The Fed will hold tomorrow, but the real shift may begin under Warsh

A hold is effectively priced in, and under normal conditions that would make the meeting less consequential. But the policy debate is no longer about this meeting, it is about what happens if inflation begins to reaccelerate.

Powell is expected to describe the economy as being on firm footing.

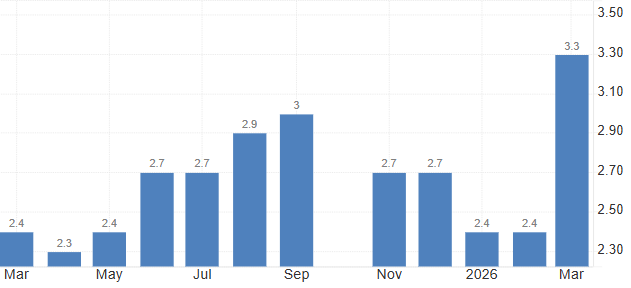

Inflation projections have moved sharply higher toward 4.7%.

Warsh first challenge would be proving independence.

Powell last press conference

Pricing in a pause already happened. Usually, that’d shrink the importance of this gathering. Yet right now, attention shifts past today - curiosity lingers on tomorrow. What unfolds if prices start racing again? Power moves are shifting quietly. Ideas tied to Kevin Warsh gain ground behind closed doors. The real story hides in that change, not in minutes or statements. Tone replaces rules. People outweigh procedures.

Stuck in neutral, Jerome Powell probably won’t budge anytime soon, a sign he still sees inflation as too risky to ease up. Oil costs are climbing once more, thanks to fresh conflict involving Iran, which tugs prices upward right when confidence was building that inflation might be cooling for good. Still, energy often sparks wider price jumps across markets. When oil prices climb, they nudge up transport bills, factory expenses, and what shoppers pay - rippling through the economy in ways that stick around longer than expected.

Even now, Powell will likely say the economy stands solid. Though growth slowed a bit, it holds steady while spending shows little sign of dropping. Hiring isn’t rushing anymore, pay gains aren’t surging either - still, the job scene resists big shifts unless world conflicts worsen or fuel costs refuse to fall. Despite softer trends, balance returns, yet risks linger beneath.

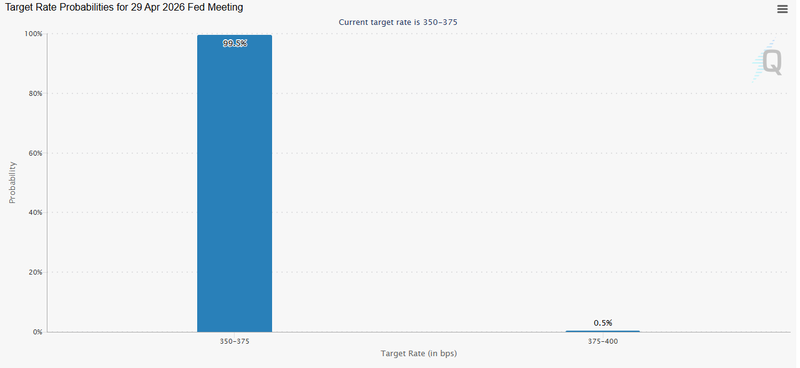

Source: CME Group

That balance keeps the Fed in a holding pattern

Powell may also reference the lessons of 2020, when aggressive policy support helped stabilize growth but later contributed to the inflation surge that forced the most aggressive tightening cycle in decades. That experience remains central to Fed thinking.

Different fed under Warsh leadership

Rather than relying primarily on policy rates, Warsh’s framework points toward a coordinated tightening model where rates and balance-sheet reduction work together. That would mean more aggressive quantitative tightening, likely in coordination with the United States Department of the Treasury, to normalize bond-market functioning faster than the current Fed path implies.

Short-term projections have moved sharply higher toward 4.7%, a level that materially changes the policy conversation. At that point, inflation is no longer drifting above target, it is accelerating back into territory that threatens credibility. And credibility is the one thing the Federal Reserve cannot afford to lose, particularly during a leadership transition.

Warsh has consistently argued that the Fed’s balance sheet has become a structural distortion rather than a neutral policy tool. The current portfolio, still sitting around $6.5 trillion, is central to that argument. His view is that prolonged large-scale asset holdings suppress market pricing mechanisms, distort term premiums, and weaken the signaling function of long-end yields.

Easing would accusations of political accommodation

Inflation itself may force its hand before balance-sheet policy can fully matter. At 4.8% or 5%, the political room for interpretive inflation metrics narrows significantly. Measures like trimmed mean or supercore inflation can sometimes provide softer policy arguments, but at those levels the headline number dominates public perception. Any attempt to justify easing while inflation pushes toward 5% would immediately raise accusations of political accommodation.

Source: U.S. Bureau of Labor Statistics

Warsh first challenge

Warsh’s first challenge would not be to prove loyalty to growth it would be proving independence. And the fastest way to establish that independence would be through policy restraint or even additional tightening.

That matters because it directly conflicts with the political expectation surrounding his nomination. Donald Trump has publicly framed Warsh as a growth-oriented chair and has repeatedly pushed for lower borrowing costs. If inflation forces the opposite outcome, the relationship becomes structurally tense from the beginning.

The historical parallel here is not accidental

The Federal Reserve remains deeply aware of the policy mistakes of the 1970s when premature easing and inconsistent tightening allowed inflation expectations to become embedded. Once that spiral formed, the cost of regaining control became far higher than the cost of acting early.

A renewed move toward 4.8% would also directly challenge one of Warsh’s broader intellectual assumptions that AI and productivity gains will act as structural disinflationary forces. If inflation accelerates despite that productivity narrative, the framework itself weakens, leaving less room for patience.

The immediate market reaction would likely be straightforward. Front-end Treasury yields would move higher as cuts get repriced further out, the yield curve could steepen if balance-sheet reduction accelerates, and the dollar would likely strengthen as real-rate expectations rise.

The message this week may still be “hold, but if inflation continues to climb, the real policy story may shift quickly from when the Fed cuts to whether the next move is no cut at all or something far less comfortable.