BoE and ECB hold rates steady; US PCE rises while GDP growth misses forecasts

The Bank of England (BoE) and the European Central Bank (ECB) maintained interest rates at their current levels while adopting a hawkish rhetorical shift in response to escalating Middle Eastern tensions and energy-driven inflationary pressures. Concurrently, the US Personal Consumption Expenditures (PCE) price index surged to 3.5%, while the first-quarter GDP growth reached 2.0%, failing to meet market expectations.

The BoE maintained the Bank Rate at 3.75% following an 8–1 vote, cautioning that instability in the Middle East and persistent inflationary risks may necessitate further monetary tightening.

The ECB held its benchmark rate at 2.15% but adopted a hawkish stance as Eurozone inflation reached 3.0%; markets are now pricing in three potential rate hikes by the end of 2026.

The US PCE price index accelerated to 3.5% in March due to energy supply shocks, while Q1 GDP grew by 2.0%, missing forecasts despite robust investment in Artificial Intelligence and a rebound in public spending.

US equities rallied on the back of strong Big Tech earnings despite macroeconomic headwinds, while the US Dollar Index (DXY) retreated to 98.09 as the Pound and Euro strengthened following the central banks’ hawkish pivots.

BoE and ECB maintain interest rates unchanged, in line with market expectations

The pre-eminent central banks of Europe—the Bank of England and the European Central Bank—announced their latest monetary policy decisions. Both institutions elected to hold their benchmark interest rates steady, a move that aligned with the consensus amongst market analysts.

BoE holds interest rates unchanged while warning of inflationary risks from Middle East conflict

The Bank of England maintained interest rates at 3.75% amidst a backdrop of mounting economic and inflationary pressures. The United Kingdom currently faces one of the highest inflation rates in the Western world, standing at 3.30%. Simultaneously, the unemployment rate has maintained an upward trajectory over the last three years, increasing pressure on the labour market. Furthermore, UK productivity has decelerated; in the third and fourth quarters of 2025, the UK recorded a modest GDP growth rate of just 0.1%, indicating significant hurdles in the broader economic recovery.

The Monetary Policy Committee (MPC) voted 8–1 to keep the Bank Rate unchanged, with the sole dissenting vote favouring an increase to 4.0%. The BoE warned of potential economic volatility stemming from the US–Israel–Iran conflict in the Middle East, noting that the situation could necessitate higher interest rates or a prolonged period of restrictive policy. The Bank emphasised that the outlook remains contingent upon the duration of the conflict and its subsequent impact on commodity prices, particularly energy. Additionally, the BoE stated that “The Committee stands ready to act as necessary,” signalling that rising inflationary risks are weighing increasingly heavily on the Bank’s economic outlook.

Regarding market movements, the GBP/USD pair appreciated as expectations for a more restrictive BoE stance intensified. The British Pound advanced sharply against the US Dollar, rising by 0.99% to $1.3602. Conversely, despite the BoE’s cautionary tone regarding the economic context, the FTSE 100 index appreciated by 1.62% to close at 10,378 points.

ECB maintains steady rates but adopts restrictive tone amid rising inflation risks

The European Central Bank (ECB) decided to leave its benchmark interest rate unchanged at 2.15%. However, the ECB warned that the US–Israel–Iran conflict in the Middle East is exerting upward pressure on inflation within the Eurozone—a phenomenon that could adversely affect the broader European economy if the conflict persists or escalates. The European Union is currently navigating a dual economic challenge: elevated inflation combined with a sluggish GDP growth rate.

According to data from Eurostat, the EU inflation rate rose from 2.6% in March to 3.0% in April, exceeding the forecast of 2.9% and reaching its highest level since September 2023. Meanwhile, EU Gross Domestic Product (GDP) accelerated by a marginal 0.1% in the first quarter of 2026, falling short of the 0.2% growth anticipated by analysts. Reports from Reuters indicate that market participants now expect the ECB to implement three rate hikes, potentially raising the benchmark to 2.75%. Following these developments, the Euro appreciated by 0.50% against the US Dollar to reach $1.1730.

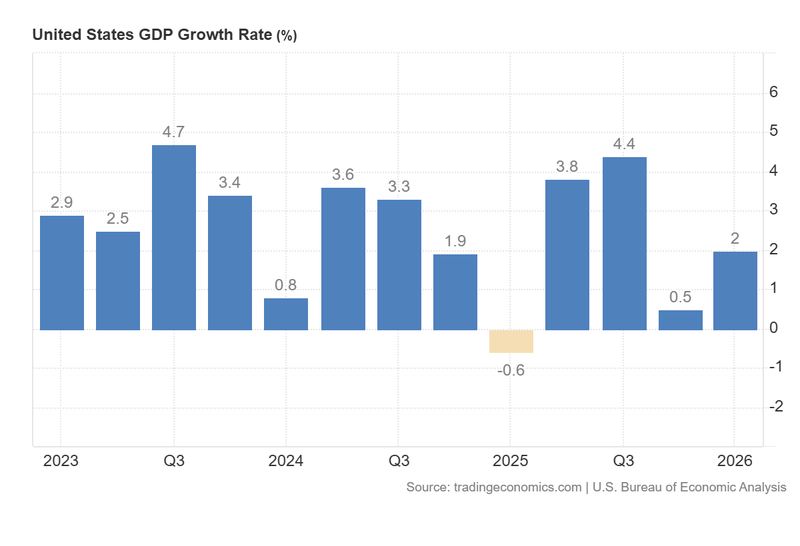

US PCE Price Index accelerates while GDP growth trails forecasts

Data released by the US Bureau of Economics Analysis (BEA) reveals that the year-on-year (YoY) PCE Price Index accelerated sharply from 2.8% in February to 3.5% in March, the highest level recorded since May 2023. In tandem, the US GDP growth rate reached 2.0% in the first quarter of 2026—a recovery from the 0.5% growth seen in the final quarter of 2025, yet still below the 2.3% forecast by analysts.

The BEA report suggests that the surge in US inflation was primarily driven by the conflict in the Middle East, which has caused severe disruptions to the global energy supply chain. This, in turn, has driven up gasoline prices and the cost of a basic basket of consumer goods within the domestic economy. Furthermore, the Core PCE Price Index—which strips out volatile energy and unprocessed food prices—accelerated from 3.0% to 3.2% over the same period.

While the GDP data underperformed forecasts, it nonetheless represents a recovery from the stagnation observed in the fourth quarter of 2025. According to the BEA, private sector investment was driven largely by the Artificial Intelligence sector, while government spending rebounded in comparison to the Q4 2025 where the longest government shutdown in US history happened. Nevertheless, economists remain cautious regarding the second quarter, forecasting a potential negative impact on GDP growth should global energy supply chain instability persist.

Following these economic releases, US equity indices rose in parallel, buoyed by robust first-quarter earnings from the Big Tech sector. The S&P 500 appreciated by 1.02% to 7,209 points, the Dow Jones Industrial Average gained 1.62% to reach 49,652, and the Nasdaq 100 advanced by 0.98% to 27,452 points. Conversely, the US Dollar Index (DXY) fell sharply by 0.89% to 98.09 points, primarily due to the significant appreciation of the British Pound and the Euro following the hawkish pivots by the BoE and ECB.

Figure 1. US GDP Growth Rate (2023–2026). Source: Data from the US Bureau of Economic Analysis; Figure obtained from Trading Economics.