensions involving the US, Iran, and Israel threaten critical logistical routes across the Middle East.

US equity indices delivered a mixed performance, while Treasury yields and the US dollar advanced, reflecting investor apprehension regarding persistent inflation.

Business confidence in Australia fell to -24 points—a level not seen since the 2020 pandemic—as international conflicts continue to disrupt key industrial sectors.

US inflation exceeds forecasts, pressuring the Federal Reserve to remain restrictive

According to data from the US Bureau of Labor Statistics (BLS), the headline Consumer Price Index (CPI) accelerated from 3.3% in March to 3.8% in April, surpassing the consensus analyst forecast of 3.7%. Similarly, core CPI—which excludes the volatile energy and unprocessed food components—rose from 2.6% to 2.8% during the same period, exceeding the anticipated 2.7%. The BLS report highlighted that the most significant price increases originated from the fuel sector, specifically gasoline and diesel.

Although the Federal Reserve prioritises the PCE Price Index for its primary monetary policy framework, the CPI provides vital insights into the immediate price pressures facing domestic consumers. Consequently, market participants are now pricing in a significantly lower probability of a rate cut. According to the CME FedWatch Tool, market probabilities suggest that interest rates will remain unchanged through 2026 and 2027. Furthermore, for certain months, the tool now signals the possibility of a rate hike, given that inflationary risks remain systemic.

Additionally, these mounting inflationary pressures are impacting the US administration ahead of the upcoming elections. President Donald Trump had centred his campaign on pledges to reduce inflation for domestic consumers; however, current data trends appear to be undermining these arguments, potentially impacting the mid-term prospects for Republican candidates.

Regarding the market reaction, US stock indices closed mixed. The S&P 500 index retreated by 0.16% to 7,400 points, while the Nasdaq 100 index fell 0.87% to 29,064 points. In contrast, the Dow Jones Industrial Average rose 0.11% to 49,765 points. Concurrently, 10-year US Treasury yields rose by 5 basis points at 4.46% as inflation risks intensified. Meanwhile, the US Dollar Index (DXY) appreciated by 0.35% to 98.30 points, as investors anticipated a more hawkish stance from the Federal Reserve.

Figure 1. US Inflation Rate (2025–2026). Source: Data from the US Bureau of Labor Statistics; Figure obtained from Trading Economics.

Oil prices surge amid geopolitical instability in the Middle East

Global oil prices remain highly volatile as geopolitical instability persists across the Middle East. Reuters reports that heightened tensions between the United States and Iran have disrupted shipping in the Strait of Hormuz, while military engagements between Israel and Hezbollah in Lebanon continue. These developments have sparked fears that existing ceasefire agreements could collapse, leading to a protracted conflict that would exacerbate global inflationary pressures.

In response, the Brent and WTI benchmarks advanced in tandem as concerns over geopolitical escalation were renewed. The Brent futures contract (BRNN6) increased by 3.44% to $107.70 per barrel, while the West Texas Intermediate (WTI) futures contract (CLM6) appreciated by 4.22% to $102.18 per barrel.

Australian business confidence declines, yet surpasses analyst estimates

According to data released by the National Australia Bank (NAB), business confidence stood at -24 points in April, weighed down by rising inflation concerns linked to the US–Israel–Iran conflict. The NAB report indicates that activity is eroding across several critical metrics, most notably forward orders, capital expenditure (capex), cash flow, and employment.

However, the April reading was less severe than that of March, when the indicator plummeted to -29 points. In both instances, current levels represent lows not observed since May 2020, suggesting that Australian business confidence is deteriorating at a pace comparable to the economic contraction experienced during the pandemic.