BoE facing a hard path

Bank of England walks into this week’s policy meeting with holding rates and facing a more difficult inflation rally than expected earlier in the year.

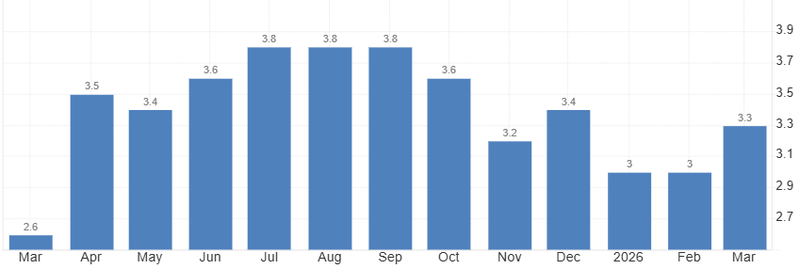

March inflation rose to 3.3%, up from 3.0% in February.

BoE needs evidence on whether higher fuel prices will filter into core inflation.

BoE may be forced into a longer pause or even reopen the door to tightening.

BoE between policy, labour, and inflation

Right now, the Bank of England walks into this week’s policy meeting facing a more difficult inflation rally than expected earlier in the year. The problem is not that inflation is surging again in a dramatic way it is that it is proving stickier than the Bank had hoped at a stage where the disinflation process was supposed to become more predictable.

Creates a policy complication

March inflation rose to 3.3%, up from 3.0% in February, with the main driver being fuel prices, which posted their largest increase in more than three years. On the surface, a 0.3 percentage-point increase may look manageable. But the issue is not the size of the move, it is the source of it.

Higher fuel costs feed quickly into transport, logistics, manufacturing, and household budgets. Businesses absorb part of it at first, but over time those costs are passed on. Consumers then adjust spending behavior, and if those pressures remain elevated long enough, wage expectations begin to shift.

Source: Office for National Statistics

Policymakers are watching closely.

Governor Andrew Bailey has made it clear that the Bank will not rush to judgments on rates despite the recent inflation rebound. That wording is deliberate. It signals that policymakers are not yet convinced the current price shock requires an immediate reversal in policy, but it also tells markets that the easing cycle is no longer on autopilot.

That is largely because the Bank still needs more evidence on whether higher fuel prices will filter into core inflation and wages. Energy inflation on its own can be volatile and temporary. Wage inflation is not. Once higher living costs begin influencing pay negotiations, inflation becomes harder to reverse because it moves from external shock to domestic reinforcement.

labour market becomes central

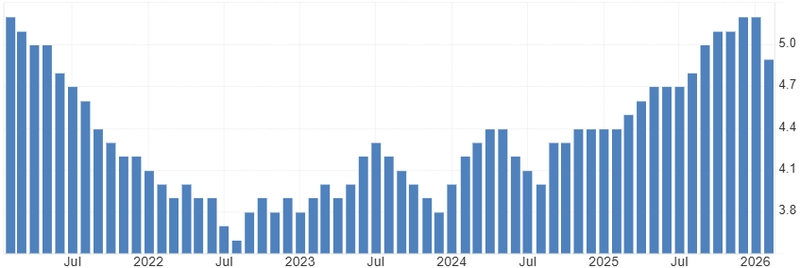

The labour market has softened to 4.9% after recording a peak at 5.2%, but not enough to remove wage pressure. Hiring has slowed, vacancies have declined, and momentum is cooling, but wage growth remains elevated relative to the Bank’s inflation target. That creates the risk of second-round effects where workers demand higher pay to offset rising living costs, reinforcing inflation internally.

That is why tomorrow’s vote split matters almost as much as the rate decision itself. That matters because central banks often communicate future direction through voting dynamics before changing policy outright. A widening hawkish minority would suggest the bar for future cuts has risen materially, and that the Bank is prepared to pause longer than markets may have expected.

The economy is not in recession, but momentum remains soft. Consumer demand is still uneven, business investment remains cautious, and higher borrowing costs continue to weigh on household spending. That limits how aggressive the Bank can become.

Source: Office for National Statistics

inflation changes that equation

Central banks can tolerate slower growth for a period. They struggle to tolerate inflation expectations drifting higher. Once credibility becomes the issue, policy tends to stay restrictive longer than markets initially expect.

In the short term, a hold paired with a hawkish split would likely support gilt yields and provide some strength to the pound as traders push back expectations for additional cuts. But the medium-term picture is becoming less straightforward.

If fuel prices remain elevated and inflation stays sticky, the Bank may be forced into a longer pause or even reopen the door to tightening. Tomorrow’s meeting will be likely to deliver patience. Because the Bank of England is no longer asking how quickly it can continue cutting it is now asking whether inflation is becoming stubborn enough to force a much longer hold or something more restrictive.